No varsinaisia verrokkeja noista ei ole kuin Playtech, loput Evon sekä Kambin asiakkaita.

4 tykkäystä

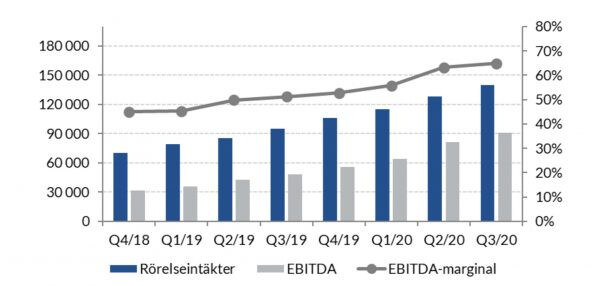

Tässä ilmeisesti kyse dedikoitujen pöytien käyttöasteesta koronan jälkimainingeissa. Jos oikein tulkitsen, niin tämänkin pitäisi tuoda boostia Q4-lukuihin kaiken muun ohella…

10 tykkäystä

Days range 810-856sek. Ei vissiin osata päättää oliko demokraattien värisuora hyvä vai huono asia Evolle ![]()

Toinen vaihtoehto voi olla, että odotetusti nyt luovutaan viime vuoden nousijoista ja ostetaan noususta jälkeen jääneitä arvolappuja.

6 tykkäystä

Curacaon lisenssillä oleva nakkikioski. Curacaon lisenssi on melkein surkeimpia kuluttajansuojalta ja pikku kasinoita lisenssin alla on satoja. Tällä ei siis käytännössä mitään merkitystä Evon sijoituskeissin kannalta.

Olis suotavaa vähän avata asiaansa, jos se ei käy selväksi esim. twiitistä itsestään.

11 tykkäystä

https://www.fredagskronikan.se/2021/01/08/evolution-21/

lisäys: translator käännös

After Evolution Gaming had a very nice 2020, it is perhaps natural that many people wonder if they can keep pace in 2021. I think it may be a bit strange approach because the conditions for EVO’s success in the past year were created in the years before, exactly like the successes of 2019, etc. With this year’s growth and investments, on the contrary, the conditions are set for continued good development.

The company’s operations are such that it is the investments in new popular games and greater studio capacity and, of course, the conclusion of new agreements with operators whose customers also like these games that over time create ever higher sales. With higher sales, the margin rises all other things being equal, as the business is largely extremely scalable.

In 2020, it was clear that more and more people began to follow the number of players on EVO’s most popular games, not least among analysts and managers. This is positive because it increases transparency among all market participants, but was previously something that only we most committed owners dealt with. All measurements I have seen have shown an accelerating growth during the fourth quarter, which bodes well for a good report. It is important to know, however, that the number of players is not completely correlated with the revenue because EVO also has revenue from its dedicated tables and because there is different profitability and size of the bet in different games with Blackjack as the big deviator. The fact that from this week Flutter’s very large British business also offers its customers EVO’s games will help growth in the coming quarters.

However, making a more detailed prediction about 2021 is a little more difficult than before due to NetEnt being integrated with EVO from 1 December. I think the conditions for success with this acquisition are excellent. NetEnt’s slots are the world’s best and the company is now doing excellently, not least thanks to its own acquisition of Red Tiger. In addition, we have the management’s now somewhat legendary ability to keep costs down, which comes in handy as NetEnt’s costs are clearly higher as a share of revenues than “old EVOs”. Finally, as is well known, the acquisition was paid for in full with shares and no indebtedness was avoided.

Obviously, the staff reductions went hard, among other things, they immediately shut down NetEnt’s live operations. This is important because NetEnt has clearly higher personnel costs as a percentage of sales than EVO. It will also be important that NetEnt’s Other costs fall, but you are probably well on your way there when you close offices and studios.

With 59.4%, NetEnt’s EBITDA margin was almost in line with EVO’s at 64.8%, but the operating margin is clearly lower at 39.4% against EVO’s 59.7%. A result of NetEnt’s high depreciation, which in part comes from the acquisition of Red Tiger, most recently these were 21% of revenues against EVO’s 5%.

It is important to keep in mind, however, that the “old EVO” is of course significantly larger than NetEnt. NetEnt’s sales in the third quarter were 36% of EVO’s and the profit only 21%. So it is not a “merger of equals” but EVO swallows NetEnt. In total, the whole will be bigger than the parts, I think, and as I wrote about earlier, the merged company will now have an unbeatable offer comprising the world’s by far the best live, slots and even RNG casino.

This whole will very likely continue the successes both east and west in 2021 and beyond. In any case, I have never felt more secure. That the share is now included in OMXS30 and EVO is steadily climbing upwards among Sweden’s largest companies, currently in seventeenth place, gives a completely different visibility both in Sweden and abroad.

25 tykkäystä

13 tykkäystä

Sopii hyvin sekä Kambi että Evo omistajana! Tosta jää kyllä auki vielä että onko vasta kuvernöörin toive että sallitaan vai päätös asiasta? Olan sanojen avataan, englanniksi calls for (aikomus). No sinänsä trendi on sama eli enemmän ja enemmän osavaltioita tulee sallimaan.

Tässä on myös sellainen dominoefekti joka menee niin että jos osavaltio vieressä sallii niin alkaa pakottamaan muitakin koska pelko on että omat asukit vierailevat sitten naapuriosavaltiossa. Itä-rannikolla menee hyvin selvästi tämän kaavan mukaan. Ensi New Jersey, siten New York jossa Cuomo nimenomaan sanoi yhdeksi syyksi New Jerseyn. Connecticut on sitten Nykin naapureita ![]()

7 tykkäystä

Jos ja kun Connecticut vaatii, että livepelejä striimataan fyysisesti heidän osavaltiossaan tietää se jälleen uutta studiota.

Aika iso etu Evolutionille, että alkaa olla jo melko rutiinia pistää näitä pystyyn tehokkaasti. Mietin vain, että missähän menee osavaltion koossa raja, ettei enää kannattaisi laittaa studioita pystyyn?

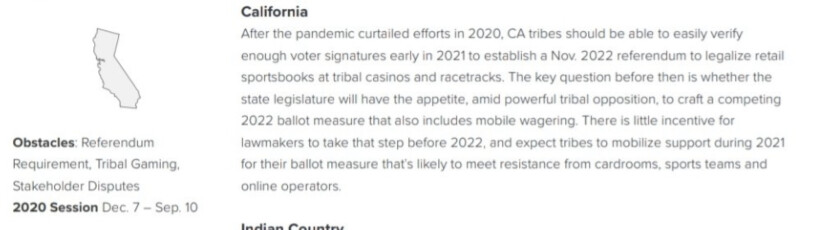

Sitten kun California tai Texas näyttää näille vihreää valoa ostan pullon kuohuvaa. List of U.S. states and territories by population - Wikipedia

5 tykkäystä

Kambi ketjussa näitä enemmän mutta tossa viimeisimpiä arvioita sekä Kaliforniasta että Texasista. Texas olisi ehkä avaamassa 2021, Kalifornia 2022.

5 tykkäystä

New Yorkin kohdalla tuosta oli kommenttia; Koronan takia osavaltioiden talous kuralla → kiihdyttää online uhkapelien sallimista koska niistä saadaan helppoa verotuloa vs. nykyinen tilanne jossa pelit tapahtuvat laittomasti.

15 tykkäystä

https://mobile.twitter.com/Rastapo09963637/status/1347595952388005888 taas uudet ath lukemat pelaaja määrissä. Kyllä kelpaa.

4 tykkäystä

Olen samaa mieltä, kelpaa! Tosin pitää rehellisyyden nimissä muistaa, että onhan sitä kasvua hinnoiteltu jo aika riskisti sisään…

4 tykkäystä

Brittien lockdownit puskee läpi tilastoihin williamhillillä. Eiköhän ath lukemia kolkutella tulevina viikkoina useamminkin ![]()

8 tykkäystä

Spotify, Evo, Embracer, Storytel, Kambi… Oikeastaan ei yllättänyt tuo lista yhtään.

8 tykkäystä

Varmasti pitää muistaa kallis hinta, mutta EVO on onneksi sieltä päästä missä tulos kirii kokoajan arvostuskertoimia kiinni, toisin kun esimerkiksi sähköautofirmalla joka alkaa T-kirjaimella. ![]()

![]() Evossa ei siis mielestäni ole ainakaan merkkejä kuplaantumisesta, vaikka ripeää on nousu ollutkin.

Evossa ei siis mielestäni ole ainakaan merkkejä kuplaantumisesta, vaikka ripeää on nousu ollutkin.

14 tykkäystä

PEG-luku tuloskasvusta laskettuna on kyllä hyvä arvioidessa tällaista pitkää kovaa kasvu-uraa tekevää keissiä. PEG < 1 on tällaisesta halpaa ja mielestäni tuossa oltiin syksyllä ja ei varmaan nyttenkään kaukana… tällaista lappus voisi hyvinkin hinnoitella 1.5 tai jopa 2.0 kertoimella kunhan usa sijoittajat heräävät.

Olis kiva saada Redin rapsa niin näkis niiden arviota pitkän aikavälin tuloskasvusta pro forma.

16 tykkäystä

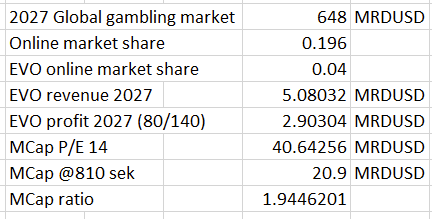

Tein tästä analyysista pienen excel koosteen. Eli jos voittomarginaali on viime raportin mukainen 80/140 ja P/E on 14 vuonna 2027, niin voittoa tulisi 94,4 % nykyhinnalla 810 SEK. Ei kuulosta kovin houkuttelevalta. Online market shareja ja P/E lukuja muuttamalla saa tietysti tästäkin paljon houkuttelevamman.

8 tykkäystä

Eli 10%:n vuosituotto + osingot? Pitäisin tuota varsin houkuttelevana. PE 14 oletus tuntuu aika pessimistiseltä.

7 tykkäystä