Käytännössä vuosikymmeniä kasvavaa osinkoa voidaan ylläpitää vain ostamalla samalla omia osakkeita. Kannatan jatkuvaa omien osakkeiden ostamista. Puolet voitonjaosta kasvavina osinkoina ja toinen puolet omien osakkeiden ostoina.

40 tykkäystä

hankittava määrä/summa täyttyy melko varmasti

Maalis-/Huhtikuun vaihteessa.Itseäni kiinnostaisi vielä tätä lisätä omaan salkkuun,

koska uskon @916 mainitseman osinkokiiman

Laskeskelin minäkin eilen ja arvaus tällä hetkellä olisi, että viimeinen omien osto on 21.3. Aiempi laskelmani oli tehty liian suurpiirteisillä luvuilla.

Sammon osinko varmaankin nostaa kurssia sitten alkukeväällä ehkä, hyvä ettei vielä ole nostanut, kun ostelevat omia ![]() Nordean osinko maksetaan aikaisemmin ja siihen saisi tulle myös kova osinkonousu hieman ennen kuin Sampo myy seuraavan tai seuraavat erät.

Nordean osinko maksetaan aikaisemmin ja siihen saisi tulle myös kova osinkonousu hieman ennen kuin Sampo myy seuraavan tai seuraavat erät.

19 tykkäystä

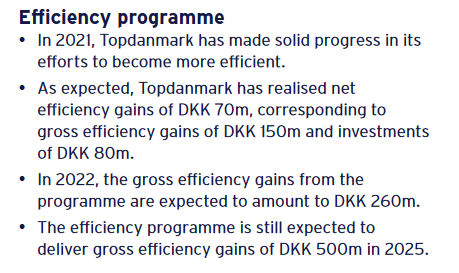

Topdanmark:

Dividend distribution for 2021

The Board of Directors will recommend to the AGM that distribution of a total dividend of DKK 3,105m takes place, representing DKK 34.5 per share, a pay-out ratio of 145.2 and a dividend yield of 9.4. The total dividend is made up of an ordinary dividend of DKK 2,115m from this year’s profit of DKK 2,138m, representing DKK 23.5 per share and a pay-out ratio of 98.9, as well as an extra dividend of DKK 990m, representing DKK 11.0 per share.

Subject to the approval from the AGM, the distribution of dividend will take place immediately after the AGM on 24 March 2022.

–

Higher dividend distribution than expected: 34,5 dkk per share And the share as is down on forward guidance. This is ‘always’ the case. Topdanmark always guides conservatively to be then able to do a positive update during the year.

Edit 1: to prove my point on conservative guidance (even if 2021 proves to be a special year):

CEO words: 2021 was a very satisfactory year for Topdanmark.

We delivered record-strong financial results with a

reported net profit of DKK 2,138m or DKK 1,978m

before run-off, significantly higher than our

original expectation at the beginning of 2021 of

DKK 1,000-1,100m before run-off.

Edit 2: even with the extra dividend of 11 dkk per share, the solvency ratio is still 204 % (down from 243 %). They also state that if no dividend would have been paid this year the solvency ratio would have been 293 % ![]()

Edit 3: I am listening to the conference call and the so called Arne tax (populist tax based on the idea of that certain people in denmark should get early retirement) will increase the tax burden by 4% ![]()

![]() from 2023 or 2024. That is perhaps also a motivator for paying out extra dividends.

from 2023 or 2024. That is perhaps also a motivator for paying out extra dividends.

28 tykkäystä

The upcoming 2 to 3 weeks will of special interest for Sampo. (Sorry for posting again, I will be less vocal after this post ![]() )

)

First, today Sampo is allowed to sell Nordea shares again. The question is will Sampo able to it as elegantly as they did last time around? With on-going global political instability in the air (read Putin) which will potentially have a negative sentiment on the market.

Also, will Sampo sell all 6.1%? And at what price? And should they do it before Nordea posts earning and has its CMD with new return on equity targets?

My personal view is that Nordea should not be too gready at this time, I take anything over 10 euro. Because when this selling process started I bet you that Sampo or any of us would not have foreseen that Nordea would trade over 10 and even 11 euro.

Secondly, Solidium can sell again in early February (I think 5th of Feb). I personally think that they will sell again, as why stop the process now since they already started it. And with the regional elections behind us in Finland, the political thirst for money is not exactly disappearing. If they have some brains I do hope they sell first after 9th of February (Sampo reports) into the first stage of ‘osinko-kiima kausi’.

Third, with Solidum’s exit in Sampo leaves possibly the door open for the next phase in Sampo’s future path. Once Sampo is done with its transformation to an insurance company could possible attract the interest of some global insurance heavy hitters to enter the Nordic market, which is by far the most profitable in the world. Essentially, Sampo can possible become a object for takeover with no anchar investor having a large stake in the company anymore.

All in all, the volatility in the Sampo share can be quite intresting the next 2 - 3 weeks.

Edit: (speculation) if some of the global insurance giants would want a position in Sampo, Solidium exit would offer a perfect staring point. Do anyone have info of who bought Solidiums shares in November?

45 tykkäystä

Solidium sold 11 million shares in november and large buyers were SEB 110 million, Citibank 8,6 million and Sampo 3,4 million.

4 tykkäystä

Mikä on @Sauli_Vilen mielipiteesi Sammon positioinnista kasvu-/arvo-osake kartalla ja mikäli sijoitusvarallisuuden siirtymä kohti arvo-osakkeita jatkuu niin miten arvioit Sammon tästä hyötyvän? Luonnollisesti Sampo ei ole kasvuosake, mutta olisi mielenkiintoista kuulla mielipiteesi miten Sampo normaaleissa markkinaolosuhteissa tulisi pärjäämään tässä siirtymässä kohti arvo-osake sijoittamista?

2 tykkäystä

Sorry I am back again (could not help myself ![]() )

)

I have now been analysing all big insurance players reports published so far (Topdanmark, Tryg and Gjensidige).

Some reflections:

-

Does the Nordic market get any better than this is my first thought? All companies report really good numbers, and most demonstrate around 25 %- 31 % return on equity at the moment. All have pricing power and have or will increase premiums. So inflation is not a worry and for example an interest increase with 1% will benefit Tryg with 300 Million dkk per year.

-

The Nordic market has to be the best insurance market in the world. The retention rate among all big players are around 90%. Meaning that only 1 in 10 custumers in the Nordics are likely change policy provider. And that 10% is most likely custumers the companies are rather happy to get ridd of because these are the ones with most risks as they prone to accidents.

-

Consolidation. The subject is of course relevant for Sampo and the case of Topdanmark. The only way to increase your market presence is to buy another company. As you cannot organically grow too much as those who are likely to change insurance company are customers that are the ones you dont want (because they cost too much).

-

If is going to present a really good result based on the competitive landscape. I will look for in the If report the cost ratio as here If lags its competitors (Tryg and Gjensidige). This lag can also be a product of how cost is calculated in each company and I have no insights into this.

-

All big players are innovative. Buying and integrating different companies to support their massive scale, everything from towing companies to introducing innovative IT solutions and they have the money to develop these. Small companies do not have proper IT budgets and will eventually lag their big peers (will result in that the big ones will buy the small ones, subject to regulation of course)

70 tykkäystä

älä turhaa pyytele anteeksi hyviä analyysejä.

omia mielipiteitä:

1.listatut yhtiöt julkaisevat hyviä numeroja muut sekalaisia paitsi op. itse vänkään sitä, että korkojen nousulla on +/- vakuuttajille. vastuuvelka pienenee, mutta kilpailun pitäisi nostaa Comp ratiota. kilpailu ei toimi minusta kunnolla, saa nähdä tuleeko viranomaisilta sääntöjä, että se tulisi helpommaksi. tanskassa on myös kiinnitetty huomiota alan ylisuureen kannattavuuteen -(kultainen vasikka, autovakuutus)

2 kannattavuustaso on erittäin korkealla. historiallisesti jättiläismäinen.

-

agree

-

IF:iltä tulossa hyvä tulos. ainoastaan private ei juuri kasvane, koska tärkeä automarkkina on eri syistä alamaissa.

-

I concur

5 tykkäystä

En ole varsinaisesti ajatellut tätä, mutta kyllähän Sampo on niiiiiiiiin arvo-osake kuin vain voi olla ![]()

Kyllähän ympäristössä missä asiat kuten tulos, osinko tai jopa oma pääoma/varallisuus (ENNEN KUULUMATONTA!) nousevat esiin, niin Sampo on varsin houkutteleva sijoituskohde. Toisaalta miten tämä sitten vaikuttaa? Minä hinnoittelen Sampoa osien summalla, osinkomallilla ja verrokkien kautta myös jatkossa ja ei tuo käypään arvoon vaikuta. Korkojen mahdollinen nousu voisi viedä pohjaa pois TINA-osakkeiden preemiovaluaatioilta, mutta meidän Sampo-casehan ei ole koskaan nojannut tähän ![]()

61 tykkäystä

Kiitos Sauli hyvästä vastauksesta👍

2 tykkäystä

-

It is hard to see that the market can really get any better than this. Almost all of the main players are “rolling in green” with superior profitabilities. The thesis that “everyone needs to focus on insurance profitability since investment returns are so poor” is starting lose ground as almost all players are earning strong return on the insurance business side. In normal competition environment, high profitabilities all across the board should encourage some players to grow in expense of profitability. This would lead to a price competition and hence lower margins. Obviously, the risk of this continues to climb as the combined ratios continue to go up. Obviously there is always some micro price competition going on somewhere (country, product line etc.), but large scale intense price competition (or even price WAR) is something we have not seen in a long long time. Time will tell if this becomes reality during this decade, but at least the landscape would support the thesis.From If’s perspective it is important to remember that If has pan-Nordic reach which mitigates the effect of possible price war in one market. Since most players are local, the price competition does cross borders. This is why If’s earnings volatility is so low.

-

Yes, the market is fantastic, don’t really see how it can get any better than this. Also I don’t see any sudden change for worse.

-

In the big picture the market is split between handful of big players. There is not really too much room for consolidation. It is worth to notice that you can also grow through price hikes (one of the key drivers during the past years in the Nordics). Obviously insurance prices increase together with GDP (more expensive cars, houses etc.). But obviously without taking market share the growth is limited to close to GDP figures.

-

I’ll comment this later with pre-comment

-

Obviously big players have the scale with IT-investments. However I want to highlight that usually when some industry is disrupted the disruption comes outside the industry or from some new kid on the block (think of FAANGS, Tesla etc.). As you pointed our earlier, the Nordic market has super attractive fundamentals which at least in theory should attract new competition. Obviously, the entry barrier is super super high and it is hard for me to imagine where the disruption would come from (maybe you buy car insurance from the car companies in the future? Or something like that). Anyway this is something Sampo owner should follow, even though there is not any major threat in the foreseeable future

Ps, don’t be sorry, your content is really good and you are great contributor for this forum! ![]()

74 tykkäystä

Some replies to the comments above:

-

My point of being apologetic refers to that I do not want to ‘dominate’ the discussions (with many inputs), as the forum should be about many various viewpoints and thereby improving the Sampo discussions. (voitte hyvin vastata suomeksi, vaikkakin kirjoitan itse englanniksi, työkieli on englanti)

-

With regard to the Nordic pricing landscape, it is of interest to note that all big players underline that they are ‘indirectly’ not going to start a price war. As why would they? All thrive in this environment.

An example of a company who started a price war in order to gain market share was Protector. And look how they ended up. ![]() Undercut anyone with prise and ending up with bad quality customers.

Undercut anyone with prise and ending up with bad quality customers.

- I personally think that there would not be an innovation disrupter in this market.

Why?

One: regulation.

Two: All big players can rather ‘easly’ copy the interrupters. Or at least have the money to do so.

An example of this would be the Nordic banking landscape. Some years ago there where predictions of that the banks would be eaten for lunch by Fintech. Well this in my view has not happened and will not happen. Because of regulation and because of the Nordic banks are quite innovative in comparision to other banks in the world. And if there is a big successful Fintech they will attempt to buy them or copy them.

Three: many of the insurance companies’ custumers a rather satisfied based on different surveys. For example here is one: Danske forsikringskunder er de mest tilfredse i Norden

Lets say Meta, or Google or Tesla would or whoever of the big tech would like to innovative this market. How many of us would trust giving our personal info to these companies? I bet you there would be a lot of trust issues here.

27 tykkäystä

Omien ostoa jatkettu eilen; yhteensä 192 216 kappaletta keskihinnalla 42,58.

20 tykkäystä

Kevään Nordea osinkojen osalta Sampo on uuden edessä, kun omistus on alle 10% ja niistä pitäisi maksaa verot. Lokakuussa - 21 Sammolla oli juuri sopiva 10,1% Nordeasta.

Omien ajatusten ilotulituksena tuli mieleen että jos Cevian ja Sampo laittaisivat Nordea omistukset yhteisyritykseen ennen Nordean osingon täsmäytystä saisivat molemmat (Cevian ja Sampo) osingot verovapaasti yhteisyritykseen.

Tuo tällä palstalla usein viitattu 10% alitus ja sen merkittävyys liittyy myyntivoiton verotukseen, ei osinkoon suoraan. Usko pois, kyllä siellä konttorilla on nämä osattu laskea. ![]()

Edit: Mielenkiintoista on tosin miettiä, milloin loputkin Nordeat lähtee myyntiin? Voipi olla, että Nordean osinkoja ei välttämättä enää tarvitse ottaa huomioon ollenkaan. Myyntirajoitushan taisi mennä umpeen maanantaina (24.1.)?

7 tykkäystä

Oyj:n jakama osinko toiselle Oyj:lle on verovapaata tuloa. Tuo 10% koskee ainoastaan jos Oyj maksaa osinkoa Oy:lle.

Tosiaan Nordean osakkeet olleet Sammon käyttöomaisuutta ja luovutuksen verovapaus perustuu EVL 6b§.

9 tykkäystä

Kappas niin olikin, että listayhtiöiden välillä tämä oli verovapaata - hyvä näin.

1 tykkäys

Tilanne päivitys:

Tähän mennessä on siis ollut ostopäiviä: 79 kpl

Yhteensä ostettu: 11268905 kpl

Ostettujen määrä kaikista osakkeista: ~2,029 %

josta saadaan keskiarvona: 142644 kpl / päivä

ja prosentteina per päivä (per 750milj.) : 0,843 %

ja prosentteina nyt hankittu (per 750milj.) : 66,60 %

Yhteensä käytetty : ~499,5 Milj. €

Keskihinnan ollessa nyt noin: 44,324€

Muutamana viime päivinä on hankittu enemmän kuin 1,1% hankittavasta määrästä versus normaalin 0,8xx% sijaan on selvää että perälauta lähenee nopeammin ja jos vielä se osinkokiima pääsisi iskemään, niin silloin nopeutuu entisestään. Nyt siis näyttää vahvasti siltä, että omien ostot saatetaan saada päätökseen @Aatu mainitsemassa ajassa 21.3. (Juuri nyt laskennallinen 23. tai 24.3.) Mukavasti on viime päivinä keskihinta pudonnut, eikä haittaisi vaikka alehinnat pitäisivät ostojen loppuun ![]()

35 tykkäystä