One casino to rule them all

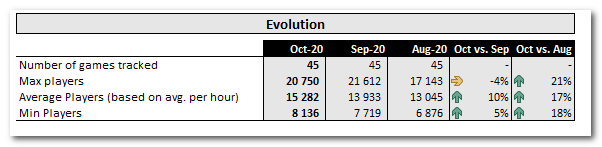

Evolution’s report came in well just as I thought, ie with the eyes of the market very strong. For natural reasons, there was a general perception that this quarter would grow significantly slower sequentially from the second quarter, which broke all records with 50% growth against the same quarter the year before and very strong 11.4% sequentially. Analysts believed in young. 5% sequentially but it became very strong 9% (48% y / y).

Profit doubled during the year and increased by 13% sequentially, which is why the margin rose further to 64.8% From 63.2% in the previous quarter and 51.2% in the same quarter last year. The profit margin is now 56.7% (42%). However, something that is barely reported in the financial media is the sequential profit increase. As much as 76% of the sales increase from Q2 was a pure profit. Very welcome was the news that the studio in Pennsylvania has now opened and the one in Kaunas has been completed at record speed. EVO will soon cut a new studio in the quarter.

North America is today 7% of EVO after a growth of 51%, ie in line with the company as a whole. Behind this, however, lies a fantastic development in New Jersey and the great handicap they had from not having the studio in Pennsylvania in operation. According to its official statistics, this new state has thrown itself into online casinos and sports since it was legalized a year ago. However, one should probably not miss the probably very strong start EVO gets as the online casino in Pennsylvania, as I said, is in full swing and many of course have been waiting for live to get there as well. EVO still has the entire live casino market in the United States.

It is hard to believe otherwise than that the ever-increasing gap between revenues and costs, especially staff costs, will continue to increase even if the company needs to hire to fill the tables that had to be closed this spring. Or in other words, the share of costs in sales will continue to fall at the same time as revenues increase tirelessly. This is how exponential profit growth is created.

To sum up the almost four years that I have followed EVO very closely, it is not just a matter of enormous growth but an effective displacement of competition, which is undoubtedly even more important for the future. Even if the competitors in some cases also grow, it is at a clearly lower rate than EVO, which has made it wrong today to talk about competition in the classical sense. There is again a large second in the market that fights in principle on an equal footing with Evolution on customers. Admittedly, Playtech is the second largest, but in reality this means that their live business is around 10-15% of EVO’s today. The fact that it even has such a large share is largely due to the fact that their customers are usually locked into long-term agreements that prohibit them from bringing in other providers of live casinos.

Although Playtech as well as the really small players also create new games, it is usually shameless and poorly executed copies of EVOs that appear a couple of years after the original. This at the same time as EVO first launched Lightning Roulette almost three years ago which was a resounding success by the standards of the time, since Monopol Live which has grown its number of players even faster to this summer having released the flagship Crazy Time which the other day had 6000 simultaneous players after just a few months. Playtech’s best games, by comparison, have a few hundred simultaneous players.

The conclusion one must reasonably draw from this is that today it is EVO that “disrupts” the classic casino industry, ie traditional table games in physical premises. They have succeeded incredibly much better than their competitors in recent years and the players also go very clearly in online casino from RNG games to live, so it is no exaggeration to say that it is basically EVO that drives this. Of course, there are competitors and these will hardly be fewer, but to claim that any company with a few percent of EVO’s turnover and significantly worse customer offering would be involved in the disruption would be misleading. These companies only depend on the trend that EVO is pursuing.

The importance of the lion’s share of the money ending up in EVO’s pockets when classic casino on a global level goes from physical premises to online is enormous. This of course presupposes that EVO can continue to maintain this dominance, but everything indicates that today. With the acquisition of NetEnt, which is a world leader in slots, you can get over this vertical very painlessly, even if NetEnt’s dominance in slots is not at all at the level EVO’s is in live. This in combination with Evolution’s constant expansion of the range of live to the latest bingo and craps means that you slowly but surely fill all the gaps in the range.

Of course, a physical casino will always exist, whether we are talking about classic palaces or simple bingo halls. However, there is nothing at all that would indicate that not least half of the turnover will move to online in the foreseeable future. Just like with anything else that can be digitized. The speed at which this occurs has also increased significantly due to covid. Anyone who follows the industry can read almost daily about the problems these once proud gaming metropolises and casino moguls have when traffic has become a staple of what it once was.

This is a classic disruption as Clary Christensen described it - a new and potentially significantly better technology arrives which is initially limited (for online casinos by the bandwidth) but over time technology development solves this and the transition takes place faster and faster. The old industry first dismisses this threat (“Who wants to sit at home in front of the computer and play roulette instead of coming here and playing for real, drinking and watching entertainment?”).

In time, it is the upstart who laughs instead. The old companies go bankrupt and new players who can perform the service exponentially much more efficiently take over more and more of the turnover and almost the entire profit. FAANG in a nutshell. Anyone who refuses to see where we are going, and these have not exactly been few in Finanssverige, misses the train.

Tässä nyt puolitoista päivää tästä yhtiöstä lukeneena saa kuvan hyvin kunnianhimoisesta tekemisestä. Vaikka kilpailijat tuntuvat nielevän pölyä pahasti takana, painaa EVO entistä kovempaa menemään. Jatkuvasti pyritään tekemään kaikkea aina vain paremmin. Ei jäädä laakereille lepäämään ja tuudittauduta turvalliseen johtoasemaan. Kokoajan on putkessa tulossa uusia pelejä, markkinoiden avautuessa ollaan yhä nopeammin laittamassa seuraavaa studioita pystyyn. Prosesseja hiotaan entistä tehokkaammiksi, mutta laadusta ei tunnuta onneksi tingittävän.

")