Oliko lähdettä tälle?

3 tykkäystä

Ilmeisesti näkyy vain jos on maksullinen palvelu tuolla? Sisälsikö minkäänlaista analyysiä?

Baader - TP 47.30 (BUY) 20.1.2022

Morgan Stanley - TP 36.00 (Equalwt/Cautious) 19.1.2022

@Puuhoyla2 Ei näytä olevan analyysia saatavilla ainakaan vielä. Bloomberg Terminal käytössä.

1 tykkäys

En väitä tietäväni mitään yrityksen arvosta taikka siitä miten oikeusjupakat vaikuttavat siihen, mutta logistiikan ammattilaisena tiedän että heillä on erittäin laadukas tuote ja sitä tulee hankkimaan moni alan isoista nimistä. Esimerkiksi DB Schenker ja DSV ovat molemmat hankkimassa näitä tulevaisuudessa useampiin eri varastoihinsa Euroopassa. Olen itse nähnyt nuo käytössä jo Göteborgissa ja Vantaalla. Tältä pohjalta itse ostin osaketta aiemmin ja olen tankannut sitä lisää.

8 tykkäystä

Tätä olen kyllä kovasti pohtinut. Erittäin mielenkiintoinen yritys, mutta mitä mieltä arvostuksesta? Mielestäni jo IPO hinnoissa kallis ja 2022E 500M$ liikevaihto? Yritys kuitenkin lähes 8 miljardin arvoinen. Hankala tästä millään muotoa saada halpaa…tämäkin alka kuitenkin jo sen verran ollut dippailut, että tekisi mieli ottaa positio. En vaan vieläkään ole tätä arvostusta saanut itselleni perusteltua.

3 tykkäystä

Onko tästä vieläkään kukaan onnistunut löytämään minkäänlaista analyysiä? Tuntuu että tästä ei juurikaan ole mitään analyysiä tai keskustelua missään.

Kiistelyt patenteista jatkuvat, saas nähä miten tässä käy. AutoStore AS: Update on litigation with Ocado | Inderes: Osakeanalyysit, mallisalkku, osakevertailu & aamukatsaus

Kiinnostava tutkimus eri automaatio järjestelmistä ja mitä etuja missäkin on. Kannattaa lukaista läpi.

Evaluation of Automated Storage and Retrieval in a Distribution Center

By Adriane Turner:

2 tykkäystä

https://channel.royalcast.com/hegnarmedia/#!/hegnarmedia/20220217_2

Siitä 17.2.2022 tulosesityksen linkki

2 tykkäystä

AutoStore Holdings Ltd. (AutoStore, OSE:AUTO) today announces revenues in the fourth quarter 2021 of USD 93.2 million, up 58.3% from the corresponding quarter in 2020 (USD 58.9 million), bringing the full-year revenues to USD 327.6 million, exceeding the 2021 guidance of revenues of over USD 300 million. The company had an order intake of USD 198.4 million, bringing the backlog to USD 456.5 million, and AutoStore raises the 2022 revenue guidance to USD 550-600 million.

“AutoStore delivered another strong quarter with a revenue growth of 58%, an adjusted EBITDA margin* of 44%, and an impressive order intake of USD 198 million, bringing our order backlog to over USD 456 million. AutoStore continues to benefit from a huge, underpenetrated market with high expected growth rates for fast cubic storage, driven by a strong macro backdrop of labor shortages, pressure on warehouse costs and productivity, and the rapid e-commerce growth. In a highly successful 2021, we increased our market access, continued to gain market shares, further developed our technological leadership and exceeded our own revenue guidance,“ says Karl Johan Lier, Chief Executive Officer of AutoStore.

AutoStore reported revenue in the fourth quarter of 2021 of USD 93.2 million (58.9), and a reported EBIT of USD 5.0 million (11.3), significantly impacted by IPO transaction costs and the Ocado litigation. The adjusted EBITDA* was USD 41.1 million (31.8), corresponding to an adjusted EBITDA margin* of 44.1% (53.9%). The order intake in the fourth quarter was USD 198.4 million (87.9), representing a growth of 125.9%, contributing to a backlog of USD 456.5 million (159.1).

“To support our rapid growth and the increasing demand for AutoStore solutions across regions, we are proud to announce Element Logic as a global partner, providing the rights to sell and implement our technology across the world. Also, with an increasing demand for AutoStore in Latin America, we have the pleasure of announcing a territory expansion of AutoStore in this region with SmartLog. Both Element Logic and SmartLog will bring necessary capacity to a global market with rapid growth from underlying megatrends,“ Lier says.

AutoStore has a strong position to leverage on the global megatrends within e-commerce and automation, where the rapidly growing e-commerce industry, a changing consumer demand, and the emergence of Micro-Fulfillment Centers and the increased demand for automation, in addition to sustainable and efficient solutions, provides a strong platform for growth acceleration.

“The growth and performance highlight the momentum for AutoStore. The record-high order intake and order book provides the company with a significant revenue visibility and AutoStore raises the 2022 guidance from revenues exceeding USD 500 million to USD 550-600 million, with a medium-term growth rate of ~40 percent,“ Lier concludes.

AutoStore will present the fourth quarter 2021 financial results at Høyres Hus, Oslo, Norway, at 08:00 CET. The presentation will be hosted by Karl Johan Lier, CEO, Bent Skisaker, CFO and Mats Vikse, CRO. The presentation will be followed by a Q&A.

The presentation will be broadcasted live at www.autostoresystem.com and can also be streamed

12 tykkäystä

SpareBank1 Markets - NEUTRAL, TP: 28 NOK (45)

Higher uncertainty on order intake and margins

We keep our Neutral recommendation but reduce our target price to NOK28 (45) in order to reflect 1) lower estimates for 2023e-24e, 2) lower peer valuation and 3) higher near-term uncertainty related to order intake and margins. On our new target price, the stock would trade at EV/EBITDA 46x/33x/23x (2022e/23e/24e) and P/E of 85x/56x/38x. Our DCF calculation justify the target price assuming a 2027e ROCE of 40% anda FCF of USD675m, up from USD41m in 2021,8% WACC and a terminal growth of 3.8%, starting in 2028e.

Estimate changes

We increase net income for 2022e by 3.1%, driven by 10.2% higher sales reflecting high order intake in Q4 and the company’s guiding of 2022e revenues in the USD550-600m range. Higher revenues are partly offset by a 4pp reduction in the gross margin, mainly explained by a significant price increase for aluminium. Our 2023e/24e net income is down by 5.9%/9.1% as 2.4% higher sales is more than offset by lower gross margins (input costs + dilution reflection aggressive growth).

Peer valuation hit by rising interests

We have compared Autostore to a selection of companies with both similar business characteristics and similar financial performance. The recent development with rising inflation and interest rates, combined with increased mid-term earnings risk (input costs, long term effects on the economy), has put expensive stocks under pressure. At our target price, Autostore would trade at 46x 2022e EBITDA, well above almost every peer except a couple of software companies. Very few companies in the peer group have demonstrated consistent ROCE above 30%, and only one company (MIPS AB) has an average 2018-2021 ROCE close to the 40% we gradually assume for Autostore towards 2027e.

Increased risk on order intake and margins

We expect a sequential reduction in order intake in Q1 following Autostore’s price increases in December that likely boosted Q4 orders at old prices. The EBITDA margin is expected further down from Q4 driven by higher COGS and limited scale effects at this stage. We also argue that a fair share price should reflect risk of 1) more supply disruption and 2) a “wait-and-see” approach among retailers (consumer confidence, e-commerce post covid),in addition to a 3) long-term risk of new competition that could put the implied growth and profitability expectations under somewhat pressure

Onko kenellä näkemystä? Tuoretta analyysia tästä? Huomenna tulos ja Capitalmarket day. Tätä lyöty oikein kunnolla nyt, alkaisko olemaan ostohinnoissa?

Mäkin mielelläni kuuntelen ajatuksia, jos joku tuota tulosta meinaa perata. En tiedä minkälainen tulos olisi pitänyt tulla, jotta kurssi ei vetäisi noin rumasti…

En tiedä mitkä olivat odotukset ja suoraan sanottuna en osaa ottaa valistunutta arviota, mikä osakkeen arvostuksen tulisi tällä hetkellä olla, mutta itse ostin tänään vähän lisää. Ihan kelpo tulokseltahan tuo näytti ja firman tulevaisuus näyttää hyvältä.

Päivitettyjä rapsoja ei ole vielä tullut vastaan, mutta aamun pikaiset tuloskommentit on.

Tässä ABG:n tuloskommentit:

Q1 Order intake -10% vs cons, Revenues +10% vs cons, Adj EBITDA +9% vs cons, margin 44% (-0.4pp vs cons 44.5%) Order backlog -7% vs cons.

- Outlook: guidance unchanged (and covered by order book). Company has introduced alu surcharge on top of price increases, expects pos margin impact from Q4’22 and full effect from Q1’23. Trial judgement in UK case v Ocado expected in Q3’22.

- Estimates: report is ~2% pos on ‘22e. Given lower GM short-term, expect smaller estimate changes. - Conclusion: a bit stronger Q1 results, but a bit soft intake. Market likely to focus on latter. Needs +200m in coming Qs to support run-rate ~800m in revenues (2023e cons). Share reaction hard to call, but could be down.

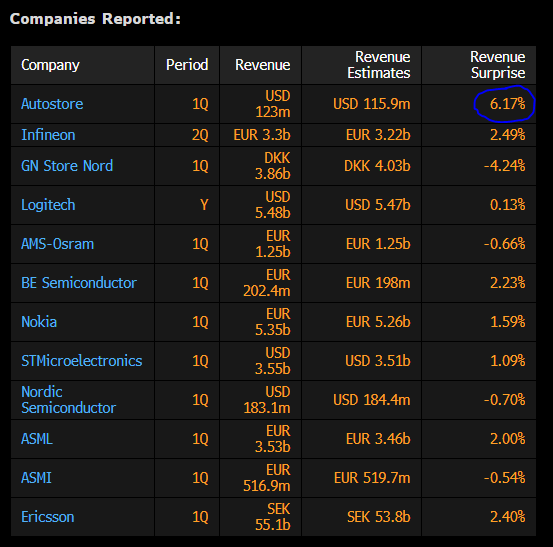

Tässä vielä tällainen tilasto, jossa on jo raportoineiden STOXX600 kuuluvien Hardware ja Semiconductors -yhtiöiden liikevaihdon ylitys/alitus suhteessa konsensukseen. Autostore kärjessä positiivisimpana ylittäjänä:

3 tykkäystä

ABG:n päivitetty rapsa julkaistu. En tiedä miten niitä saa sellaisenaan jakaa, mutta tässä kopioitu tekstipätkiä. TP laskettu 37 → 28, suositus OSTA.

AUTOSTORE

Q1 was good, but order levels a concern

AutoStore reported adjusted EBITDA of USD 54.2m, 9% ahead of

consensus, driven by revenues that were 10% higher than expected,

partly offset by a slightly weaker adj. EBITDA margin (44.0% vs.

consensus at 44.5%). However, the focus of the report was the weaker

than expected order intake of USD 160m (-10% vs cons), down 19%

sequentially. While it is more than enough to cover 2022 estimates, we

note that given 9-12-month lead times, AutoStore needs an average

order intake of close to ~USD 200m per quarter in order to support

consensus ‘23 revenue estimates (~USD 800m). In our view, this is still

achievable, but it means intake needs to come materially up again in the

coming quarters. Overall, we make smaller negative estimate changes

after the Q1 report, mainly driven by lower short-term gross margin

assumptions for ‘22e.

2023 margins supported by price hikes and surcharges

The Q1 report showed continued gross margin pressure from raw

material prices (aluminium prices), and this will likely continue in Q2-Q3.

Based on this, our gross margin assumptions are reduced for 2022e (by

-2.3pp). At the same time, the price hikes on new orders from December

2021, and temporary surcharges on aluminium introduced in Q1, will

support margins into 2023. For employee costs and other opex, we make

smaller revisions.

Uncertainty creates opportunity – BUY

While the share is down ~50% YTD, AutoStore has actually delivered

better results than expected, i.e. this is mostly a matter of multiple

contraction. AutoStore is now trading at a ‘23e EV/EBIT(A) of ~16x and a

‘23e adj. P/E of ~22x, respectively, 30-40% below peers. While estimate

uncertainty has increased, we believe the long-term prospects for

AutoStore is still strong and argue that the pricing is attractive at these

levels. Based on this, we keep our BUY recommendation but reduce our

TP to NOK 28 (37) following a material decline in peer multiples.

Q1 results

In our view, the Q1 results in isolation were good, but this was largely

overshadowed by the weaker than expected order intake (-10% vs cons). While it

is more than enough to cover 2022 estimates, we note that given 9-12-month lead

times, AutoStore needs an average order intake of close to USD 200m per quarter

in order to support consensus ‘23 revenue estimates (~USD 800m). In our view,

this is still achievable, but it means intake needs to come materially up again in

the coming quarters.

Adj. EBITDA beat driven by higher backlog conversion

AutoStore reported adj. EBITDA of USD 54.2m, 9% ahead of consensus, driven by

revenues exceeding consensus by 10% alongside a slightly weaker adj. EBITDA

margin (44.0% vs. cons 44.5%). The stronger revenues imply higher deliveries on

the backlog, i.e. better conversion (27%). This is still well below the historical trend

(35% avg. in the last 8 quarters), but better than expectations (25%). While

AutoStore still says that there is a tight market situation in the short-term, it does not

seem to have significant negative implications for production.

Weaker GM partly offset by leverage on opex

The lower adj. EBITDA margin vs our estimates in Q1 was mainly driven by lower

gross margins (-2.1pp), down ~3pp q-o-q due to higher raw material costs on the

back of the higher aluminium prices seen in 2021 (lags aluminium price by 3-9

months). At the same time, the price hikes on new orders from December 2021 and

temporary surcharges on aluminium introduced in Q1 should in our view support

margins into 2023. According to AutoStore, the adj. EBITDA margin in Q1 would be

closer to ~50% (vs. 44% reported) based on the pro-forma inclusion of aluminium

surcharges and the previously announced price increase.

6 tykkäystä

JP Morganin päivitetty raportti ja kommentit.

TP laskettu 48 → 40, Suositus OVERWEIGHT.

Lopussa yhteenveto riskeistä.

AutoStore

Our take:

AutoStore reported Q1’21 revenues of $123m, +92% yoy and beating consensus by 10%, as growth continued to be strong. Order intake also remained strong, growing 112% to $161m in Q1, supported by underlying market trends including e-commerce growth, labour shortages and pressure on warehouse costs. Order backlog stood at all-time high of $487m (+129% yoy), and provided visibility and support for management’s reaffirmed 2022 guidance for $550-600m in revenues. Adj. EBITDA was $54m in Q1, +68% yoy, beating consensus by 9%, and reflecting a margin of 44% (-6.3ppt yoy impacted primarily by the higher cost of aluminium, as anticipated). Margins look likely to remain impacted in the near term, but price increases from Dec’21 and an aluminium surcharge introduced in Q1 should help margins recover by Q4 this year as projects move from backlog to realized revenue. Litigation costs relating to the IP infringement cases with Ocado continued to rise to $9.9m in Q1, and so far the US ITC was decided against AutoStore (although appealed), the German cases were stayed for now, and the UK case has been to trial with a decision expected this summer.

Noteworthy Areas:

- AutoStore introduced an aluminium surcharge in March 2022, on top of the previously announced 7.5% price increase in December 2021.

- Regionally,Q1 revenue growth was +132% in EMEA, +5% in NAM, and 389% in APAC. NAM has strong order backlog for 2022, but the lower revenue growth was related to timing of delivery. APAC revenue is expected to grow strongly this year.

- Simplified FCF was +86% yoy in Q1 to $41m, and cash conversion stood at 76%.

- AutoStore continues to strengthen its supply chain by securing more capacity, adding new suppliers, and increasing levels of inventory.

- Partner network expanded with Element Logic as a global partner, SmartLog as a distribution partner for Latin America, and Doosan Logistics Solutions as a distribution partner for South Korea.

- New products launched included the R5+ robot for larger bins, and the newly redesigned Bin Lift 2.0 that enables flexible utilization of warehouse space, while extending bin reachability.

Impacts from the war in Ukraine

AutoStore has halted all sales activities to companies in Russia and stopped all marketing and other initiatives directed at Russia. Overall, it expects a very limited direct impact from the war, as the sales activity had been low in Russia/Ukraine. AutoStore also does not have any employees in the regions. However, AutoStore does expect to see an impact on the cost of grid parts. While it does not source any materials directly from suppliers in Ukraine or Russia, there could be indirect effects, in particular regarding aluminium. Prior to the war, the aluminium market was already constrained, primarily due to high European energy prices, which have come under further pressure by the war. Furthermore, Russia is a global supplier of raw materials used in aluminium production,and hence the supply and price could be further impacted.

Outlook & Guidance:

2022 Guidance confirmed. 2022 Guidance is for revenues to be $550-600m. The company does not guide for adj. EBITDA margins but notes that material costs are likely to continue impacting margins until price lifts and surcharges can fall through from Q4 with full effect from Q1 2023 trending towards historical levels in FY23 (i.e. the ~50% seen from 2018-2021).

Suurimpina riskeinä tällä hetkellä:

- Patenttikiista Ocadon kanssa, joka voi johtaa epäsuotuisaan lopputulokseen.

- Toimitusketjuongelmat ja sen myötä nousevat kustannukset.

- Teknologiaosaamisen ylläpitäminen ja oman teknologian kehittäminen. Yhtiöllä noin 95%:n markkinaosuus tämän hetken asennuksista, joten potentiaaliset asiakkaat saattavat valita kilpailijan, joilla on kehitetty oma vastaava ratkaisu.

- Suuri riippuvaisuus kumppaneista ja heidän myyntiverkostosta, koska myynti tapahtuu pääosin heidän kautta.

- Jatkuvan liikevaihdon pieni osuus vaikeuttaa pitkän tähtäimen myynnin ennustamista. Liikevaihdon jakautuminen erittäin suppeaa; kaksi myynnissä olevaa varastojärjestelmää muodostavat +90% liikevaihdosta.

- Valmistus aivan liian keskittynyt. Tällä hetkellä vain yksi tuotantolaitos, joka sijaitsee Puolassa. Uusien laitosten avaaminen ilmeisesti suunnitteilla Jenkkeihin ja Aasiaan.

- Uusien yritysostojen integroimisen, liikevaihdon ja synergioiden kanssa mahdollisuus alisuorittamiseen.

7 tykkäystä

Yhtiö korosti edelleen parenttikiistan epäsuotuisen päätöksen 3. Kvarttaalilla olevan pieni, joka ei haittaa liiketoimintaa. Ei tässä kuitenkaan ainakaan hirveän hyvin ole tähän asti ainakaan mennyt asian kanssa. ![]() Yhtiö kertoi inflaation aiheuttamien kustannusten sisäänajaminen myyntihintoihin korotuksina toimineen vielä toistaiseksi. Uskoisin, että pyörivät melko lailla asiakkaidensa budjettien rajoilla.

Yhtiö kertoi inflaation aiheuttamien kustannusten sisäänajaminen myyntihintoihin korotuksina toimineen vielä toistaiseksi. Uskoisin, että pyörivät melko lailla asiakkaidensa budjettien rajoilla.

Myös yhtiön laaja-alaisen kansainväisen toiminnan puolesta on outoa, että ainoastaa Puolasta löytyy tuotantoa. Laajennussuunnitelmat vaikuttivat kuitenkin hyviltä.

Ajat eivät ole helpoimmat tämänkään yhtiön kohdalla. Kuitenkin Autostoren Q1 vaikutti valoisalta tulevaisuuden kannalta. Uskon nykyiseen strategiaan, yhtiön ollessa kuitenkin melko merkittävä ja ainutlaatuinen tekijä varastoautomaation markkinassa.

Tiedä sitten kuinka paljon tälle kannattaa antaa arvoa, mutta kuitenkin.

Independent Board Member recently bought kr1.9m worth of stock

On the 18th of May, Viveka Ekberg bought around 100k shares on-market at roughly kr19.17 per share. This was the largest purchase by an insider in the last 3 months. This was the only on-market transaction from insiders over the last 12 months.