Kiitos palautteesta ![]() Kävin korjaamassa alkuperäistä kirjoitusta niin että muutin vähän sanamuotoja sekä lisäilin enemmän perusteluja näkemyksilleni

Kävin korjaamassa alkuperäistä kirjoitusta niin että muutin vähän sanamuotoja sekä lisäilin enemmän perusteluja näkemyksilleni ![]()

Katselin Marketscreeneriä ja laittoi miettimään, mikä laittaa analyytikoita muokkaamaan kohdehintaa? Esimerkiksi TP on nyt alhaisempi kuin Huhtikuussa 2021, jolloin yritys oli pienempi (sen jälkeen siis on tehnyt yritysostoja ja kasvanut orgaanisesti). Ovatkohan analyytikot vähän laiskoja, ja mätkäisevät tavoitehintoja pelkkään Hypeen ja kurssinousuun perustuen, vai muuttavatko niitä yrityksen fundamenttien muuttuessa? Ymmärtääkseni Bicolla ei ole ollut mitään vastamäkiä liiketoiminnassa, vaan kasvu on ollut erittäin reipasta. Vai onko analyytikoilla (tai muilla?) tiedossa jotakin jota en vain sitten itse tiedä?

1 tykkäys

Tuohan on aika tyypillistä että tavoitehinta muuttuu osakkeen hinnan mukana, ja tuskin BICO on tämän suhteen poikkeus. Analyytikoiden perusteluna on yleensä se, että markkinoilla hyväksytyt kertoimet ovat muuttuneet. Toki ne ovatkin, etenkin kovaa kasvaville yhtiöille joiden pitkän aikavälin tulevaisuus on keskimääräistä yhtiötä enemmän hämärän peitossa.

Lisäksi BICO:n osalta Q3/2021 tulos oli markkinoilla pettymys, mikä selittää tuon marraskuun kohdalla tapahtuneen laskun kurssissa ja tavoitehinnassa.

2 tykkäystä

CollPlant and CELLINK will explore the use of CELLINK’s next-generation high throughput extrusion bioprinters for the future commercial production of CollPlant’s regenerative breast implants, addressing a $2.8 Bn market with 2.2 million procedures performed annually worldwide.

2 tykkäystä

With immediate effect, BICO’s CFO, Gusten Danielsson leaves the company and his role as CFO.

Shares in BICO Group fall as much as 26%, the most since November, after the lab-equipment company announced its CFO and co-founder, Gusten Danielsson, would leave his position with immediate effect.

- BICO CEO Erik Gatenholm says in phone interview a CFO change is needed to develop BICO further as an international health-care concern

- “It’s a journey we got ahead of us that demands we have the right skills in the right place,” Gatenholm says

2 tykkäystä

CFO lähtee, kurssi tällä hetkellä -28% ![]() Huipuistakin tultu alas jo aika paljo. Harmi kun tästä on niin huonosti uutisia löydettävissä. Toisaalta tekis mieli ostaa lisää, mutta en oikein osaa perustella itselle muulla kuin ”halvalla” hinnalla

Huipuistakin tultu alas jo aika paljo. Harmi kun tästä on niin huonosti uutisia löydettävissä. Toisaalta tekis mieli ostaa lisää, mutta en oikein osaa perustella itselle muulla kuin ”halvalla” hinnalla ![]()

1 tykkäys

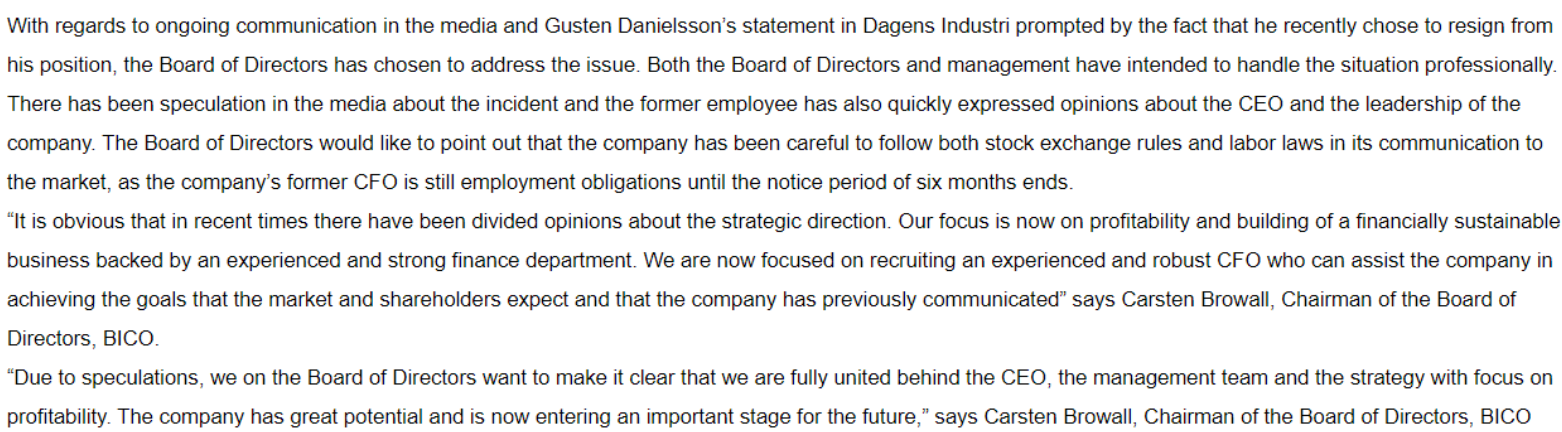

Dagens Industrissa on ilmeisesti juttu, mutta maksumuurin takana. Ilmeisesti äänesti sitä vastaan että hallitukselle annettaisiin vastuuvapaus. Voisi kuulostaa siltä, että siellä on hassattu rahoja vastuuttomasti, jos ei sentään rikoksia tehty. Onko kenelläkään enempää tietoa tai muita lähteitä? Seuraako joku ruotsinkielisiä keskustelupalstoja?

2 tykkäystä

Gusten (ex-CFO) oli myös ainoa, joka äänesti nykyisen hallituksen ja hallituksen puheenjohtajan uudelleenvalintaa vastaan. Lopuksi päätti äänestää jaloillaan. Jatkaa kuitenkin omistajana, koska uskoo yhtiön menestyvän kunhan vain johto osaa viedä yhtiötä oikeaan suuntaan oikein.

Tässä Translatella käännetty: BICO: BEHÖVER NY VD ENL TIDIGARE FINANSCHEF - DI (privataaffarer.se)

STOCKHOLM (Nyhetsbyrån Direkt) Gusten Danielsson, one of the founders of Bico who left his role as CFO of the company on Tuesday, believes that Erik Gatenholm is no longer the right CEO for Bico.

It writes Dagens industri.

On Tuesday, Bico announced that Gusten Danielsson will leave with immediate effect as CFO of the company, something that caused Bico’s share price to plummet. At the subsequent Annual General Meeting on Tuesday, Gusten Danielsson then voted against granting the Board discharge from liability.

"I believe that Bico with the right leadership has a bright future. I still own all my shares in the company. That I resigned as CFO of Bico on April 25, however, reflects my conclusion that Erik Gatenholm is no longer the right leader for the company - even if he remains a controlling shareholder ", states Gusten Danielsson for Dagens industri and continues:

“In the meantime, I expect the board to maintain good corporate governance aimed at protecting all of Bico’s shareholders. My votes at yesterday’s AGM reflect that expectation.”

Gusten Danielsson is Bico’s eighth largest owner with just under 1.3 million shares, of which a small part are A shares, corresponding to 2.01 percent of the capital and 2.63 percent of the votes, according to the owner database Holdings.

Yhtiön hallituksen vastaus:

3 tykkäystä

Mitähän tänään tapahtuu? Kurssi nyt -57%…

Täytyypä koittaa etsiä netistä tietoa.

Edit: nyt löytyi, negaria puskee (google kääntäjän läpi):

BICO Group romahti yli 50 % voitosta varoituksen jälkeen - Varoittaa epävarmasta markkinatilanteesta

Taloudellinen aika • Tänään 16:37

Bioteknologiayritys BICO Group on raivoissaan perjantai-iltapäivällä. Tämä sen jälkeen, kun yhtiö varoitti perjantai-iltapäivänä voitosta ja antoi näkemyksensä tulevaisuuden markkinatilanteesta ja samalla käynnisti kustannussäästöohjelman. Pian kello 15 jälkeen BICO oli romahtanut yli 50 %. Toisen vuosineljänneksen alustava liikevaihto (ilman asiakasluottoja) oli 543 MSEK (293), mikä vastaa kasvua.

Alkuperäinen linkki ko. Uutiseen:

Omassa salkussa ollut Cellink ajoista saakka, ekat ostot 12/20 ja lisäyksiä keväällä -21, nyt komiat -90% taulussa😡

3 tykkäystä

Jestas. Ajattelin jo, että nyt on käynyt kuningasmoka ja tuote ei toimi tai muuta vastaavaa. Kyllähän tämä mieltä syö, mutta ilmeisesti kasvun hidastuminen johtuu enemmän ulkoisista tekijöistä kuin sisäisistä ongelmista. Näin ainakin toivon. Nyt täytyy pitää hatusta kiinni. Nähtävästi itse ydinliiketoiminnassa ei ole vikaa, mutta asiakkaat ovat päättäneet lykätä suuria hankintoja tulevaisuuteen epävarmassa markkinatilanteessa. Ymmärrettävää, kun ottaa huomioon sodan Ukrainassa ja yleisen inflaation. Useat läheet ennustavat taantumaa kasvun sijasta.

With this rapidly changing market environment, we can see a shift in our customers’ liquidity and buying behavior, with purchasing decisions for larger CAPEX being pushed forward, for example, impacting sales across Biosciences and Bioautomation.

The cost reduction program target to reduce expenses by 100 MSEK on a twelve-month basis.

“While experiencing an increasingly uncertain world around us, we are focused on achieving desirable organic growth while delivering a positive EBITDA,”

Enemmän dataa odotettavissa 24.8.2022.

The full financial performance and outlook, as well as an update on cost reductions, will be presented in the interim report January – June 2022 scheduled for August 24, 2022.

Tässä uutinen Bicon sivuilta.

Nyt kysytään kanttia.

Edit: Syytän Venäjää tästä(kin).

3 tykkäystä

Onko joku osallistumassa? Voisi laittaa yhteenvetoa foorumille, jos pääsee kuulemaan.

On the occasion of the press release issued on Friday July 15 2022 regarding the preliminary performance for the second quarter, BICO invites to a combined presentation audiocast and telephone conference with the opportunity to ask questions. The conference will take place on Monday 18 July at 10:00 CET. President and CEO Erik Gatenholm, and Interim CFO Mikael Engblom will hold a short presentation, and thereafter be available to answer questions. The conference will be held in English.

The presentation audiocasts can be accessed via the following link:

Inderesin tiedote:

https://www.inderes.fi/en/tiedotteet/invitation-presentation-bicos-preliminary-q2-performance-2022

2 tykkäystä

Tässä ABG:n tuoreesta rapsasta pääkohdat. Target laskettu 35 SEK (210) ja suositus laskettu HOLD (BUY).

Preliminary Q2 figures and credit provision

Preliminary Q2 sales were SEK 543m (-9% vs ABGSCe 594m) and EBITDA

was SEK -20m (-165% vs ABGSCe SEK 31m). The organic growth was 9%

(ABGSCe 31%), driven by a slowdown in emerging biopharma and biotech

related to the recent macroeconomic challenges. Management has also

reviewed historical accounts receivables, which has led to a more

conservative sales process and a credit provision of SEK -59m (SEK -43m

net of COGS), which means reported EBITDA in Q2 will be SEK -63m. The

provision relates to sales in 2021 for which customers have not been able to

pay, due to the changing market environment. The products have been

returned and will be sellable to other customers. Furthermore, management

will implement a cost reduction programme to reduce expenses by SEK

100m on an annual basis, with full effect from Q1’23.

Uncertainty on historical and future financials

To us this announcement is a major concern, which is exacerbated by the abrupt

departure of the CFO three months ago. With historical financial performance

now in question, we are uncertain what the true level of demand is from

customers that can make payments. Furthermore, we believe that further credit

provisions cannot be ruled out, such as from sales recorded over the last 6m that

have not yet become overdue. The Q2 figures are another concern, with the

market slowing down while BICO’s costs continue to increase rapidly.

Down to HOLD on uncertainty and balance sheet concerns

We revise our estimates and turn more cautious, assuming 15% organic

growth for ’23e-’24e. Despite us assuming only modest opex growth

(~8%/y), and a large reduction in capex (SEK 500m to SEK 200m), we do

not expect BICO to generate a positive FCF until ’25e. With current cash of

SEK 1.2bn and SEK 1.5bn in convertible debt maturing ’26e, and SEK 470m

in earn-outs to be settled in ’22-’24e, we believe there is risk of an equity

issue. Considering the material uncertainty to operations and financials, we

downgrade to HOLD (BUY) with a new TP of SEK 35 (210).

Financial concerns, down to HOLD

We believe that Friday’s announcement raises several questions:

- If BICO’s financial results for 2021 were based on sales to customers not able

to pay for its products, what is the true financial performance of the company? - Has management taken any precautionary measures for sales that occurred

over that past six months, but where products are not yet overdue? Will there be

further credit provisions? - Why have customers purchased products they cannot afford, but refrained from

using them so that they now (6-18 months later) remain in a re-sellable

condition? - Why has this issue not been identified earlier, such as in February, when

management “initiated measures to improve the invoicing process to reduce day

until payments”? - How does this relate to the sudden departure of the CFO in April?

- To what company (or companies) do these issues relate? Was the company

recently acquired or was it in the Group when this happened?

Concerning developments in Q2

Beyond the sales to questionable customers, we are concerned about the

developments in Q2 where the market seemingly saw a slowdown while BICO’s

cost continued to increase. Assuming that the gross margin was 73%, cash opex

increased to SEK ~415m in Q2, which corresponds to a 15% q-o-q increase from

Q1. It should also be noted that this was during a period when management guided

that it would see only modest cost increases during the year. In our view, this

development was not addressed in the press release. Assuming that capex is

similar to previous periods, we believe the underlying EBITDA indicates a negative

FCF in the range of SEK -100m to SEK -150m in the quarter. With this in mind, we

believe the annual cost savings of SEK 100m are not enough to turn around the

development.

7 tykkäystä

Riskillä lisäilin isosti kun käytiin kolmenkympin alapuolella, heinäkuun kurssilasku tuntui niin yliampuvalta. Aika hyvä raportti ja tekemisen suunta näyttää taas erittäin hyvältä. Tätä kirjoittaessa +38% reaktio rapsaan ![]()

6 tykkäystä

Bico heräilee koomasta pyrähdyksittäin. Tätä kirjoitettaessa on kaikkien aikojen yhden päivän kurssinousu.

Eli Sartorius ostaa 10% siivun Bicosta ja ne ovat uusia osakkeita, jotka liudentavat omistusta. Paradoksaalisesti tämä osakeanti aiheutti osakkeen kasvupyrähdyksen. On ainakin minulle mysteeri, miksi tällainen raju kurssireaktio. Olisiko markkinoiden yli-innostumista? Ainakin yhtiö saa runsaasti kassavarantoa tämän annin seurauksena, joten kasvun tavoittelu voi jatkua ja ehkä aiemmin suunnitellut supistustoimet ovatkin tarpeettomia tulevana vuonna? Aika näyttää.

The Board of Directors of BICO Group AB (publ) (“BICO” or the “Company”) has exercised the authorization granted by the Annual General Meeting to issue up to 6,408,626 class B shares (“New Shares”) in full, equivalent to ten percent (10%) of outstanding shares in the company

Mahdollisesti kurssireaktio voisi selittyä sillä, että Aasian markkina avautuu aivan eri lailla kuin aiemmin. En tunne Sartoriusta yhtään, joten tämän vaikutusta on vaikea arvioida, mutta jos kurssireaktio on oikea, tällä voi olla kouriintuntuva positiivinen vaikutus tulevaan liikevaihtoon.

In conjunction with the Share Issue, BICO and Sartorius have agreed on a comprehensive technology as well as sales and marketing cooperation. As part of the partnership, both companies will enter into a research & development collaboration relating to 3D cell printing and associated technologies as well as digital solutions for cell line development workflows. Additionally, it was agreed that Sartorius will become a distributor of BICO products in the Asia-Pacific (APAC) region.

5 tykkäystä

Ja takaisin kanveesiin ![]()

BICO Group AB (publ) today announces the decision to impair goodwill in Ginolis totaling SEK 625 million, ahead of the year-end report 2022 to be published on 22 February 2023.

3 tykkäystä

Holy shit. Klo 10 on tulossa turpajuhlat… ![]()

1 tykkäys

Klo 7.00 julkaistu tilinpäätös. Mielenkiintoista nähdä mitä markkina tuumaa.

1 tykkäys

Tässä ilmeisesti jotain juttua Bicosta, mutta näkyy vain tilaajille.

Tätä heinäkuun alkupuolella julkaistua uutista tänne ei oltu vielä laitettukaan:

Next step in Sartorius partnership finalized: several sub-sales and distribution agreements as well as R&D project agreements have been signed

Eli touko-kesäkuussa ovat solmineet sopimuksia Sartoriuksen kanssa ja sen myötä kesäkuun alun jälkeen osakekurssi onkin noussut jo +30 %.

6 tykkäystä