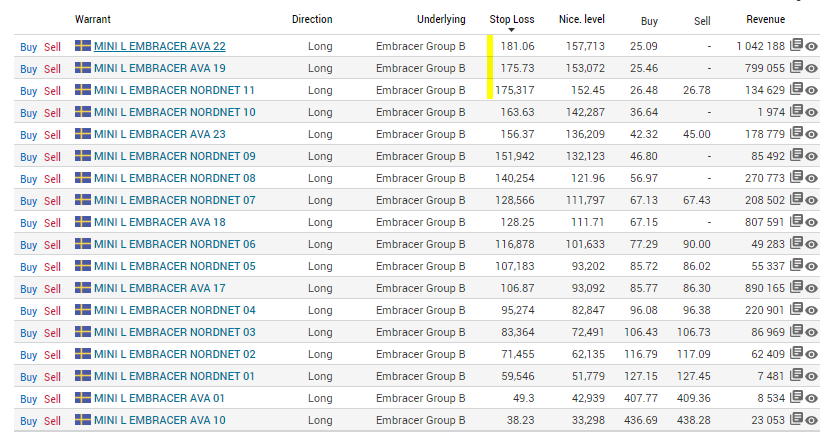

Tulkitsenko nyt oikein, että 175SEK tasolla knokataan useampi warrantti eli laskua saattaa vielä olla luvassa.

8 tykkäystä

Luulisin, että ei noilla ole merkitystä (myöskin Revenue sarakkeesta päätellen), eikä kukaan ainakaan tahallaan jahtaa tällaisessa kioskissa, että nuo knockaisi ja erääntyisi arvottomana. Luultavasti suurin osa on normi pulliaisilla hallussa. Ja vaikka nuo warrantit erääntyisi arvottomana, niin ei pitäisi vaikuttaa osakkeen kurssiin. Normaalisti myös maksellaan vaan rahana mitä pitää, eikä varsinaista kohde-etuutta liikutella.

5 tykkäystä

Niin osaketta shorttaamalla saadaan kurssi laskuun ja ostowarret knokkiin, tapahtuuko näin en tiedä mutta ei varmasti olisi ensimmäinen kerta kun näin on tarkoituksella tehty.

Pääosin, koska verrokkiryhmän arvostus on laskenut…

11 tykkäystä

BUY EMBRACES, SELL THE FACADE GROUP (Directly)

2021-08-12 09:10

STOCKHOLM (Nyhetsbyrån Direkt) In its latest issue, the newspaper Aktiespararen recommends buying the gaming company Embracer and selling the facade company Fasadgruppen.

Assa Abloy, Vimian, Lifco and Addlife will all have to wait for the recommendation.

Embracer has a large acquisition fund earmarked for growth and we have probably only seen the end of the beginning of the journey. Embracer is a stock that deserves its place in a broad, growth-oriented portfolio, but perhaps not today as a core investment for widows and orphans, the newspaper writes.

The façade group is now valued at around 20 times the operating profit (ebita) and the p / e ratio calculated in 2022 is more than double that of the stock exchange’s construction giants, states Aktiespararen and adds that the risk in the share is high.

Börsredaktionen +46 8 51917911 https://twitter.com/Borsredaktionen

News agency Direkt

17 tykkäystä

14 tykkäystä

Lyhyt katsaus

9 tykkäystä

En sano, että Embracer Groupilla olisi suurta tunnettavuusongelmaa sijoittajien keskuudessa, mutta hassua, että puolet jokaisen artikkelin ja videon sisällöstä on aina pyhitetty aiheelle WTF is Embracer group and WTH do they do…

6 tykkäystä

11 tykkäystä

11 tykkäystä

Ostoksia Saberilta. Tällä kertaa kauppa summia ei paljastettu. Onko sitten saatu liian halvalla vai kalliilla. Siinä on pohdittavaa.

Vaikka pelialalla työskentelen on pakko sanoa että noi kaikki yhtiöt on never heard.

9 tykkäystä

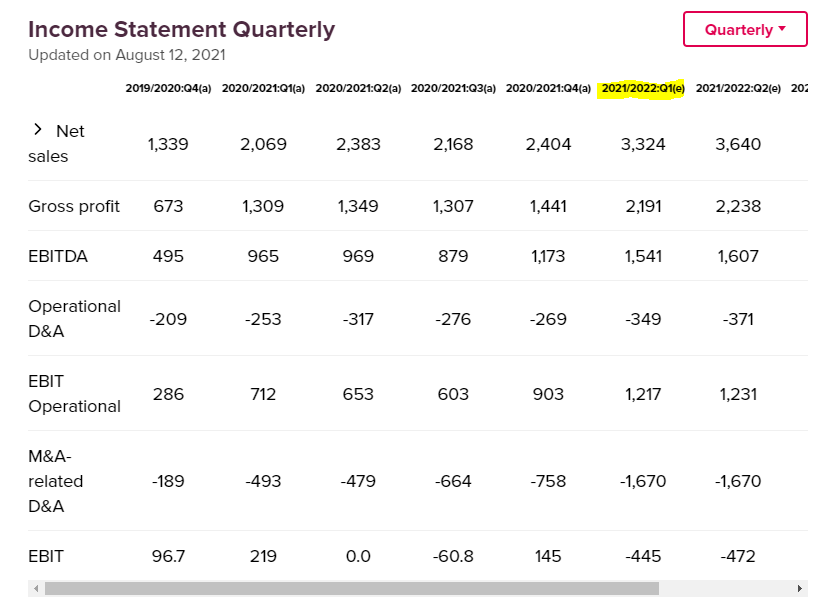

Ihan hyvältä näyttää omaan silmääni. Tässä vielä analyytikkojen ennusteet.

Eiköhän tästä kuitenkin hyvät rommelit saada aikaan.

7 tykkäystä

Hyvältä näyttää tulos. Timontin linkittämä yhtiön sivuilta löytyvät konsensus ennusteet on vaikea selata kännykällä, mutta nähdäkseni ainakin liikevaihto meni yli ennusteista ja ilmeisesti EPS myös

Eikä se biomutantkaan ollut ihan floppi ilmeisesti:

The main revenue driver in the quarter was the release of Biomutant from our internal studio Experiment 101. So far, the game has sold more than one million copies. The full investment into development and marketing as well as the acquisition cost for Experiment 101 and the IP, was recouped within a week after launch.

Management now expects SEK 225 - 275 million in completion value during the second quarter to be followed by a gradual increase in activity and for the fourth quarter to become even busier than previously forecasted. Across the group we have numerous new games announcements planned up until December for products releasing current year and future years. Stay tuned!

We are increasingly optimistic about our long term organic growth prospects with more than 180 games under development. Over the next few years, we are confident that our organic growth will continue to significantly exceed the overall gaming market expansion.

10 tykkäystä

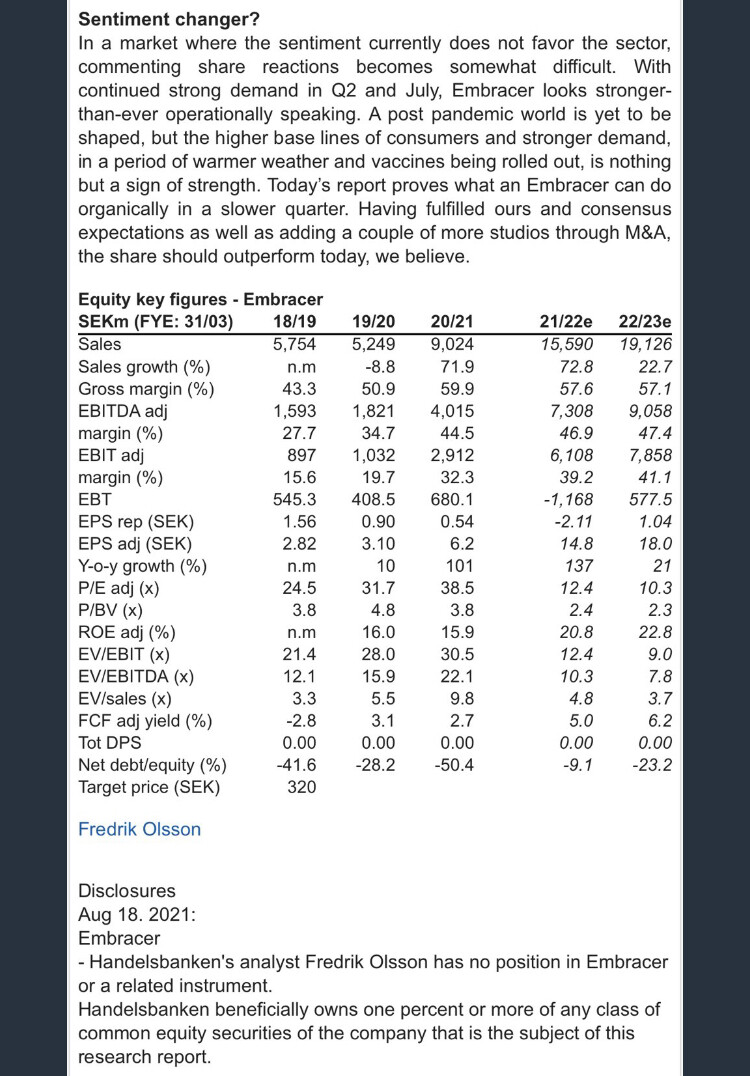

Jos ei tällä saada nousua aikaiseksi niin on kumma… Analyytikot lähes kaikki povaa 300kr tavoitehintaa ja osuu samojen amalyytikoiden ennusteisiin.

8 tykkäystä

Embracer Group - Beat & ~15% organic growth in tough quarter

Q1 adj. EBIT SEK 1,271m, +12% vs. ABG, +5% vs. cons

Prel. consensus 21/22e adj. EBIT estimate up ~10%

Webcast call today at 09:00 CET

Q1’21/22 details and 21/22e outlook

Embracer delivered a strong quarter today, which beat Infront consensus expectations, with an adj. EBIT of SEK 1,271m, +12% vs. ABGSCe and +5% vs. consensus. Revenues were SEK 3,427m, 6% vs. ABGSCe and +3% vs. consensus, for a total y-o-y growth of 65.6%. However, when we adjust for M&A and FX we reach an organic growth of ~15% on a group level (ABGSCe was at 19.5% before the report). We consider this a strong performance given the COVID-19 boosted comparables from last year and compared to many gaming peers which have been struggling for organic growth in this quarter. Games represented 86.4% of total revenues as Gearbox, Easybrain and Aspyr are now fully consolidated, which drove a large uptick in the gross margin, which came in at 76.3%, +16.4pp vs. ABGSCe and +10.4pp vs. consensus, up from 59.9% in Q4’20/21. Ultimately adj. EPS was SEK 2.30 per share, growing 53.7% y-o-y. Management reiterates the previously highlighted current FY pipeline of new games with a development cost of SEK 2.9-3.3bn. The releases will scale up over the remaining three quarters, Q2’21/22e will feature new game releases with a development cost of SEK 225-275m, and Q4 will features the strongest lineup.

Potential consensus estimate changes

We could see consensus 21/22e adj. EBIT estimates come up at least ~10% on the back of the report and the newly displayed gross margin.

Final thoughts

Embracer’s share is down ~3% YTD, following a change in investor sentiment in regard to gaming companies. As such, Embracer is now trading at a 21/22e EV/adj. EBIT of 13x on our estimates, which is ~30% below the five-year historical average. This is despite Embracer having a new game pipeline with a SEK 2.9-3.3bn development cost (~4x last year) which we think will drive ~30% organic growth in a year where peers are struggling for growth and plenty of M&A headroom (SEK +20bn). There is a webcast at 09:00 CET, link: Embracer Group Q1 Report 2021

21 tykkäystä

#Biomutant has sold more than 1 million copies since its release. The full cost of development, marketing, and the acquisition of studio Experiment 101 by THQ Nordic $EMBRAC were recouped within a week.

14 tykkäystä

RedEye kommentoi

4 tykkäystä

Noniin kertoimet tällä ylös jos ei muuten

24 tykkäystä

Jenkeissä pelitaloilla on matalammat P/S-kertoimet kuin täällä (esim. TTWO, EA, ATVI), joten rinnakkaislistaus voi myös johtaa kurssilaskuun.

3 tykkäystä