Täähän voisi olla hyvä kohde. Vahvat ja tunnetut brändit ainakin täällä Suomessa sekä se että paskapaperille on myös silloin tarvetta kun se tavara osuu tuulettimeen ja taloudella ei mene hyvin. Täytyy ottaa seurantaan ja vähän tarkemmit tutkia. Mikä mahtaa olla tuossa viime aikojen kurssikehityksessä takana?

Mielenkiintoista. Onko tämä siis inderesin asiakas?

Musta nyt tuntuu, et kaikilla vähänkään nousussa olevilla osakkeilla tuo loppuhuipennus tällä hetkellä samannäköinen. Eihän sitä graafin muodon mukaan pitäisi sijoittaa, mutta tulee heti huonot vibet

Excellent company. I have been a shareholder of Essity after its spinoff from SCA.

This company ticks all my boxes: defensive, good leadership, brands etc. Only problem, as with the rest of the market, a bit pricey for my taste at the moment, even though SEK is rather weak. I rather own Essity than Kimberly-Clark.

This is a long term investement for me (as is also Visa, Sampo, Novo Nordisk). Will increase my share holdings in the future for sure.

If someone wants to add Essity be sure to follow insider trading (to get an idea of a good entry point), as their have been in recent years rather broad activity (not only the usual suspect buying like the CEO) and most have been adding (very few if none have been selling). I think the latest purchase was around 270-280 SEK.

I usually use Finansinspektionens register to look for insider trading patterns.

Essity is definitely a company that I would like to own. I completely agree with you, the stock seems to be a bit pricey despite the decent growth in net sales. I will most likely open my Essity position if the share price drops below 270 SEK.

At least aging population, longer life expectancy, growth in world population and income(Essity is present on emerging markets) as well as increased awareness of the importance of hygiene(emerging markets). How well these trends will translate to revenue growth for Essity is of course a more difficult question.

STOCKHOLM (Nyhetsbyrån Direkt) Louise Svanberg, styrelseledamot i Essity, har på onsdagen köpt 3.100 B-aktier i hygienproduktsbolaget.

Det framgår av inrapportering till Finansinspektionens insynsregister.

Köpet gjordes till kurs 306 kronor och var därmed värt nästan 1 miljoner kronor.

Louise Svanberg, som tidigare varit vd för spårkursföretaget EF och som 2016 valdes in i Essitys styrelse, äger 15.000 aktier i Essity, enligt bolagets hemsida. Det framgår inte när den uppgiften uppdaterades senast.

Viime kuun lopulla julkaistu Essityn tulos oli aika linjassa edelliseen vuoteen verrattuna. Osakkeen kurssi on madellut, vaikka yritys on vakavarainen ja omaa vakaan myynnin. Ehkäpä yritys on hiukan tylsä… Olen miettinyt, että pitäisikö luopua omistamistani osakkeista ja hakea parempaa tuottoa.

Essity is by its nature a ‘boring’ company. But for me its one of the best quality companies in the Nordics (I am a value, long-term investor.)

If you have a long-term time horizon and have the patience to wait owning this share it will eventually prove to be successful.

The short term catalyst: the end of the worldwide corona lockdowns, which will increase the use of Essity products (in airports, in hotels, restaurants, schools etc). Corona will create more awareness of hygiene products. Here the strong Essity brands will prosper.

The long-term catalyst is the fact that people in the western (rich) socities are living longer and will drive the demand of Essity related products.

Any thoughts about the Q1 report and acquisitions? For me the company seems interesting and boring at the same time Kind of worrying that sales are way lower than Q1 2019. 2020 is naturally a tough comparison.

Essity will have a couple of rough quartals ahead of them. That is given, due to lockdowns and costs concerns driven by mass price increases.

But that said, Essity is doing everything right, and if I want to be in this space I prefer Essity over KMB, which is heavily in debt (as it uses the American way to boost it share price by spending way to much money on share buy backs).

I am bullish on the long-term view of Essity. But owning Essity as you indicated requires patience, which is hard to find among investors these days.

edit: I do like that Essity pursues (‘small’) bolt-on acquisitions, rather than big, as these usually do not have a favorable outcome (especially) for the buyer.

Paljon on ehtinyt tapahtua viimeisimmän kirjoituksen jälkeen. Kolmen vuoden aikana Essity on monipuolistunut tekemällä lukuisia yritysostoja:

2021

-ABIGO Medicalin ja Aseleo Caren osto kokonaan itselleen (aikaisemmin osaomistus).

-Productos Familia S.A. omistusosuus nostettiin 95,8%:iin.

-Johnson&Johnson:lta ostettiin urheiluteippibrändit Coach, Elastikon ja Zonas.

-Kipsiliinojen valmistajan AquaCast Linerin osto.

-Haavanhoidon yhtiö Hydoferan osto.

2022

-Tork -brandin omistavan pyyhintäyhtiön Legacy Converting, Inc.:n osto.

-Modibodi, erikoisalusvaate (leaking proof) -yhtiön osto.

-Knix Wear Inc. erikoisvaate (leakproof) -yhtiön osto.

Divestointejakin on tehty. Essity myi Venäjän liiketoimintansa v. 2023. Onkohan verrokit KMB ja PG tehneet sitä vieläkään? Tuorein divestointi on Hong Kongissa listatun Vinda -tytäryhtiön myynti. Essity on omistanut Vindasta noin 50%. Ostotarjous odottaa ymmärtääkseni vielä lopullista hyväksyntää, mutta toteutuessaan se tuo yhtiön kassaan 19bln SEK.

Mielikuva Essitystä yhdistyy helposti vielä Lotukseen, Tenaan tai Liberoon. Yhtiön strategiana on ollut vähentää WC-paperin ja vaippa -liiketoiminnan osuutta ja lisätä korkeamman marginaalin uusia tuotteita, lähinnä yritysostoin. Jos pitää Kimberly-Clarkia tai P&G:ia liian kalliina tällä hetkellä, niin Essity alkaa olemaan varteenotettava holdilappu huomattavasti edullisemmilla tunnusluvuilla ja kohtuullisella velkaprofiililla. ROCE vuoden 2023 tilinpäätöksen mukaan oli 14,4%. Osinkoa korotettiin ja on 7,75 SEK.

2023

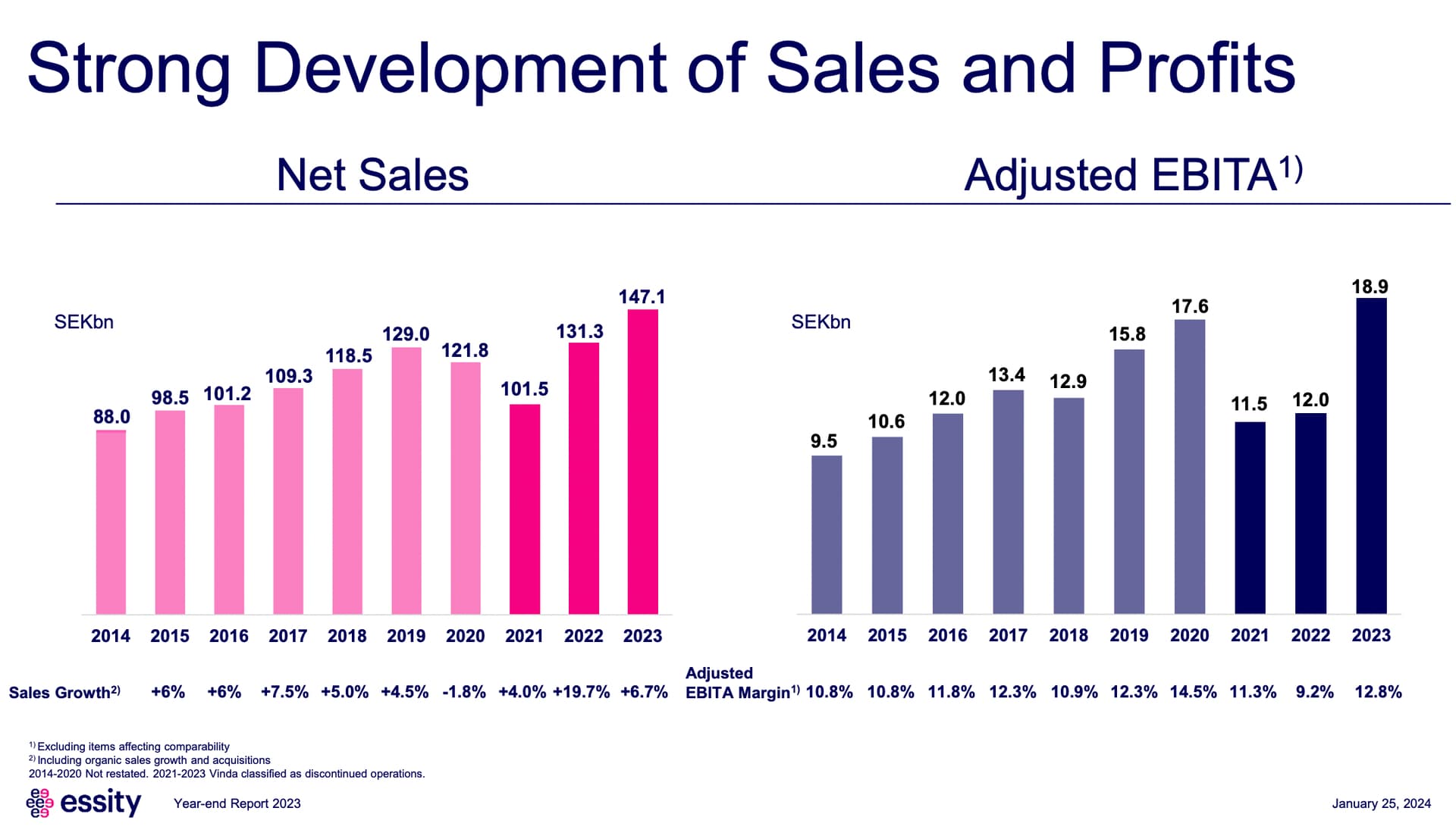

• Net sales increased 12.1% to SEK 147,147m (131,320). Sales growth, including organic sales growth and

acquisitions, amounted to 6.7%, of which volume accounted for -3.7%, price/mix for 9.5% and acquisitions

for 0.9%.

• Operating profit before amortization of acquisition-related intangible assets (EBITA) increased 68% to SEK 16,607m (9,876)

• Adjusted EBITA increased 57% to SEK 18,898m (12,047) and the adjusted EBITA margin increased 3.6 percentage points to 12.8% (9.2)

• Profit for the period continuing operations increased 84% to SEK 9,517m (5,165)

• Earnings per share continuing operations increased to SEK 13.44 (7.28) and adjusted earnings per share continuing operations increased 51% to SEK 17.56 (11.60)

• Operating cash flow increased 130% to SEK 17,685m (7,680)

• Return on capital employed increased to 14.4% (8.9) and the adjusted return on capital employed increased 5.5 percentage points to 16.4% (10.9)

Essityllä on erittäin laadukaita liiketoimintoja. Yhtiö tuotiin vähän liian kovalla arvolla pörssiin, mutta nyt valuaatio painunut järkeville tasoille. Mikäli kasvu jatkuu yhtiön arvo nytkähtänee jossain kohtaa perässä.Pitäisin samanlaisen kasvuprofiilin omaavana yhtiönä kuin Huhtamäki. Ei mitään isoa osinkotuottoa lähtötasona, mutta aika merkittävä kasvuoptio joka hyvin toteutunut historiassa.

Pidän henkilökohtaisesti tälläisistä yhtiöistä joissa tuotteisto pysyy suhteellisen samanlaisena vuodesta toiseen. Korkoa korolle efektiä mukava rakentaa sellaisen päälle jota ei tarvi joka vuosi innovoida uudelleen.

Essityn kohdalla näki kuinka kuluttaja maksaa lopulta inflaation ja vahvoilla yhtiöillä hinnoitteluvoimaa

Essity on hyvällä tavalla tylsä laatuyhtiö, että sen uutisia/tiedotteita ei tule seurattua kovinkaan reaaliaikaisesti. 4.3. tiedotettiin, että viranomaiset ovat hyväksyneet Vindan osuuden myynnin tarjoajalle. Essity saa myynnistä aikaisemmin tiedotetun 19mrd SEK.

Jatketaan lähes kuollutta keskustelua laatuyhtiön parissa.

Essity jatkanut tasaista menoa. Osinko kasvaa jälleen ja tase senkun paranee. Yhtiöllä alkaa olla lihaksia ostaa joko enemmän omia osakkeita tai lähteä täydentäviin yritysostoihin. Mieltäisin pohjoismaisista yhtiöistä ehdottomasti parhaimmistoon. Tappavan tylsä ja tuottava firma. Strategia kasvaa perinteisistä bulkkituotteista korkeamman lisäarvon tuotteisiin toiminut. Esim. Health & Medical segmentti pystyi 18% ebita marginaaliin jota pitäisin erinomaisena.