Saattaa olla vaan joku isompi myyjä joka haluaa luopua osakkeistaan ja myy nyt kun on osarin myötä hyvin likviditeettiä eikä kurssi dippaa isommin vaikka myy isoa positiota.

3 tykkäystä

Yhtiösivu julkaistu: Evolution Gaming Group | Inderes: Osakeanalyysit, mallisalkku, osakevertailu & aamukatsaus

21 tykkäystä

Poimintaa päivän uutistarjonnasta:

EVOLUTION: CLOSE TO FULL CAPACITY AND MARGIN CONTINUED HIGH - CEO

STOCKHOLM (Nyhetsbyrån Direkt) Evolution Gaming beat analysts’ marginal expectations for the eighth consecutive quarter. In the previous quarter, profitability was helped by fewer tables in operation, but now capacity has been shifted up again.

“The covid effect in the third quarter is significantly lower, now we are not operating fully but are starting to approach full capacity and we still see that the margin is at a good level,” CEO Martin Carlesund told Nyhetsbyrån Direkt after Thursday’s report for the third quarter.During the pandemic outbreak, the company was forced to reduce the number of tables in operation, which on the one hand hampered growth in the second quarter, but on the other hand strengthened the margin. According to the CEO, capacity is now on the rise and he expects the number of tables to return to the “peak level” again at the end of 2020 or the beginning of 2021. Whether the current margin level is sustainable over time, however, the CEO does not want to comment .

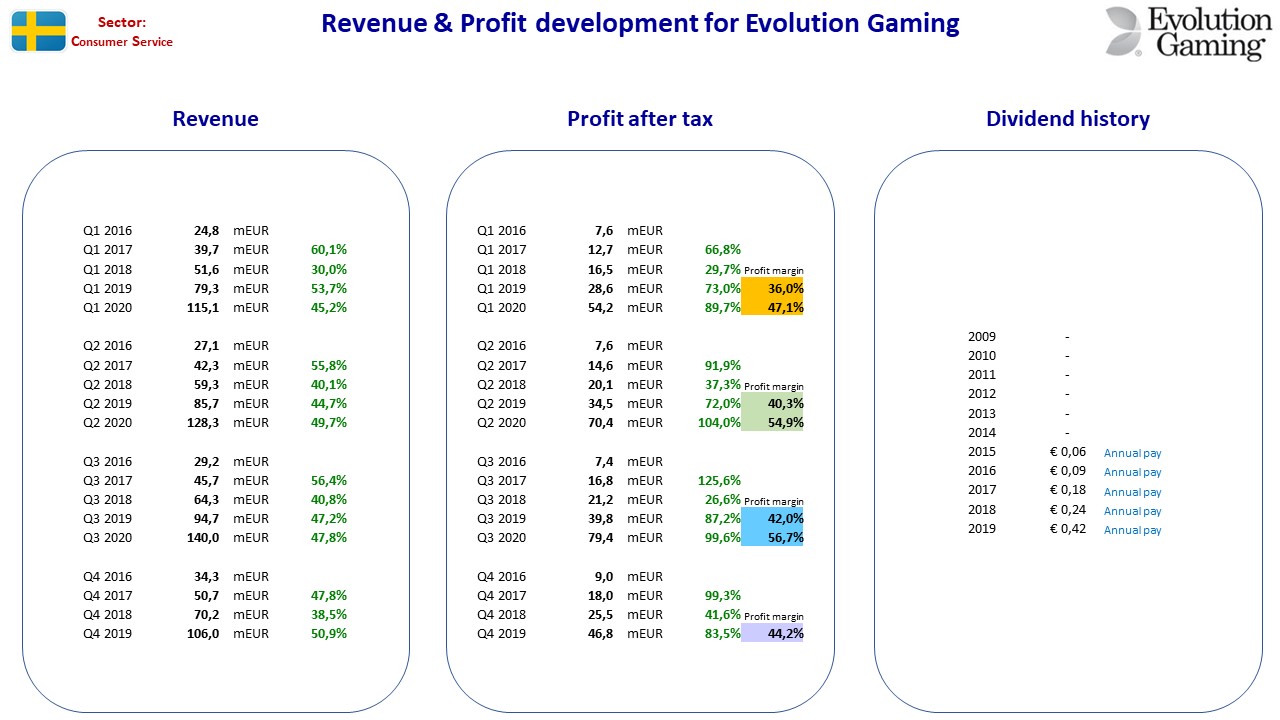

Evolution Gaming has a long history of exceeding analysts’ expectations, and the last three corona quarters have been extra awkward for the experts, but also for the company. Ahead of the year, Martin Carlesund set a goal of reaching over the 2019 margin of 50 percent. With nine months completed and a margin of 61.5 percent, that is the goal in port.

“We thought it was a good goal to strengthen the margin. Of course, with the figures we have today, one can think that it was wrong or right, but I am satisfied with both the guidance and the result,” says Martin Carlesund, who believes that it is in the nature of the matter that prophecies are difficult in the case of Evolution.

“The difficult thing to take in is that a company of our size grows 48 percent with a scalable business model,” he says, adding that the leverage between growth and profitability will be so high and that it is better to be on the cautious side.

When trading on the Stockholm Stock Exchange began on Thursday, the share rose, but then turned into a decline. The report exceeded analysts’ expectations on all points, but at the same time the company announced that German revenues account for between 5-10 percent of total revenues, which was a slightly higher share than the 5-7 percent that, for example, Pareto’s analysts had previously assumed.

These revenues will be affected by the German transitional rules prior to a re-regulation in July 2021. According to the rules, operators wishing to apply for a license may not offer table games. On the total revenue, however, the company believes that the transitional rules will have a limited effect.

The reason why not all revenue from Germany is expected to be erased is that some revenue comes from what is classified as slot games, which will be allowed, in addition, the management at the report presentation indicated that not all operators will try to get a license in 2021, which implies that some will continue to offer Evolution’s live tables even during the transition phase.

During this morning’s report presentation, however, the stock market calmed down and the price climbed steadily upwards and at 10 o’clock was back on the plus side with an increase of just over 1 percent.

5 tykkäystä

Uskomatonta takomista. On firmalla kalliit kertoimet, mutta on niin vakuuttava träkki niin en anna sen häiritä… pitkään holdiin ![]()

6 tykkäystä

5 tykkäystä

näin kovalle kasvajalle P/E 50 on halpa… mikä pitää kurssin näin alhaalla. Onko toimiala epäsopiva ESG mielessä, vai koetaanko online kasinoiden suosio väliaikaiseksi

2 tykkäystä

Varmaan monia syitä.

ESG. Moni iso insituutio ei sijoita sektoriin.

Ruotsalaisuus. Pieni syrjäinen markkina US vinkkelistä eikä yhtiö ole kunnolla jenkkisijoittajien seurannassa, mutta tämä on selvästi hiljalleen muuttumassa ja kasvu jenkeissä tuo näkyvyyttä. Eilisessä earnings callissa oli vain yksi osallistuja jenkeistä, Ed Young Morgan Stanleylta. Jenkkifirmana kurssi olisi jo tuplat.

Kasvupotentiaalin aliarviointi. Eurooppa suurin markkina ja markkinaosuus jo iso täällä ja sijoittajat eivät ehkä ymmärrä vielä miten iso potentiaali Aasiassa ja jenkeissä on. Kuvitellaan että yhtiö alkaa olla jo kasvukäyrän loppupuolella vaikka pelkästään Aasia on markkinana yli 10 kertaa Eurooppaa suurempi ja Jenkit on myös valtava potentiaali.

Pelko regulaatiosta ja vaikutuksista. Saksa nyt konkreettisena esimerkkinä, mutta firma itse näkee tämän positiivisena keskipitkällä aikavälillä (ks alla) vaikka lyhyellä aikavälillä tuleekin negatiivisia vaikutuksia. Eilisestä earnings callista:

Germany is on its way to be the next regulated market in Europe. As of July 2021, online casino games, as well as other games will become regulated. However, until July 2021, the transition period will take place and several operators will stop operating Live Casino. We expect this to have a negative effect on our revenue during the transition to quantify the impact on our revenue system at this time, but an indication is that the German market is around 5% to 10% of our revenues. Important to emphasize is that the move towards regulation in Germany is positive for Evolution, always there will be a notch in the revenue curve during the limited starting [ph] time. In the long run, we expect the German players to return and Live Casino licenses are awarded in July. Regulation of Germany is positive.

13 tykkäystä

Tämä ![]() Evolutionin softa on todella laadukas kilpailijoihin verrattuna. Netent oli iskemässä tähän rakoon satsaamalla paljon uuteen live puoleen, mutta se kilpailu meni siinä

Evolutionin softa on todella laadukas kilpailijoihin verrattuna. Netent oli iskemässä tähän rakoon satsaamalla paljon uuteen live puoleen, mutta se kilpailu meni siinä ![]()

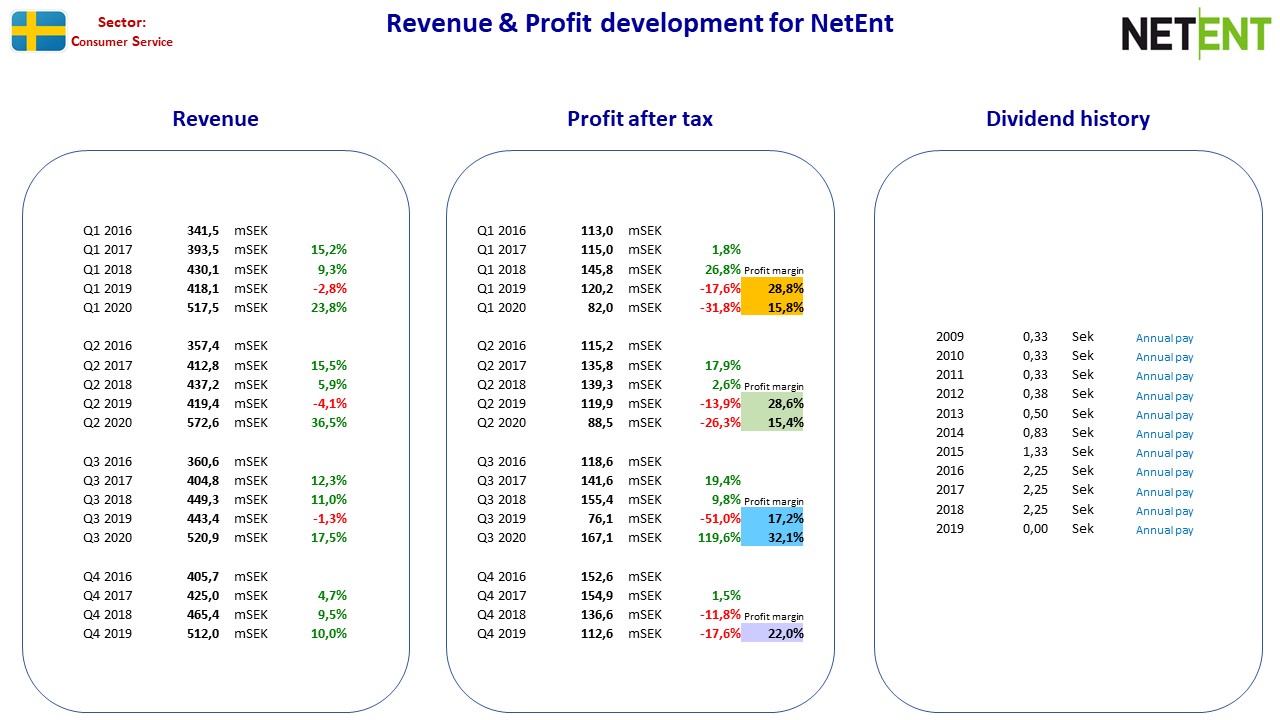

Netentin puolelta kannattaa vielä huomioida noita jenkkilän asioita:

Gross gaming revenues (GGR) from the US market increased by 313% Y/Y and accounted for more than 10% of total Group GGR in the quarter. We remain very excited about the US opportunity and have continued to expand our footprint by signing important customer deals with operators such as DraftKings, William Hill, Tipico, Wind Creek, BetMGM and The Cordish Companies.

During the quarter we continued to invest in our strategic growth areas USA, Red Tiger and Live Casino, while driving cost and revenue synergies from the ongoing integration between NetEnt and Red Tiger. A number of important activities in the third quarter are expected to have a positive effect on earnings in Q4 and onwards, including:

• Market entry in West Virginia in October as the first third-party supplier.

• Expected early entry in Michigan when the market opens.

• Launching Red Tiger’s games in Pennsylvania under NetEnt’s license. Go-live is expected in November.

9 tykkäystä

lisäys la 24.10.2020:

- EVO:lla tällä hetkellä consensus n. 755SEK (marketwatch) ja 770SEK (marketscreener).

- Ensi vuoden EPS-konsensus on 2€ (hajonta tässä hyvin pientä).

- 700SEK kurssilla P/E '21 on noin 34.

- Tuohon jokunen vuosi muutamien kymmenien prosenttien tuloskasvua p.a., niin tulee kertoimet alas kivasti.

NÄISSÄ LUVUISSA OLETETTAVASTI EI NETENT-FUUSIOTA MUKANA.

10 tykkäystä

Offtopic mutta lauantai huumoria. Käytän twitterin automaattista käännöstä toisen kotimaisen kohdalla.

" Morgan Stanley nostaa Evolutionin tavoitehintaa 18% 800 kruunuun (680), ja toistaa liikalihavuuden.[$EVO] "

15 tykkäystä

Pennsylvania launchia

6 tykkäystä

Siitä ihmettelemään kasvulukuja

Usa ja Aasia ansiosta vauhti tulee olemaan vähintään samaa, olettaisin.

11 tykkäystä

Oletko perehtynyt NetEnt diiliin? Onkohan osto menossa läpi minkälaisella todennäköisyydellä ![]() Hinta ei kuulosta omaan korvaan mahdottomalta (~2b$ joista osa omilla osakkeilla) hyötyihin nähden. Kuitenkin samalla saataisiin oman osaamisalueen ulkopuolelta lisää casino osaamista, sekä syötäisiin live puolelta kilpailija pois. Yhdistymisen edut olisivat kyllä huomattavia.

Hinta ei kuulosta omaan korvaan mahdottomalta (~2b$ joista osa omilla osakkeilla) hyötyihin nähden. Kuitenkin samalla saataisiin oman osaamisalueen ulkopuolelta lisää casino osaamista, sekä syötäisiin live puolelta kilpailija pois. Yhdistymisen edut olisivat kyllä huomattavia.

3 tykkäystä

Tässä hyvää tarinaa

However, no serious operator could say no to both Evolution and NetEnt as it would miss out on both the best live casino offering as well as the best slot offering.

All in all, we regard the merger as value-adding for Evolution, and we will have to make substantial estimate changes. As a result, we will make a thorough research update to capture the full impact of this game changing bid and we will most likely increase our fair value.

All operators need Evolution´s and NetEnt´s offering to offer a competitive offering to its players. As a result, Evolution will dominate the online casino supply chain, and we can expect the profit margins to remain on a very high level in the foreseeable future.

NetEnt Q3: yritysoston kautta Evon USA-valtaus saa boostia

Harkitsen edelleen evon lisäostoja tästä 700sek tasoilta.

P/E ensi vuodelle 34. Noin 40% pitkäkestoisella tuloskasvulla PEG on 0.85. Tällaista yhtiötä voitaisiin arvostaa esim. 1.5 kertoimella. Heittäisin fair value 12kk päähän noin 1000sek (ilman netent fuusiota).

9 tykkäystä

Itsekkin luin eilen Björn isaksonin kommentit ja uskon arvostuksen nousevan. EVO saattaa kelailla nyt jonkun aikaa tässä 700-800 sek pinnassa, mutta pidemmälle katsoessa kurssi kohoaa tasaisen tappavasti vakaan kassavirran ja kovan kannattavuuden saattelemana. Varsinkin kunhan tuo Netent saadaan taputeltua ![]()

2 tykkäystä