Joitakin podeja, näitä on muuten Affectivalla paljon.

Todella mukavaa näin omistajankin kannalta kun tulee paljon enemmän seurattavaa ja kuunneltavaa Affectivan erittäin aktiivisen PR:n myötä. Tuossa vain muutamia silmään osuneita podeja koko listasta poimittuna.

2019 vuodelta löytyy myös mm. Veoneer ja Nuance podit

Muutaman päivän pureskelulla tosi hieno juttu tämä yrityskauppa. Sijoituscase ainakin omasta näkökulmasta muuttui kertaheitolla. Long positiosta tuli extra long, eli liiketoiminnan jatkuvuus ei ole enää kysymysmerkki ja mahdollisuudet muuallekin kuin automotiveen ovat nyt oikeasti realistisia. Lyhyen ajan tuottomahdollisuudet muuttuivat sikäli, että nyt otettiin paljon lisää työntekijöitä helman alle ja profit pylväät siirtyivät uusien työntekijöiden ja yhdistymisen aiheuttamien kulujen verran eteenpäin, vailla tietoa uuden ostetun liiketoiminnan vaikutuksesta lukuihin. Kuluja tulee siis varmasti, tuotot jäävät nähtäväksi (luottavainen olen silti) Nythän tässä on ollut paljon selkänojaa tuleviin arvostustasoihin sen vuoksi, että kulut eivät juuri edellisellä setupilla olisi kasvaneet, mutta korkean katteen lisenssimaksuja yms. olis alkanut rullailemaan. Hienoa nähdä, että smartilla on uskallusta ottaa tällainen askel, pienempiä ja potentiaalisia firmoja tulee napsia varmasti tulevaisuudessakin, ennen kuin tulevat liian koviksi kilpailijoiksi.

Mielenkiintoista on se, että affectivan arvoksi osana smarttia määriteltiin 75M. Smartin markkina-arvo taisi olla ennen yhdistymistä 450M. Molemmat firmat taitavat tehdä melkein saman verran liikevaihtoa. Smartin strong pipeline taitaa näytellä tuossa MA erossa isoa roolia ja Affectivan porukalla on varmaan aika hyvä näkyvyys Smartin asemasta markkinoilla. Smartin korkeasta markkina-arvosta huolimatta Affectiva ottaa maksun Smartin osakkeina, aika vahvaa luottoa positiiviseen tulevaisuuteen (?). Mikä muuten mahtoi olla affectivan omistuspohja, onko jolllain tietoa suoralta kädeltä?

”This is a transformation that is going to happen over 30 years and possibly longer,” said Chris Urmson, an early engineer on the Google self-driving car project before it became the Alphabet business unit called Waymo. He is now chief executive of Aurora, the company that acquired Uber’s autonomous vehicle unit.”

Ihan samat pohdinnat itsellä. Etenkin kun kurssi on noussut ilman suuria uutisia 2x viime syksystä. Tämä kauppa antaa tukea kurssille uudella tavalla ja markkinan koko kasvoi martinin mukaan 2-3x.

We have previously mentioned that Seeing Machines often highlights its large data sets to be

key for being able to develop great AI. We believe Smart Eye’s acquisition of Affectiva puts

the company in an even better position in regard to this competitive edge.

Hyvä setti RedEyen uudelta analyytikolta. Pitkälti samoilla linjoilla olen.

Liikevaihdon kasvun aikahorisontti on nyt venynyt suotuisan regulaatio & markkinakehityksen takia Interior Sensingin osalta. Hinnoitteleeko markkinat tätä vielä tehokkaasti? Näyttäisi siltä, että mahdollisuuksia liikevaihdon kasvuun riittäisi ainakin 2020-luvun loppuun asti. Toki paljon nyt luotetaan Martin Krantzin viimeaikaisiin puheisiin Interior Sensing markkinan tulevaisuudennäkymistä.

Loppujen lopuksi kaikki on kuitenkin kiinni executionista eli kuinka suuren markkinaosuuden SEYE saa tulevissa DMS & Interior Sensing design winneissä, pärjätäänkö R&D kilpajuoksussa, kuinka hyvin saadaan integroitua Affectivan ja SEYE:n tiimit & kulttuurit, kuinka hyvin johto saa motivoitua henkilöstä painamaan pitkää päivää kilpailutuksissa jne… Eli toisin sanoen tällä hetkellä on todella hyvä meininki & potentiaali kasvuun, mutta riskejä on olemassa ja nämä on hyvä tiedostaa kun tekee portfolion allokaatiopäätöksiä.

Toinen merkittävä tekijä tuottopotentiaalissa, joka tällä hetkellä toimii kurssiajurina, on regulaatiokehitys avainmarkkinnoilla (USA, EU, Kiina). EU näyttää todella hyvältä, Yhdysvalloissa DMS & Interior Sensing regulaatio taitaa vielä olla vähän auki? Positiivisia merkkejä sielläkin on hiljattain ollut näkyvissä: Call for Driver Monitoring Systems to Improve Safety - Consumer Reports. Regulaation myöhästyminen tai vaatimusten löystyminen avainmarkkinnoilla toisaalta vaikuttaisi negatiivisesti sijoituskeissiin.

Niinpä. Oleellista on, että ennusteissa käytettäisiin kunnollisia turvamarginaaleja. Markkinaosuudet mielellään tyydyttävän onnistumisen mukaan laskettuna, niin riski pettymyksille pienenee ja jää optio ennusteylityksille.

Pitäisikin tsekata viimeisin Redeyen analyysi, oliko turvamarginaaleja nipistetty entisestä.

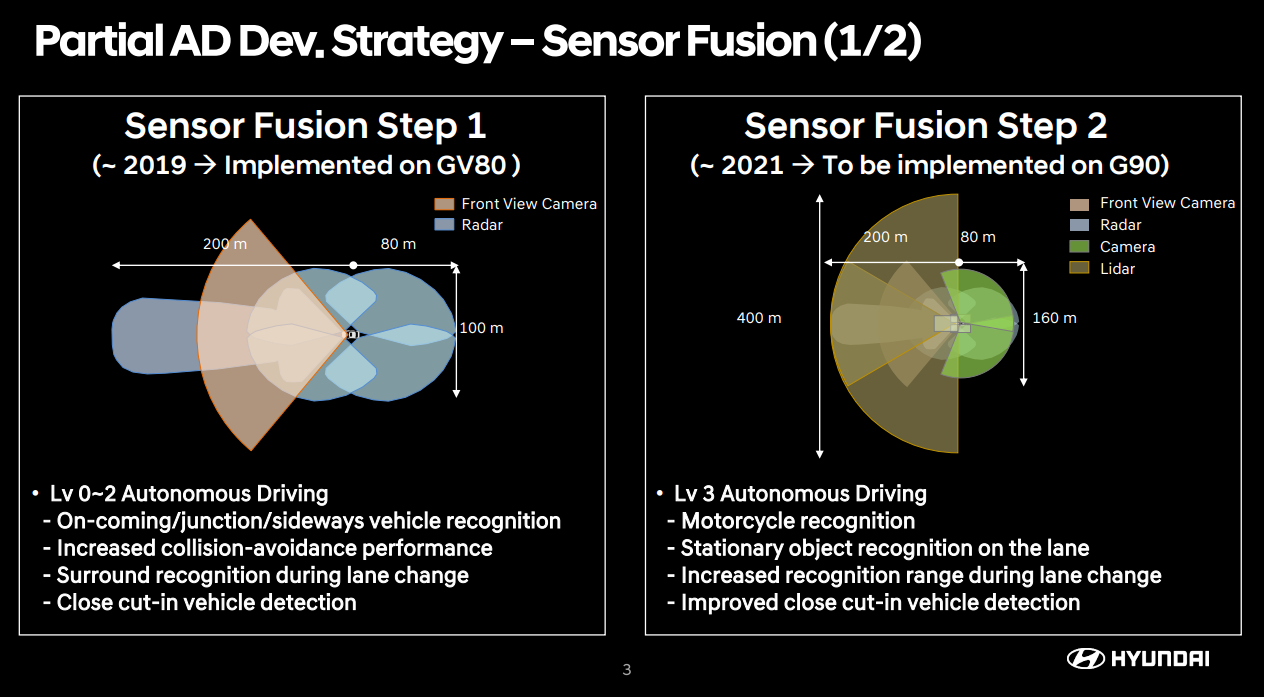

G90 ja Ioniq6 ovat mahdollisesti ensimmäisiä L3-malleja. (” The Hyundai Ioniq 6 and Hyundai Ioniq 7 may come with Highway Driving Pilot for Level 3 autonomous driving. ”).

A complete guide when choosing an eye tracking solution

Join us (Rob Wesley, Brant Hayes and Aaron Galbraith) live on June 10th at 6PM CET for this webinar where we will go through the background of understanding eye tracking followed with a guide when choosing the right eye tracking solution for your purpose.

Huhujen mukaan joitakin jenkkisijoittajia alkanut kiinnostua firmasta

Ajankohtakin viittaisi vähän siihen, että halutaan joillekin “uusille omistajille” kertoa mikä SmartEye oikein on…?

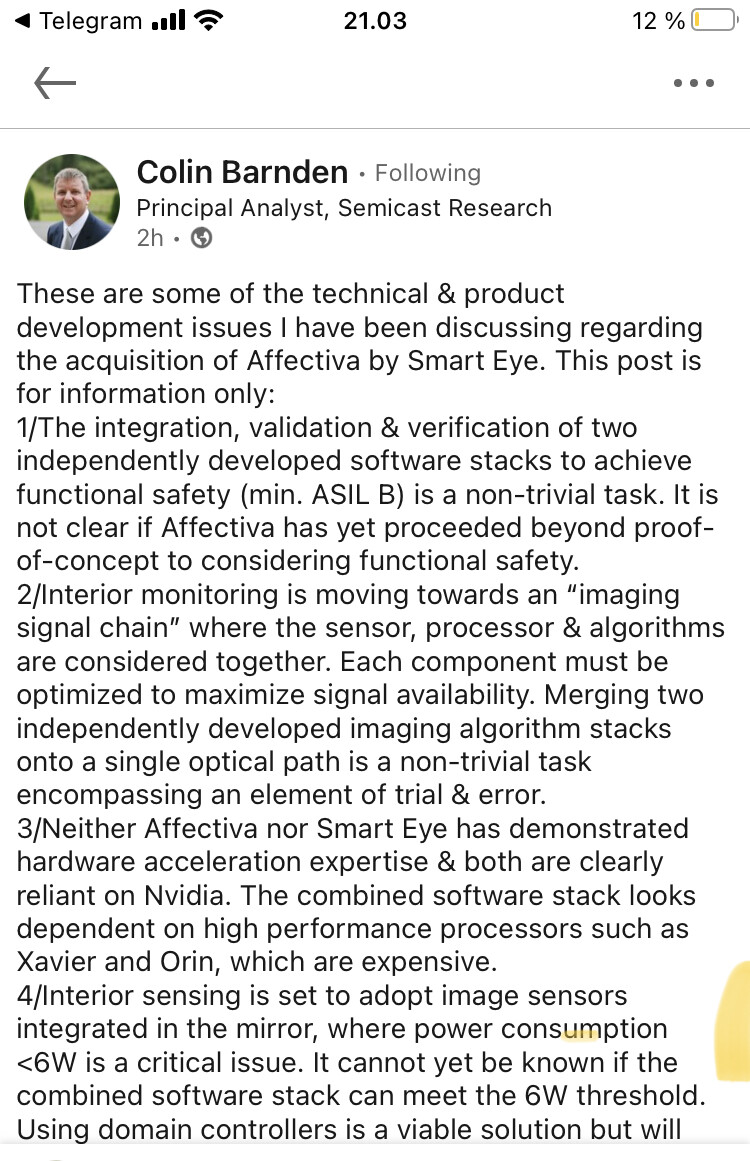

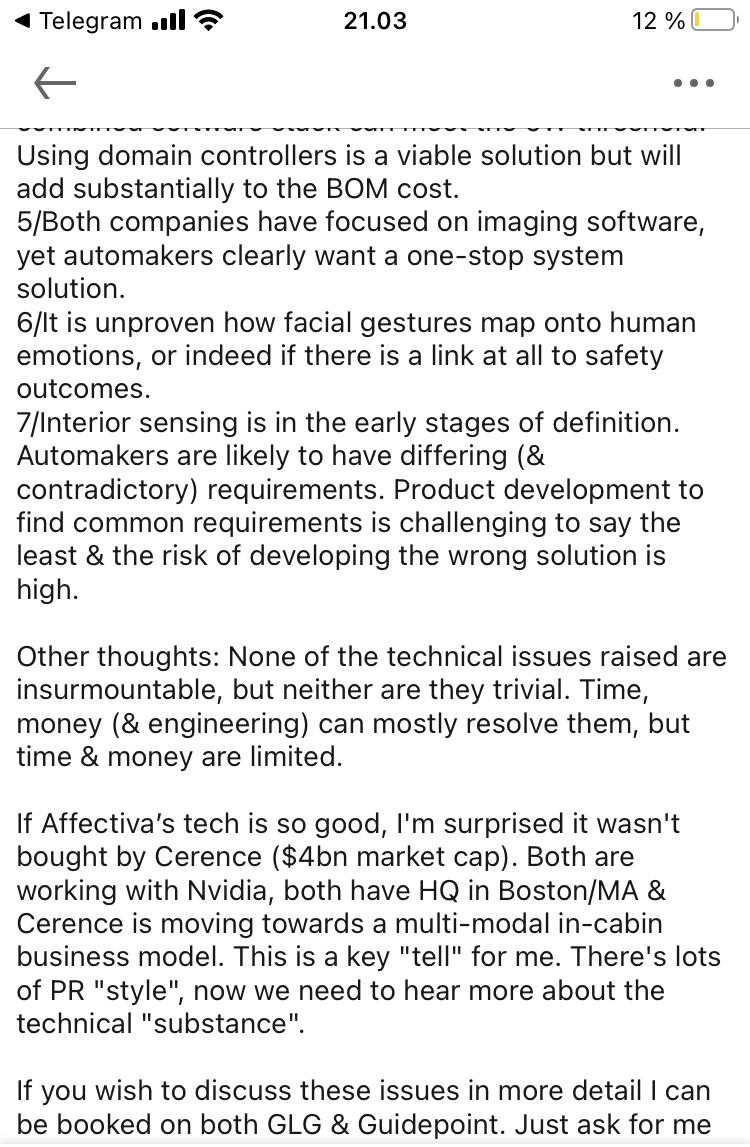

Osa ihan valideja pointteja Colinilta (mm. softastackien integrointi ei ole helppoa), mutta normaalit analyytikot analysoivat yhdistymistä esim pros&cons tyylisesti.

Colin taas ei löydä normaalin tapaansa Smartista tai sen ekosysteemistä mitään hyvää ja hakemalla hakee kaikkea negaa.

Kysymykseen, miksi Cerence ei ostanut Affectivaa, jos Affectivan teknologia kerta niin hyvä ja Cerencen arvo moninkertainen, voisi vastata vastaavasti, että miksi joku BMW, Ford, GM tai Qualcomm ei osta Seeing Machinesin nakkikiskaa, jos heidän teknologia niin ylivoimainen.

Kesa, let me provide some pro points for the deal:

The two companies are complimentary with little overlap. Good, you won’t need to spend 3-6 months deciding which developments to stop (but you won’t be able to reduce development costs much)

The media part of Affectiva is profitable - good, it should be able to fund the cost of 1or 2 good engineers in Boston or Sweden

Staff in Egypt (plus contractors?) provide cheap labelling for test data. Useful for emotion, and verification of possible state in video - have some video, possibly mostly for emotion and linked to media consumption rather than automotive. But they do have some automotive video but don’t have the experience of optical path, so will not be representative of real life embedded camera and lighting.

Complimentary in locations, but this also gives little fat to cut as will still need HR, finance, management etc for each country but will enable extra office location for merged sales staff.

Extra PR Affectiva are excellent at PR. I have been listening to the podcasts for over a year. They follow a wide range of subjects to get their name out there, especially the good Dr with her book. They are good at getting attention which was essential when funding thru VC

Colin is right, merging two ISO 26262 stacks will be hard. But it will be easier if you assume that Affectiva aren’t auto qualified and you only try to add the bare minimum of Affectiva into the SEYE stack and bring that part up to SEYE standard. (ASIL?)

You probably don’t need to write off the $10m or so that it takes to optimise Affectiva for HW acceleration. So now you will only need to do it once, when you have merged stacks

The best part of the merger/acquisition (other than the extra staff (cash burn) is that it provides a new narrative. SEYE concentrate their PR on Nordic investors (private and institutional) to keep the share price growing. They have 80+ DW, but that growth may stall due to Qualcomm. So Martin needs a new dream to sell (and cash to fund it) until he reaches his goal of the big sell. That is not VAG or Toyota, it is when he sells SEYE. He needs to be a bigger fish and the extra confusion of Affectiva will provide extra DW without needing to clarify who won what.

Now you may say correctly that SEE is about the big sell too. But our PR is tiny and aimed not at us grumpy shareholders, they are trying to make sure that auto Execs don’t know much about us until they sign the contracts. We don’t want them to realise that we are aiming for more than 30% of the HW market (we will share the software market with you, Cipia etc)

I don’t really fancy the idea of dealing the DMS/OMS/… market completely on one player entirely (due to dual sourcing preference and market dynamics in common), so this argument may be invalid in the first place.

Anyway, I find it unsettling to read comments on a company (whether it is SEE or SEYE) argued from a point of view of “us” and “them”. Those pronouns make the conversation feel like it is spoken by private investors against the (aggressive) IR of the “opposing” company. After all, every private investors is looking for best risk/reward ratio, and these conversations are not sounding like that. The point of many posts seem to be about trashing the opposite player, instead of validating the investment case of either of argued company. There may be (and there are) valid points in both of the “camps” of SEE and SEYE, but the idea of providing the best information on the best investment case seems to be lost in the struggle of which company is better as such at times. Not about which company is better investment case.

Of course the rivalry and division of the market is a significant factor in the investment case, but simply pointing out the problems of a deal or challenges of a company is not fertile discussion at all. The conversation on pros and cons might be the first step on creating value on the discussion on business case, and it concretely gives something to the discussion on the investment case itself.

To be not trashing myself, I do appreciate the effort @TheLongestShot is giving here! You are pointing out valid points against SEYE, which are of great value on calculating the business case. Also, my comment is not against the SEE “camp” alone, I find a lot of pro-SEYE comments, which are argued simply by negative view on SEE, which is not providing any more fertile discussion on the investment case of SEYE. After all there are loads of other tier 2 (and tier 1 I guess) players interested to win the market share, besides the OEMs who are not interested to give the DMS/OMS/… market solely to one DMS supplier. And behind them, are the interests of us tier 2 private investors, trying to find the best investment case, which may be different to anything the OEMs, or tier 1s, or other tier 2s are interested in. So driving the discussion to the points of view of “us” or “you” really do not serve the purpose.

Guess this is my zero cents on the discussion on the investment case. On the topic instead, I don’t really take the cons mentioned above too meaningfully. The investment case of SEYE is now mostly about DMS/OMS/… market share of 30-40%, which would generate such amounts of revenue the tiny monetary cons of Affectiva are just tidbits. Instead, the acquisition provides more opportunities to create value for shareholders even after the big first DMS/OMS/… wave, which provides the investors better outlook and therefore increases the value of investment case. And that should be about the only thing a private investor cares about!