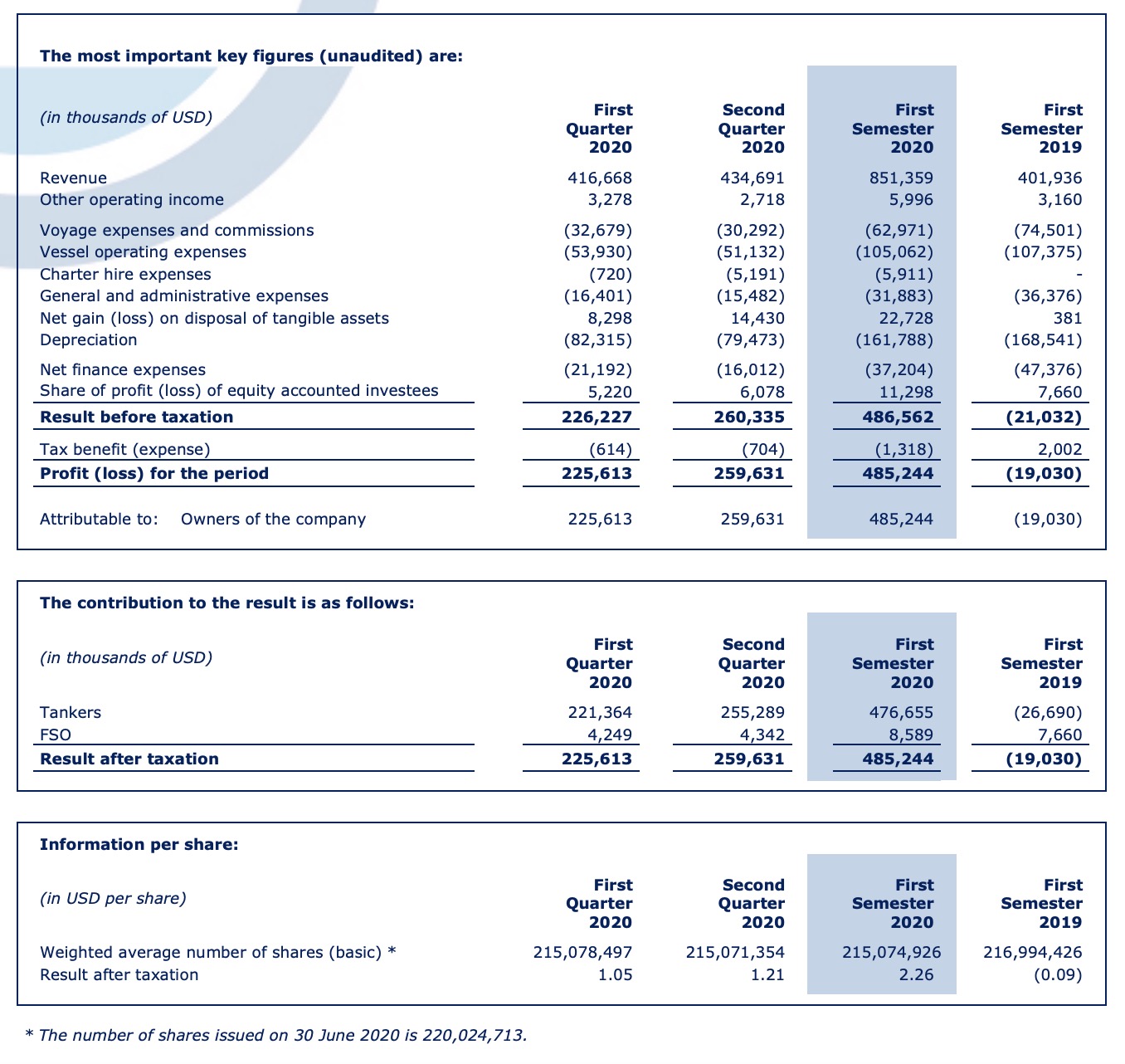

Scorpio Tankers herätti myös oman mielenkiinnon. Olen tässä lähiviikkoina ostanut muutamaan otteeseen ja pieni positio kasassa salkun pohjalla. Tässä vaan pitää yrittää päästä selvyyteen kuinka paljon sitä kannattaa nyt innostua kasvattamaan tuota positiota  .

.

Mitä ilmeisimmin näkymät taitavat olla hieman parempaan päin, ainakin alla olevan artikkelin perusteella. Onko jotain Scorpio Tankersiin liittyviä oleellisia tekijöitä mitä te yhtiön paremmin tuntevat henkilöt pidätte erityisesti silmällä tällä hetkellä?

“Tanker Operators Facing Far Better Third Quarter Than Expected (Aug 10, 2020)”

Results from several major tanker operators indicate that the third quarter will be much better than expected, projects Clarksons Platou. Earnings still benefit from the high rates seen earlier this year, while problems related to crew changes have lowered costs.

The third quarter looks set to be far better than feared for the tanker operators, even though rates have dropped from the high levels recorded earlier this year, projects broker Clarksons Platou.

The broker’s optimism comes in the wake of interim reports for the second quarter from major tanker operators Euronav and Scorpio Tankers.

Last week, the two tanker companies reported that they have already fixed contracts for half of their fleets in the third quarter. Euronav has fixed 48 percent of its VLCC vessels at rates averaging USD 60,250 per day, while Scorpio Tankers has booked 49 percent of its LR2 fleet at rates of an average of USD 22,500 per day.

“These averages are a reminder of just how strong the market was in 2Q and the opportunity presented to tanker owners to place vessels on time charter for the short- and medium-term,” writes Clarksons Platou.

“As a result, tankers are set to report much stronger 3Q results than that of 3Q19 despite the substantial decline in cargo volumes year-over-year,” adds the broker.

Clarksons Platou also says that it is “an interesting development” that several tanker operators have reported lower costs due to the limited possibilities of conducting crew changes due to the coronavirus outbreak across the globe.

The broker expects that the fourth quarter will be weaker for the tanker companies compared to the same period last year.