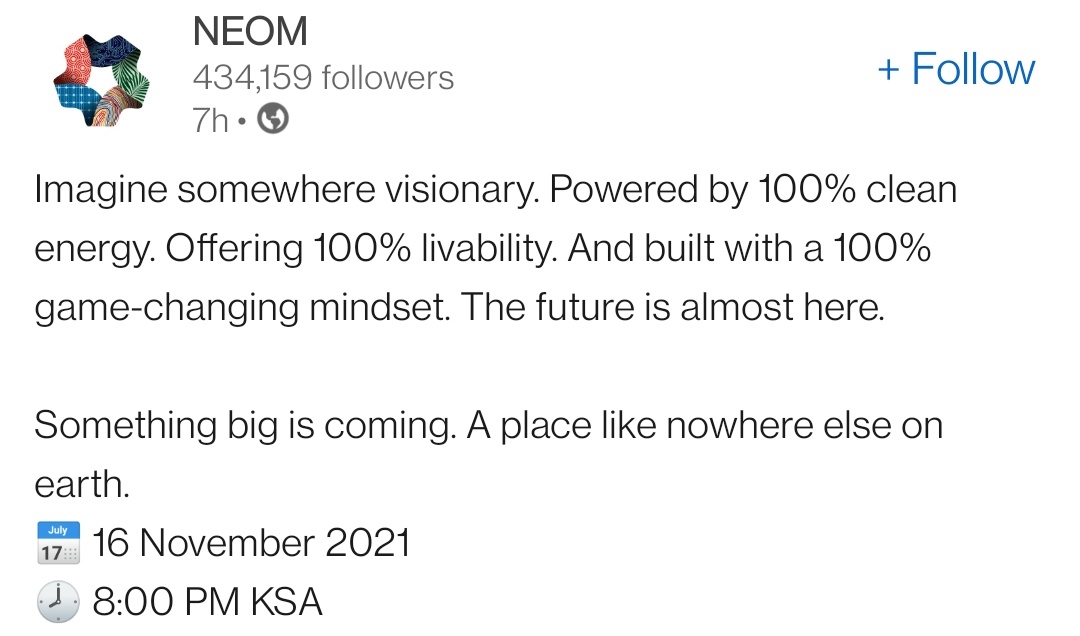

Mielenkiintoisia uutisia saattaa olla tiedossa.![]()

67 tykkäystä

Tuntilaskuri löytyy tuolta, reipas 66 tuntia niin jotain kuuluu? ![]()

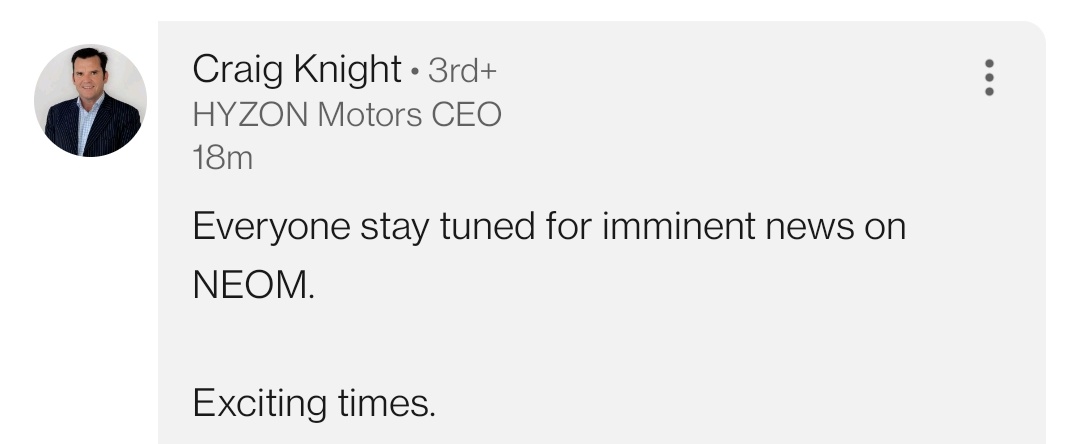

![]()

38 tykkäystä

Mistä tää screenshotti on otettu?

Edit: löysinkin sen linkedistä

4 tykkäystä

Mut mitä näistä ecokylistä ja viivan alle? Toki jos saa sinne myytyä muutenkin kuin pilottihinnoilla niin alkaa tuntumaan, mutta muuten on vain hypeä, IMO.

Kyllä näitä silti tarvitaan jotta tietoisuus leviää joten ehdottomasti plussaa ja on tärkeää olla osana tätä näkyvyyttä.

Jä tämä kylähän siis on ISO

18 tykkäystä

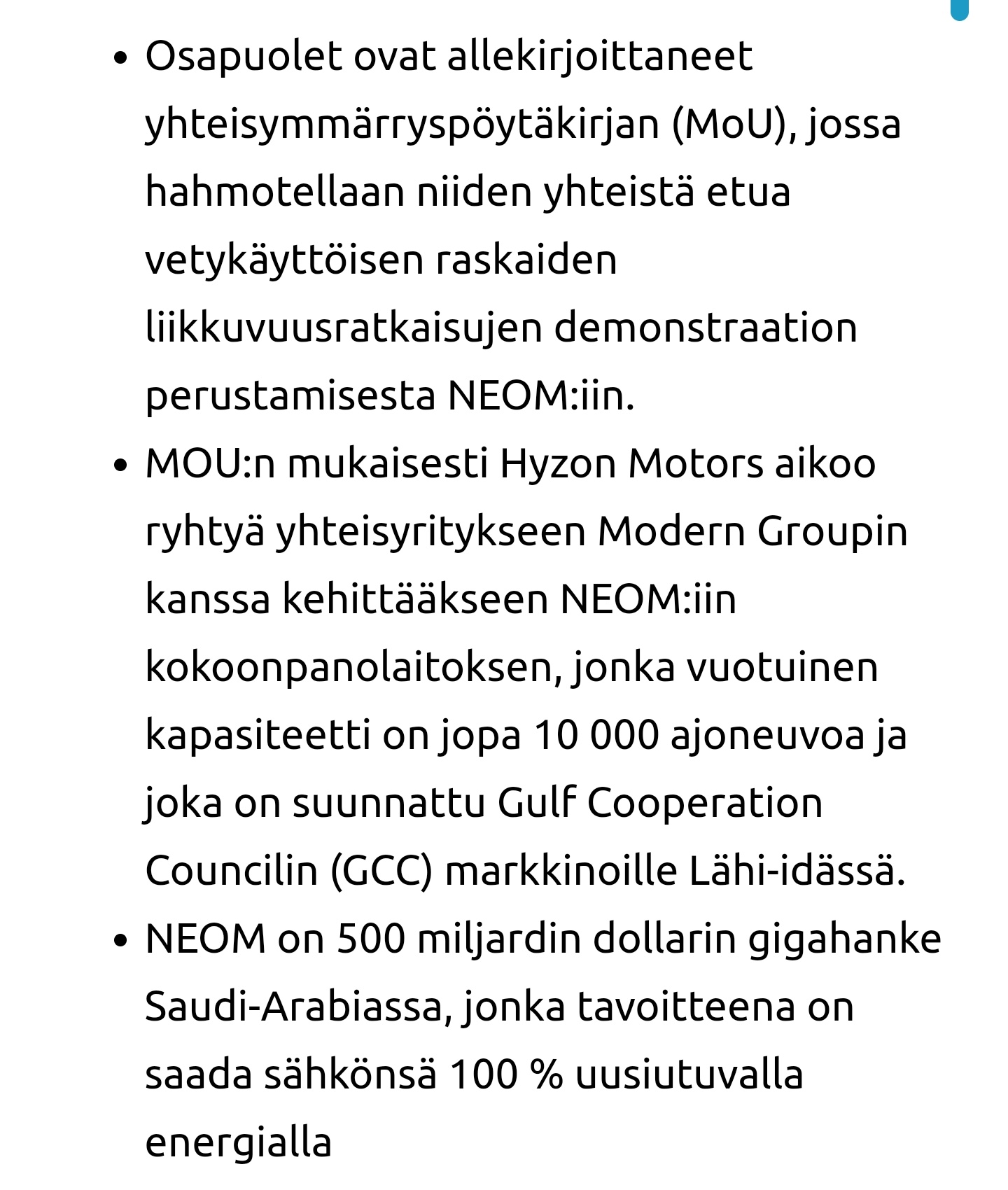

Neomissahan on aiesopimuksen perusteella tarkoitus tulevaisuudessa lyödä 10 000 Hyzonin ajoneuvoa kasaan / vuosi, eli tuossa alkaa sitten viivan alla näkymään jo aika suuria summia.

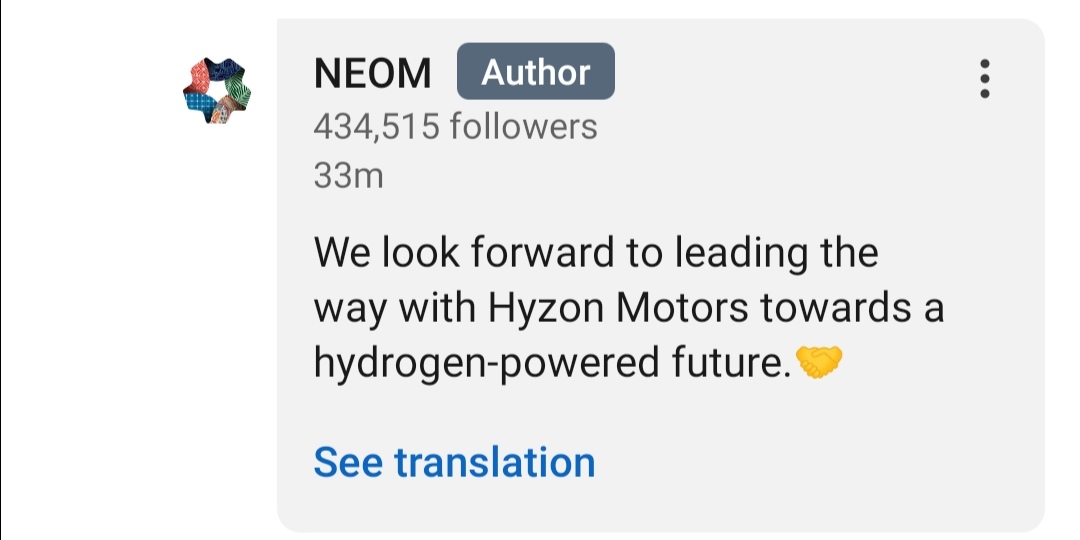

Following from the MOU, Hyzon Motors intends to enter a joint venture with Modern Group for the development of an assembly facility at NEOM with annual capacity of up to 10,000 vehicles targeting Gulf Cooperation Council (GCC) markets in the Middle East

42 tykkäystä

Mun mielestä just noi isot tulevaisuusluvut on sitä hypenluontia. Tuommoiset voi myös kostautua jos ne ei toteudu tai niistä joudutaan leikkaamaan?

5 tykkäystä

Jos aiesopimuksen suunnitelmat ovat edenneet, Neomiin perustetaan Hyzon Motors Middle East yhdessä Modern Groupin kanssa.

Tuotantokapasiteetti tarkoitus tosiaan olla tulevaisuudessa 10000 ajoneuvoa. Ei tarkoita että joka vuosi myydään sen verran, mutta tehdas mitoitetaan sen mukaan, että se on mahdollista.

Kohdemarkkina GCC, eli United Arab Emirates, Saudi Arabia, Qatar, Oman, Kuwait and Bahrain.

Eiköhän tuossa potentiaalia ole ihan tarpeeksi ja hype olisi ihan perusteltua.

39 tykkäystä

Puhelussa mainitsivat suuremmasta kysynnästä ja suuremmasta myynnistä ensi vuonna, mitä oli ennustettu. Voisiko tähän liittyen olla, että ensi viikolla ilmoittavat uutta myyntiä?

Kivahan näitä on spekuloida. ![]() Noh, muutama päivä niin selviää homman nimi. Lähtölaskennat ja kaikki, jotenkin tuntuu et kyllä tuo vaikuttaa isolta asialta.

Noh, muutama päivä niin selviää homman nimi. Lähtölaskennat ja kaikki, jotenkin tuntuu et kyllä tuo vaikuttaa isolta asialta.

29 tykkäystä

Ymmärsin että yleisellä tasolla kysyntä/kiinnostus suurempaa, toki johtaa tarjouksiin ja sitä kautta kauppoihin. Mainitsivat myös että viivästystä voi olla kun infraa ei vielä oikein ole mutta enää ei tarvitse selitellä ja perustella miksi vety.

12 tykkäystä

Itse näkisin asian niin, että tuo nyt on vaan jonkinlainen valistunut arvio ja kertoo lähinnä mittakaavaa (mahdollisesta) potentiaalista. Se, että kuinka paljon näille antaa painoarvoa omissa sijoituspäätöksissään on sitten jokaisen itsensä päätettävissä.

Ilmeisesti tässä nyt kumminkin tulossa suurempia uutisia kyseisen keissin kohdalta, muutaman päivän päästä. Hienoa kumminkin nähdä, että tarina vaikuttaa etenevän suotuisasti. Mielenkiintoista tulee kyllä varmasti olemaan seuraavat pari kuukautta.

21 tykkäystä

Voisikohan tämä liittyä Neomin ilmoitukseen ![]() Hakevat töihin työmaa johtajaa vai mikä tuo nyt tarkasti suomennettuna olisi. Kuulostaa melkoisen isolta projektilta tuo .

Hakevat töihin työmaa johtajaa vai mikä tuo nyt tarkasti suomennettuna olisi. Kuulostaa melkoisen isolta projektilta tuo .

The incumbent is accountable for the Construction Management of the NEOM Green Fuels Project, including:

a 2,500 MW () solar power plant;

a 1,250 MW () wind farm;

battery storage facilities for power storage;

an electrical grid system to connect the various facilities and (back-up) connection(s) to the primary electrical grid;

a 2,2 GW () hydrogen electrolysis plant;

a 103,000 Nm3 () per hour (N2) air separation unit (ASU);

hydrogen and nitrogen storage facilities;

nameplate capacity of 1.4 Mtpa () green ammonia plant and storage; and

a maritime offloading facility including a connection to the ammonia storage facility

() final capacity is subject to optimization and will be final when the EPC contract commences.

This Project is one of the largest and most complex capital projects for Air Products and is transformational for the organization and beyond. It will be the first industrial-scale mega Project providing a green energy carrier worldwide to contribute to the decarbonization of the industry. This position’s complexity is derived from the size and organization of this Project with an expected peak-manpower above 18.000 workers at various construction sites at the same time. Additionally, unique EH&S challenges are stemming from the individual specifics of the scope in each element.

The Construction Director will be responsible for leading and managing all aspects of Construction delivery throughout the project lifecycle. The Construction Director lead the Air Products construction execution organisation and will interface with project stakeholders, partners and corporate leadership to ensure compliance with Air Product’s expectations on safety, quality, cost and schedule performance.

Edit. On näköjään vuorokauden sisällä tullut muitakin töitä tarjolle ![]()

28 tykkäystä

En usko että tuo liittyy Hyzoniin mitenkään, vaan tähän NEOMin, Air Productsin ja ACWA Powerin jo viime vuonna julkaisemaan vihreään vetyyn perustuvaan ammoniakin tuotantolaitokseen.

Tuon investoinnin arvo on “vaivaiset” 5 miljardia, kun NEOMin koko investoinnin on arvioitu olevan 500 miljardia. Joten on siellä vielä pottia mistä jakaa muillekin.

13 tykkäystä

The joint venture project is the first partnership for NEOM with leading international and national partners in the renewable energy field and it will be a cornerstone for its strategy to become a major player in the global hydrogen market. It is based on proven, world-class technology and will include the innovative integration of over four gigawatts of renewable power from solar, wind and storage; production of 650 tons per day of hydrogen by electrolysis using thyssenkrupp technology; production of nitrogen by air separation using Air Products technology; and production of 1.2 million tons per year of green ammonia using Haldor Topsoe technology. The project is scheduled to be onstream in 2025.

Tuon yhteistyösopimuksen mukaan tavoite on tuottaa mm. elektrolyysin avulla 650 tonnia vetyä päivittäin, sähkön, typen ja ammoniakin ohella.

Voi liittyä välillisesti HYZONiin, koska HYZONin suunnitelmassa on tarjota kokonaisratkaisu, joka pitää sisällään myös riittävän vedyn saatavuuden.

20 tykkäystä

Miten tämän saa linkattua Nel Asa -ketjuun?

Nelille saattaa olla tarjolla isoa diilia tuohon liittyen: Haldor Topsoe and Nel ASA to offer end-to-end green ammonia and eMethanol™ solutions

4 tykkäystä

Nykyisellä hinnoittelulla ei ole mitään Neom lukuja arvostuksessa vielä otettu huomioon, koska jos otetaan vertailuksi nyt toimitetut 2 nuppia, jotka ovat olleet 500k pala. Tuo Neom siis tuottaisi yksinään tämän päivän hinnoittelulla 5 miljardia liikevaihtoa, jolloin tämä olisi arvostettu päivän kurssilla ev/sales x0,3 joka on aika alhainen. Mutta jos tuon Neomin takia kurssi nyt vetää Nikolat ja lähtee painelemaan avaruuteen tuon takia, niin juu silloin ollaan vaarallisilla vesillä kyllä.

Toinen negatiivinen puoli olisi se, että tuota Neomia on käytetty projektioissa, joiden perusteella spac arvotettiin alun perin. Silloin suuri osa oletetusta tulevaisuuden liikevaihdosta lepäisi tällaisen kortin varassa, mikä ei myöskään olisi hyvä juttu. Neom on siis MoU asteella ja mitään ei ole varmaa vielä, mutta jos sinne suuntaan saataisiin edes jotain virallista sopparia aikaan, vihjaa tämä ruusuisasta tulevaisuudesta, koska lähi-idässä riittää rahaa ja kun siellä haluttaan asioiden alkavan tapahtua, niin tosiaan raha puhuu sen verran, että asiat tapahtuvat.

47 tykkäystä

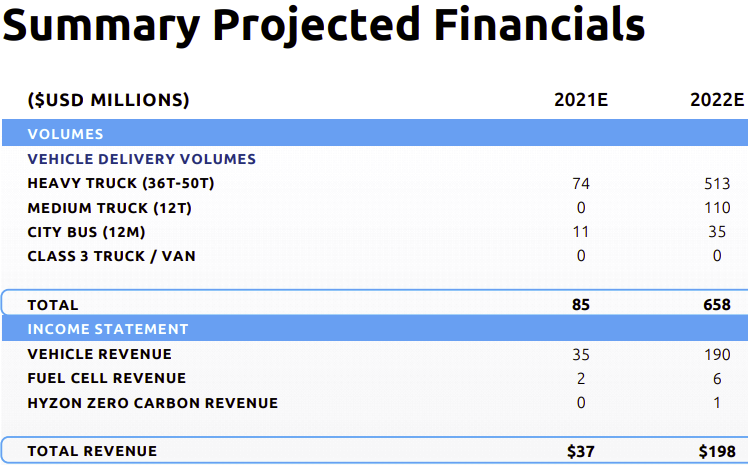

Tarkistin Heinäkuun esityksestä ja siellä oli arvioitu vuodelle 2022 658 ajoneuvoa, joten tuo nyt kerrottu 600-700 toistaa sen arvion. Tälle vuodelle oli arviotu liikevaihtoa 412k per ajoneuvo ja ensi vuodelle 289k per ajoneuvo. Tuo lasku on tietenkin luonnollista kun ensi vuonna pitäisi toimittaa myös kevyempiä ajoneuvoja. Nythän liikevaihtoa tosin tuli se 500k per ajoneuvo, mutta ehkä kahden ajoneuvon perusteella ei vielä kannatta vetää johtopäätöksiä arvioitua paremmista myyntihinnoista. Eli ei ihan niin bullish tuo 600-700 ajoneuvon arvio kuin aluksi kuulosti, mutta ainahan näin aikaisen vaiheen yrityksissä jo arvioiden toistaminen on positiivista.

26 tykkäystä

Tämä katekeskustelu meni transcriptin mukaan näin:

Craig Knight

And the second question related to the Hyzon content, if you like, so how much Hyzon content in a vehicle? So today, I think it is probably fair to say that we operate in a 35% to 40% of the kind of BOM cost of the vehicle range. It would typical, which is Hyzon content.

We are looking at getting that up towards the 70% Mark. And that essentially means that you are replacing a lot of those kind of specialized parts and components we have spoken about, and the commodity parts of the vehicle, like the chaises and doors and windows and wheels and brakes and so on. These are sourced from obviously from third parties.

It just happens to be that the commoditized parts of the vehicles are also those that usually require a lot of capital to set up manufacturing for those. So in fact, getting into the production and supply of the more specialized components within these fuel cell electric vehicles is not as burdensome on the capital front as people might think. So we believe we can get to a higher content in the vehicle with very attractive capital efficiency.

And just like we are able to build out fuel cell manufacturing, which has a very large barrier to entry, technology-wise, we are able to build that out with a modest capital commitment and that is why we don’t need billions of dollars to build this business model and this company. We are very happy with the working capital we have got on hand at the moment, and we believe that we can get up to this 70 odd percent Hyzon content over the course of the next two or three years.

And what that means for margins back to your question is that we believe that it is sustained better than average vehicle margin for a larger portion of the vehicles. So obviously anything you are doing in the vehicle, that is got a large barrier to entry are as well, differentiated is going to enjoy a better margin than the more commoditized parts of the vehicle.

So if we are doing the majority of the vehicle, when our margins are higher than average for a whole vehicle, and the margins for the commodity parts are lower than the average for the whole vehicle, I think you can see that we are planning towards enjoying sustained margin substantially better than the overall vehicle margins in a non-differentiated vehicle space.

Mark Gordon

And I want to sort of highlight something on this margin point. If you look at our long-term forecast, we have a 15.4% EBITDA margin in 2025. I mean we think that is a relatively conservative forecast. If you look at the 16 other new energy vehicles stocks that went public, we have the fourth lowest margin forecast out there. And we actually have a whole bunch of proprietary technology.

So we think that the market is not recognizing how conservative our forecast is on a relative basis. When you have proprietary technology, as Craig has pointed out, you should have a higher margin and we do, but we modeled the forecast in a way to we have upsided there.

Eli tavoite on EBITDA 15.4% ja Gross Marginin arvellaan pyörivän päälle 30%. Kuulostaa realistiselta, mutta korostavat vielä olevansa kohtuullisen konservatiivisia näiden arvioiden kanssa.

Tässä Gross Margin ennusteet Heinäkuun esityksestä vuosille 2021-2025

19 tykkäystä