Tuloskausi on pyörähtänyt käyntiin ja Perionin tulosjulkaisu häämöttää jo parin viikon päässä (4. toukokuuta). Kävin tämän kunniaksi ja aikani kuluksi vähän ennusteita ja yhtiön vanhoja prujuja läpi, joista nousi esille muutamia ainakin itselleni mielenkiintoisia pointteja. Tulosennusteissa tosiaan ensimmäiselle kvartaalille povataan $86-87 milj. liikevaihtoa (+31 % YoY) ja $7,2 milj. adj. EBITDA:a (+16 % YoY). Vuoden 2020 ensimmäinen kvartaali oli yhtiölle vahva, joten ennustettu 31 %:n kasvu ei johdu heikosta vertailukaudesta. Kate-ennusteet näyttävät kuitenkin suhteellisen laihoilta.

Kuten aloituksessakin on mainittu, Perion on historiassa ollut melkoinen kassanpolttaja korkeilla kulurakenteillaan, mutta käännettä tässä on onnistuttu jo tekemään. Asiakkaiden voittaminen tuntuu kuitenkin maksavan tällä hetkellä mansikoita, ja CAC edusti vuoden 2020 viimeisellä kvartaalilla jopa 63 %:a liikevaihdosta. CAC:issa on yhtiön johdon mukaan kausittaista vaihtelua ja tämänhetkistä korkeaa lukemaa on perusteltu yritysostoilla ja product mixin laajenemisella, sekä pandemiatilanteen vaikutuksilla. Viimeisimmät yritysostot Content IQ ja Pub Ocean ovat olleet yhtiön mukaan korkeamman CAC:n yrityksiä kuin Perion orgaanisesti ja näitä uusia hankintoja on ilmeisesti alkuun pyöritelty pitkälti omina toimintoinaan. En osaa sanoa kuinka kauan integraatioiden on ajateltu ottavan aikaa siinä määrin että niillä yhä perustellaan kustannuksien nousemista. Q2 callin kysymyksessä oli ehdotettu niiden kestävän 1–2 vuotta, eikä sitä ajatusta ainakaan toimarin puolesta torpattu. Q1 callin Q&A-osiossa puhuttiin myös vuoden 2019 ”low 50’s” -CAC tasosta normaalina Perionille. Vuonna 2019 CAC edusti siis 52 %:a liikevaihdosta.

Huomionarvoisena seikkana pidän myös sitä, että yrityksen tämänhetkinen tulosennuste vuodelle 2021 ei ota matkustus/turismi -segmentin palautumista huomioon lainkaan. Kuten aloituspostauksessa on mainittu, se on kattanut aiemmin n. 15 %:a Perionin liikevaihdosta, joten odotuksien ollessa tällä hetkellä nollassa, siihen liittyvät uutiset pitäisivät tulla ainoastaan positiivisina. Tässä mielestäni korostuu taas yhtiön konservatiivinen ohjeistustyyli, josta toimari onkin useampaan otteeseen maininnut. Underpromise, overdeliver. Tuolla Q4 callissa oli ehkä vähän piikiteltävästikin kysytty, mikä saa kasvun hidastumaan tulevina vuosina 15–17 %:iin, kun yhtiö on selvästi kerännyt momentumia ja kasvanut vahvasti vuonna 2020. Vastauksesta kävi ilmi, että halutaan antaa ennemmin varovaisia pidemmän aikavälin ennusteita luoden uskoa pysyvemmästä tuloskäänteestä, siinä missä samassa avaruudessa toimivien kilpailijoiden tulosennusteet ovat kovempia mutta vain lyhyemmälle aikavälille.

Niin joo, tuohon aiempaan postaukseeni avoimista työpaikoista liittyen – Perionin kotisivulla näkyy ilmeisesti ainoastaan israelilaiset rekryilmoitukset ja muista kanavista löytyy myös liuta avoimia paikkoja jenkeistä, jonne suuri osa yrityksen toiminnoista sijoittuu.

“Amazon’s “Other” unit, which is primarily made up of advertising but also includes sales related to its other service offerings, brought in more than $6.9 billion in the first quarter, growing 77% year over year.”

Nyt on tullut kovaa kasvua kautta linjan mitä tulee ad puolelle. Eiköhän Perion suorita hyvin myös Q1, mikäli ei niin on syytä katsoa peiliin.

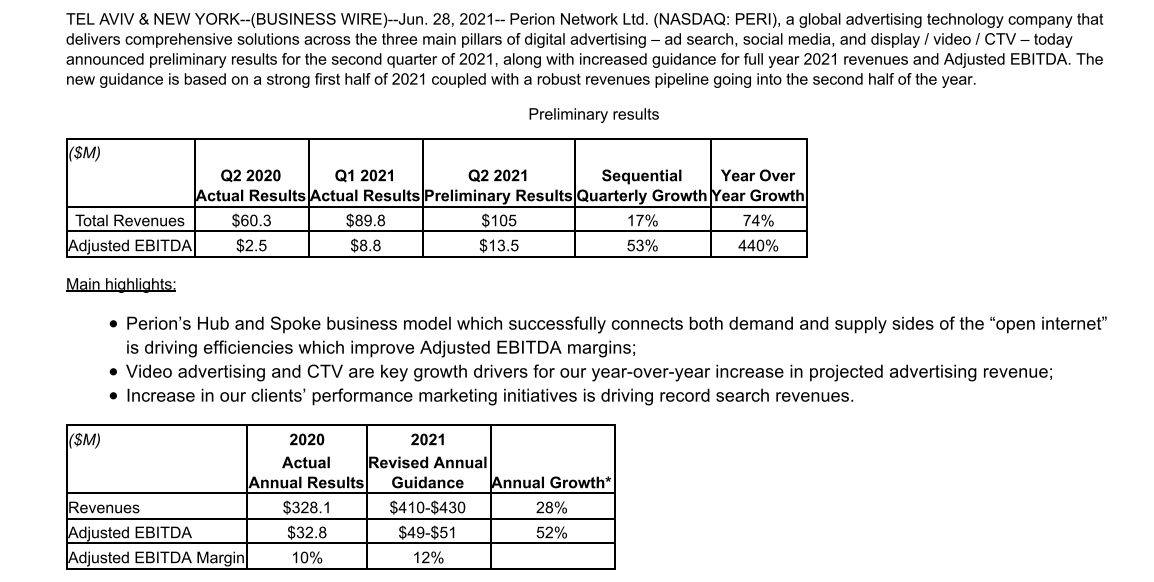

"We now expect revenue between $390 million to $410 million, and adjusted EBITDA between $39 million to $41 million.

To provide a cushion of confidence, I want to note that our 2021 guidance does not anticipate a material rebound from travel-oriented advertisers, nor does it assume any additional acquisitions. Both would represent upside to our guidance. And the fact that we are not including any projections of this incremental opportunity demonstrates the confidence we have in this expected performance."

Edit: Oppenheimer analyst Jason Helfstein maintained a Buy rating on Perion Network (PERI) today and set a price target of $30.00. The company’s shares closed last Tuesday at $16.04.

TuplaE: “Roth Capital reiterated coverage of Perion Network with a rating of Buy and set a new price target of $34.00 from $30.00 previously”

Edit: Perion Networkin markkina-arvo on eilisen päätöskurssilla 489.347MUSD, velkaa 0, kassaa 128MUSD ja kasvaa ihan kohtalaisesti.

Lisätään vielä tämä maininta callista uudestaan kun juuri inflaationumeroiden yhteydessä oli puhe matkailun elpymisestä.

“To provide a cushion of confidence, I want to note that our 2021 guidance does not anticipate a material rebound from travel-oriented advertisers, nor does it assume any additional acquisitions. Both would represent upside to our guidance. And the fact that we are not including any projections of this incremental opportunity demonstrates the confidence we have in this expected performance.”

Uutisvirta on kyllä ollut kovin myönteistä viime aikoina, mutta eihän tämäkään lappu ole sektorirotaatiolta säästynyt. Kuten ketjussakin on spekuloitu, niin eiköhän tälle ole myös jonkinlaiset Israel + matalan katteen alennukset hinnoiteltu sisään. Teknisessä mielessä kun käppyröitä tarkastelee, niin ruvetaan olemaan tuolla weekly support -alueella ja 0.618 fibon tuntumassa, joka asettuu ~13 dollariin. Uskoisin käänteen tapahtuvan viimeistään siltä tasolta.

Eiköhän tässä pitkää peliä pelaavat lopulta palkita, viimeistään jos ja kun teknojen mollivoittoinen vire joskus kääntyy.

Travel is back

" Nearly 50M U.S. airport passengers were registered in May - up 19% from April - and so far in June, the TSA has recorded nearly 35M travelers. But that’s causing some disruptions, with carriers and transportation operators struggling to keep up with the ramp up in demand, especially with the lifting of travel restrictions."

Perionin tj Q1 webcastistä:

“I want to note that our 2021 guidance does not anticipate a material rebound from travel-oriented advertisers, nor does it assume any additional acquisitions. Both would represent upside to our guidance”

Toimarin kommentit " Perion’s accelerating growth further validates our diversification strategy and the success of our holistic solutions approach,” said Doron Gerstel,

Perion’s CEO. “The key driver of our growth is the strong performance of our advertising business, which outpaced the industry’s organic growth rates,

as brands and agencies expand the adoption of our solutions. Our investments in R&D are delivering significant returns and driving Adjusted EBITDA

margin expansion. Our strong business visibility into the second half of 2021 gives us the confidence to increase our full-year outlook.”"

Ohjeistuksen nosto oli odotettavissa, hyvä että se saatiin jo ennen Q2. Odotan Q2 premeistä hieman saatetaan parantaa ja Q3 aikana saataisiin M&M toteutettua H2 aikana saadaan toinen ohjeistuksen nosto.

Salkun isoin positio edelleen ja ei tässä mikään kiire ole!

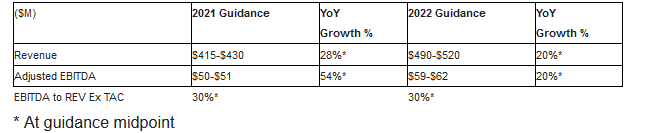

Doron Gerstel, Perion’s CEO, commented, “This quarter’s performance is another indicator that we are executing on our disciplined strategic plan and positioned to achieve our three-year targets a year earlier than expected. Based on the strength behind our growth – significantly more dollars spent per campaign and a healthy increase in new clients – we are narrowing the ranges of our 2021 guidance to revenues of $415-$430 million and EBITDA of $50-$51 million as well as introducing guidance for 2022. We expect revenue of $490-$520 million and Adjusted EBITDA of $59-$62 million in 2022.”

Second Quarter 2021 Highlights

Advertising revenue growth of 211% (or 134% on pro forma basis) fueled by broad-based adoption of our video and CTV offerings, leading to an increase of average campaign spend by 58% and a 67% increase in number of clients;

Search advertising revenue growth of 24%, primarily driven by increased performance advertising spend by brands;

The inherent and strategically constructed operating leverage in our business model increased adjusted EBITDA margin to 33% of revenue excluding traffic acquisitions costs compared to 10% in the second quarter of 2020; and

Net cash provided by operating activities was $14.6 million; Perion has $141 million in cash and zero debt as of June 30, 2021.

Outlook

Perion is narrowing it’s 2021 guidance and expects revenues to be between $415-$430 million (previously $410-$430 million) and EBITDA of $50-$51 million (previously $49-$51 million). Based on the strong business momentum and improved visibility, Perion is introducing guidance for 2022.

Oli kova Q2 tulos, meni vielä yli kesäkuun nostetuista näkymistä.

Oli kyllä erikoinen reaktio, kun kurssissakaan ei varsinaista fronttausta ollut nähtävillä. Puolittaisella osarilotto -ajatuksella lähtenyt position avaus jää kuitenkin olemaan pitempään holdiin - huolimatta kurssista tai ehkä jopa sen takia. Vielä kun NON laittaisi lainoitusarvon, niin olisi helpompi holdailla Pyyntö laitettu vetämään…

Muutama poiminta skriptistä

Kassaa on kertynyt hyvin. Ja tekeillä on ilmeisesti yritysostoa, kunhan vaan hinta ja kohde on sopiva.

From a capital position, we have $141 million in cash with zero debt. We generated $14.6 million in cash in the second quarter further boosting our balance sheet.

Those of you who have been following Perion know that we are an active strategic acquirer with the two accretive acquisitions we did in 2020. We’ve demonstrated that our deal structure with significant earn-out component, minimize the natural risk of any acquisition, and most importantly, keep the acquire team active and incentivized for the long run. We have the capital, the ability to identify the right targets and the financial model to pursue the right opportunity.

2021 näkymät ja ennusteet koservatiivisia, kuten ilmeisesti ollut aiemminkin. Oma historia tämän parista tässä vaiheessa alle viikon verran

we are quite conservative in our projection. And as we did in the last three years, we definitely would like to follow the under promise and overachieved narrative, which we’re having in the last few years.

2022 Q1 tulossa 30M$ earn out maksuja yritysostoista

We actually are not expecting to have much more payment this year with a small amount in July around $1 million. But this is it. All the other payments that we have on the balance sheet, if everything real going according to plan will pay around Q1,2022. … About $30 million.

Mielenkiintoinen veto analyytikolta ottaa myös Outbrain ja Taboola mukaan verrokkeina. Näistä kolmesta yhdessä tai kahdesta keskenään voisi saada jonkinlaisen fuusion aikaan. Synergiaa varmasti olisi OB ja TBLA tätä jo aiemmin yritti tehdäkin, mutta prosessi vedettiin jäihin.

Laura Martin

Super helpful. And then our content monetization, that was a really interesting answer you gave. I’m curious as to how you would compare that business to Outbrain and Taboola. Is that a direct competitor to those two recommendation engine businesses?

Maoz Sigron

Right. No, it’s not we’re using Outbrain and Taboola. Basically, our content recommendation. So the fact that we are helping publisher in this case is Newsweek to get new audience into the assets, into their assets, which working on our content management system, because their whole engine of optimizing or increase the revenue per session is our own engine, which is based on our own proprietary content management system. This is our core technology. One of the way here to increase it because at the end of the day, it’s a Rev share base and the idea is how are we able to get the most of this technology is by driving new audience, part of the audiences. The majority is coming from social media and the other which is like 25% is coming from content recommendation in this regard. Taboola and Outbrain are great partners and definitely drive audience into this publisher and Newsweekis one of them.