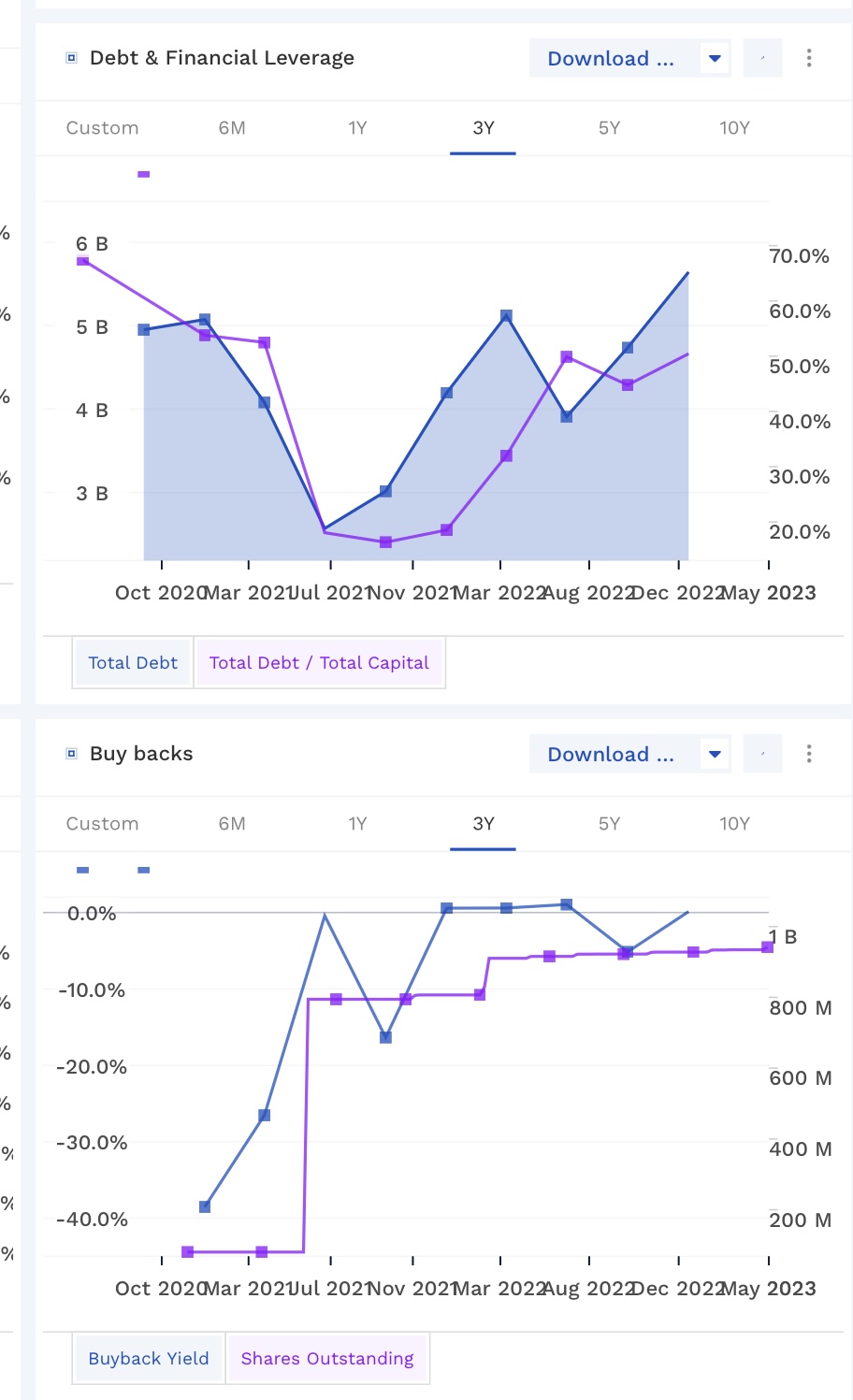

Karhuteesiä tukee ainakin kasvava velan määrä ja huomattava stock based compensation. Jälkimmäinen dilutoi osakkeenomistajia kovaa tahtia edelleen. Näistä puuttuu 1Q luvut mutta sama trendi jatkui.

5 tykkäystä

Tämä on yksi itseä jonkin verran häiritsevä tekijä. Sofi ei ole ainoa, jossa tämä ilmenee, mutta kompensaatiot ovat kyllä merkittävät. Ansiosta toki kokonaisuuden rakentamisessa, mutta voisiko olla jokin rajoitin vastassa?

Siitä huolimatta tässä ympäristössä kova suoritus, näkymien nostot ja siitä huolimatta -12% taisi olla lopputulos julkkaripäivään ![]() Olisiko näillä luvuilla pitänyt nostaa näkymiä enemmän loppuvuodelle, jotta olisi kelvannut? Sofi on kuitenkin ennustanut tyypillisesti alle toteutuneen, eli alkaa olla selkeän konservatiivinen näiden suhteen.

Olisiko näillä luvuilla pitänyt nostaa näkymiä enemmän loppuvuodelle, jotta olisi kelvannut? Sofi on kuitenkin ennustanut tyypillisesti alle toteutuneen, eli alkaa olla selkeän konservatiivinen näiden suhteen.

Myös koko pankkisektori on toki paineessa, eli sieltä puolelta toki myös vastatuulta.

Kommentteja maailmalta:

Alustapuolella hidastumista? ![]()

SoFi’s tech platform showing signs of slowing?

We want to remind you that one of the characteristics that we like about SoFi Technologies, Inc. is that it has advanced technological capabilities that it employs to attract customers. They are among the best in the business, and really across other businesses, at cross-selling products. The synergy of Technisys and Galileo has led to tremendous growth, but that growth is now slowing. The technology platform-enabled accounts were up by 15% year-over-year to 126.3 million, though that appears to have declined from 130.7 million last quarter. This could be part of the selling today. In this segment, Q1 revenue was $77.9 million in the quarter, which was up 28% from last year, but down from Q4.

Ja karhuilut poimittu tuolta, velan määrä ja osakepalkkiot toki mainittu mukana:

Bad and Ugly:

Since the report was very impressive, I am combining the Bad and Ugly sections into one, with most of these points focusing beyond this single quarter.

- SoFi’s operating margin continues to be under pressure but this is not surprising given the age of the company. Keep an eye on the company’s debt level (covered below) as it progresses through the next few quarters and years.

- As strong as the personal lending numbers were, this may not be sustainable long-term, especially if the economy tanks. I don’t need to reiterate the credit risks in such a scenario. A 749 FICO score may not mean much if the monthly paychecks stop coming in and the typical high-tech household will suddenly be under pressure to make their mortgage payments on time.

- This is not directly related to this Quarter, but something of note in general. While the company’s cash level went up significantly this quarter, SoFi has so far reported just one quarter with positive Free Cash Flow since going public (the very first quarter). The company’s debt and shares outstanding have both been on an upward trajectory.

1 tykkäys

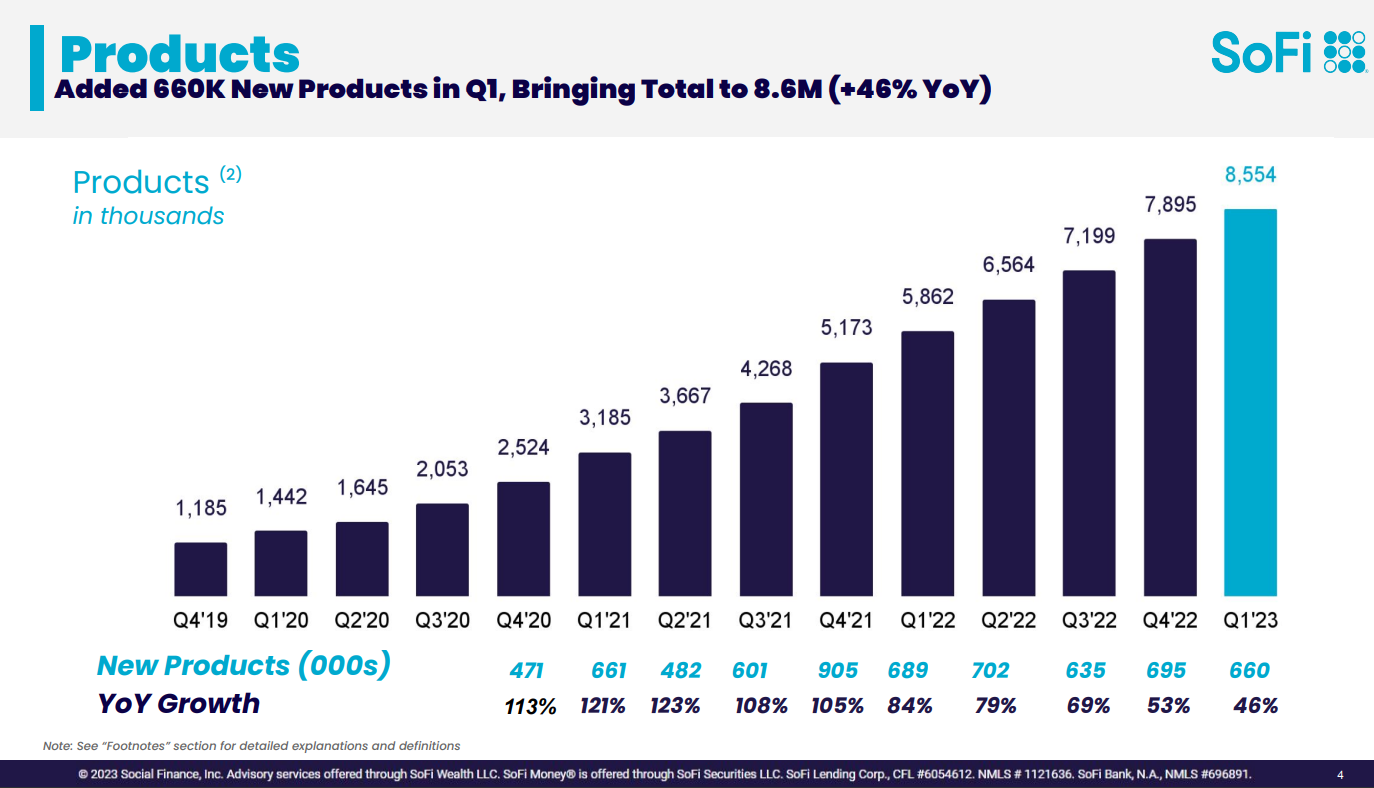

Mitä products on alla olevassa kuvassa? Onko esim yhden ihmisen yksi tili tai luotokortti tai laina aina yksi tuote? Jos näin niin keskimäärin asiakkaalla vain 1,7 tuotetta käytössä. Kuulostaa vähäiseltä, mutta toisaalta mahdollistaa kasvua.

1 tykkäys

Earnings call Presentation

Presiksen Footnote (2) löytyy selitystä enemmänkin:

(2) Total products refers to the aggregate number of lending and financial services products that our members have selected on our platform since our inception through the reporting date, whether or not the members are still

registered for such products. In our Lending segment, total products refers to the number of personal loans, student loans and home loans that have been originated through our platform through the reporting date, whether or

not such loans have been paid off. If a member has multiple loan products of the same loan product type, such as two personal loans, that is counted as a single product. However, if a member has multiple loan products

across loan product types, such as one personal loan and one home loan, that is counted as two products. In our Financial Services segment, total products refers to the number of SoFi Money accounts (presented inclusive of

SoFi Checking and Savings accounts held at SoFi Bank and cash management accounts), SoFi Invest accounts, SoFi Credit Card accounts (including accounts with a zero dollar balance at the reporting date), referred loans

(which are originated by a third-party partner to which we provide pre-qualified borrower referrals), SoFi At Work accounts and SoFi Relay accounts (with either credit score monitoring enabled or external linked accounts) that

have been opened through our platform through the reporting date. SoFi Checking and Savings accounts are considered one account within our total products metric. Our SoFi Invest service is comprised of three products:

active investing accounts, robo-advisory accounts and digital assets accounts. If a member has multiple SoFi Invest products of the same account type, such as two active investing accounts, that is counted as a single

product. However, if a member has multiple SoFi Invest products across account types, such as one active investing account and one robo-advisory account, those separate account types are considered separate products. In

the event a member is removed in accordance with our terms of service, as discussed in footnote (1) above, the member’s associated products are also removed.

1 tykkäys

Itse omistin Sofi hieman yli vuosi sitten ja myin tappiolla 2022 keväällä. Ostin osaketta aluksi, kun kiinnosti brändäys finanssialan Amazonista sekä myös spac esitteen tulevaisuuden ennusteet ja toimitusjohtaja olivat osasyitä.

2022 keväällä myin osakkeen, kun kaikki alkuperäiset asiat olivat kääntyneet. Bisnes oli muuttunut kuluttaja lainoitukseen pääosin, tulosennusteet ebitdan osalta olivat pettäneet ja toimitusjohtajan hypetys kommentit syövät itsellä hänen arvostusta.

Osake omasta mielestä tippuu nyt ihan syystäkin, kun kasvu ja voitot tulevat heikoiten arvostetusta bisneksestä eli kuluttajalainoituksesta = pikavipeistä. Siinä myös enemmän riskejä kuin asunto- ja opiskelijalaina bisneksissä missä vakuudet pääosin. Ylivoimaisesti arvokkain yksikkö eli teknologia puoli kasvaa merkittävästi hitaammin, vaikka yritysostoja tehty tiheään. Noto vielä jauhanut kuinka Sofin bisnes jakaantunut niin laajasti, mutta pikavipit ovat pääosa bisneksestä. Spac esitteessä Noto lupasi tälle vuodelle 2miljardin liikevaihdolla 716 miljoonan ebitdan, liikevaihto toteutuu mutta ebitda jää ennusteista valtavasti. Kuinka todellinen on arvio aikanaan ollut, olisiko kukaan voinut spac listautumisen ulkopuolella normaalissa listautumisessa valehdella noin paljon ?. Jos Sofin tulevaisuus on, että kasvu tulee pikavipeistä on arvostuksessa vieläkin paljon laskuvaraa jos vertaa esim lendingclubiin tai jos Sofi on pelkkä nettipankki niin Buffetin omistaman Ally Financen arvostus ei päätä huimaa. Arvo on vahvasti kiinni teknologia yksikön menestymisessä, se varmasti omaa isomman arvostuksen jos kasvua pystytään saamaan. Sofissa nyt myös riskejä kuluttajalainoituksen luottotappioissa lamassa sekä yritys poliitisesti maalitaulu kun haastoi valtion oikeuteen opiskelijalainoista. Itse olen kyllä avoin ostamaan osakkeen takaisin salkkuun jos teknologia yksikkö kasvaa ennakoitua nopeammin tai asunto/opiskelijalainoitus ottaa isomman osuuden kuluttajalainoituksesta.

7 tykkäystä

En ollut aikaisemmin kiinnittänyt huomiota mutta jenkkien viimeisimmän lainakatto ehdotuksen mukaan opintolainoja pitäisi viimein alkaa maksaa takaisin.

1 tykkäys

Tuolta lisää päätöksen seurauksista Sofille ja paljon muutakin konferenssin haastattelusta

So, go back to that same exact example I gave where someone was paying 6% over 10 years, assume for a second they’re paying 7% and extend out to 20 years. Their monthly payment will go to $540. So, it’s still a meaningful savings relative to the $775 that they were paying prior to that. So, really big opportunity. We think that there’s going to be excess demand in Q4 for us this year. This was all contemplated in the guide that we gave during our Q1 earnings call.

We expect interest to start accruing on August 30 of this year, servicers to start sending out bills in September and people to actually go back into repayment in October. So, we do expect an uplift in demand. As a reminder for folks back in 2018, prior to Cares Act, we originated on average about $1.7 billion per quarter.

So, overall quarter is going extremely well. We remain comfortable with the guidance that I provided during our Q1 earnings call. We continue to see really strong growth from a member and product perspective in-line with what we’ve seen over the course of the last several quarters. From an originations perspective, we continue to expect to see modest growth in our personal loans business.

On the student loan refinancing front, we do expect an uptick in demand in Q4. And then on the home loans front, we just acquired Wyndham Capital and the integration there is going extremely well, and we expect to see an uplift as a result of that acquisition in the back part of this year as well. So, from a member product growth perspective and originations perspective, all is going extremely well and in-line with expectations.

So, I think we’re in a really unique position where repricing our back book doesn’t have the same impact as it does for larger legacy institutions where a 10, 15, 20 basis point move in APY has a meaningful impact on the P&L.

So, we’re going to have all three segments delivering positive contribution profits. Below the consolidated contribution profit, you have depreciation and amortization, which is a large expense item and is primarily associated with amortization of intangibles of the Galileo and the Technisys acquisitions. We expect as revenue continues to grow, that we’re going to see meaningful leverage in that line item. That line item is not going to grow meaningfully for the foreseeable future. And then on the stock-based compensation side, it was 14% of revenue this past quarter.

…

EBITDA was larger than stock-based comp for the first time, and we expect to continue to get meaningful leverage in that line item as well. What we’ve said publicly is that we expect it to be single digits in the medium-term. It’s at 14% today, down from about 26.5% a year ago

SBC osalta dilutointi luonnollisesti vähenee, kun osakemäärä kasvaa ![]()

![]()

GAAP profitability by the end of this year in Q4, and we expect it to continue delivering 30% incremental EBITDA margins for the foreseeable future and 20% GAAP net income margins

6 tykkäystä

Ennakkoja Q2/H1 tulokseen ![]()

- SoFi Technologies (NASDAQ:SOFI) is scheduled to announce Q2 earnings results on Monday, July 31st, before market open.

- The consensus EPS Estimate is -$0.07 (+41.7% Y/Y) and the consensus Revenue Estimate is $475.78M (+33.6% Y/Y).

- Over the last 1 year, SOFI has beaten EPS estimates 50% of the time and has beaten revenue estimates 100% of the time.

6 tykkäystä

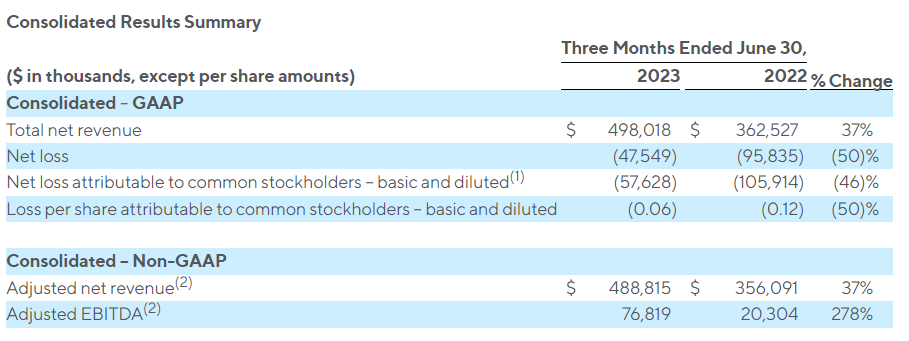

Sekä EPS että liikevaihto yli ennusteiden, näkymiä nostettu. Tiedä sitten, miten riittää markkinalle, kun kurssi vetänyt ylämäkeen koko kesän. Liikettä kuitenkin odotettavissa ![]()

- Record GAAP and Adjusted Net Revenue for Second Quarter 2023

- GAAP Net Revenue of $498 Million Up 37%; $489 Million Adjusted Net Revenue Up 37% Year-over-Year

- Record Adjusted EBITDA of $77 Million Up 278% Year-over-Year

- New Member Adds of Over 584,000; Quarter-End Total Members Up 44% Year-over-Year to Over 6.2 Million

- New Product Adds of Nearly 847,000; Quarter-End Total Products Up 43% Year-over-Year to Over 9.4 Million Total Deposit Growth of $2.7 Billion, Up 26% During the Second Quarter to $12.7 Billion

- Management Raises Full-Year 2023 Guidance

Guidance and Outlook

Management expects to generate $1.025 to $1.085 billion of adjusted net revenue in the second half of 2023, up 19% to 26% year-over-year, and $180 to $190 million of adjusted EBITDA.

For the full year 2023, management expects adjusted net revenue of $1.974 to $2.034 billion, up from its prior guidance of $1.955 to $2.02 billion, and full-year adjusted EBITDA of $333 to $343 million, up from its prior guidance of $268 to $288 million, representing a 40-44% incremental adjusted EBITDA margin. Management projects that a more significant portion of the second half adjusted net revenue and adjusted EBITDA results will be generated during the fourth quarter. As the company moves toward expected GAAP net income profitability in the fourth quarter, management expects share-based compensation and depreciation and amortization expenses to be slightly higher than reported second quarter 2023 levels in both the third and fourth quarters of the year.

Edit, vielä sijoittajapresis mukaan

16 tykkäystä

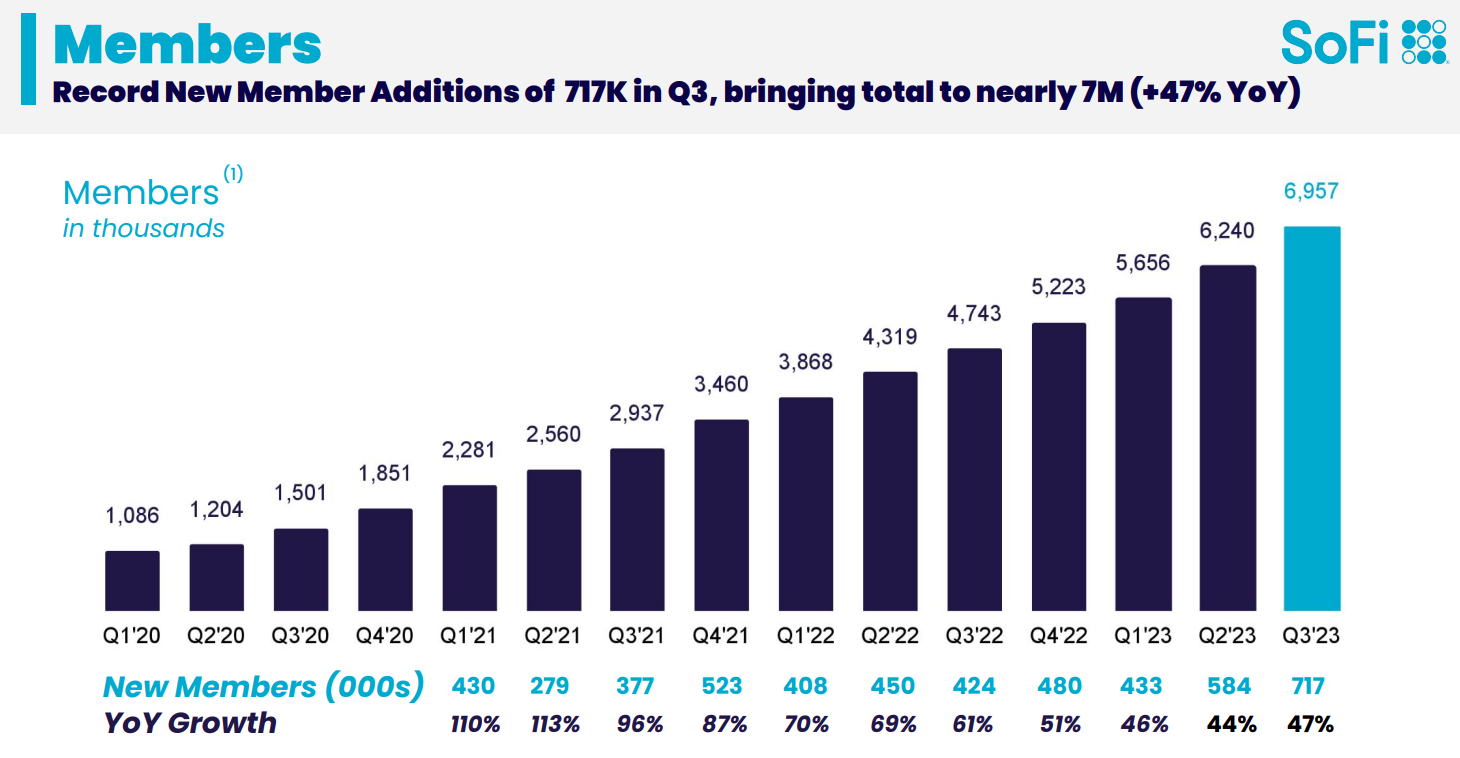

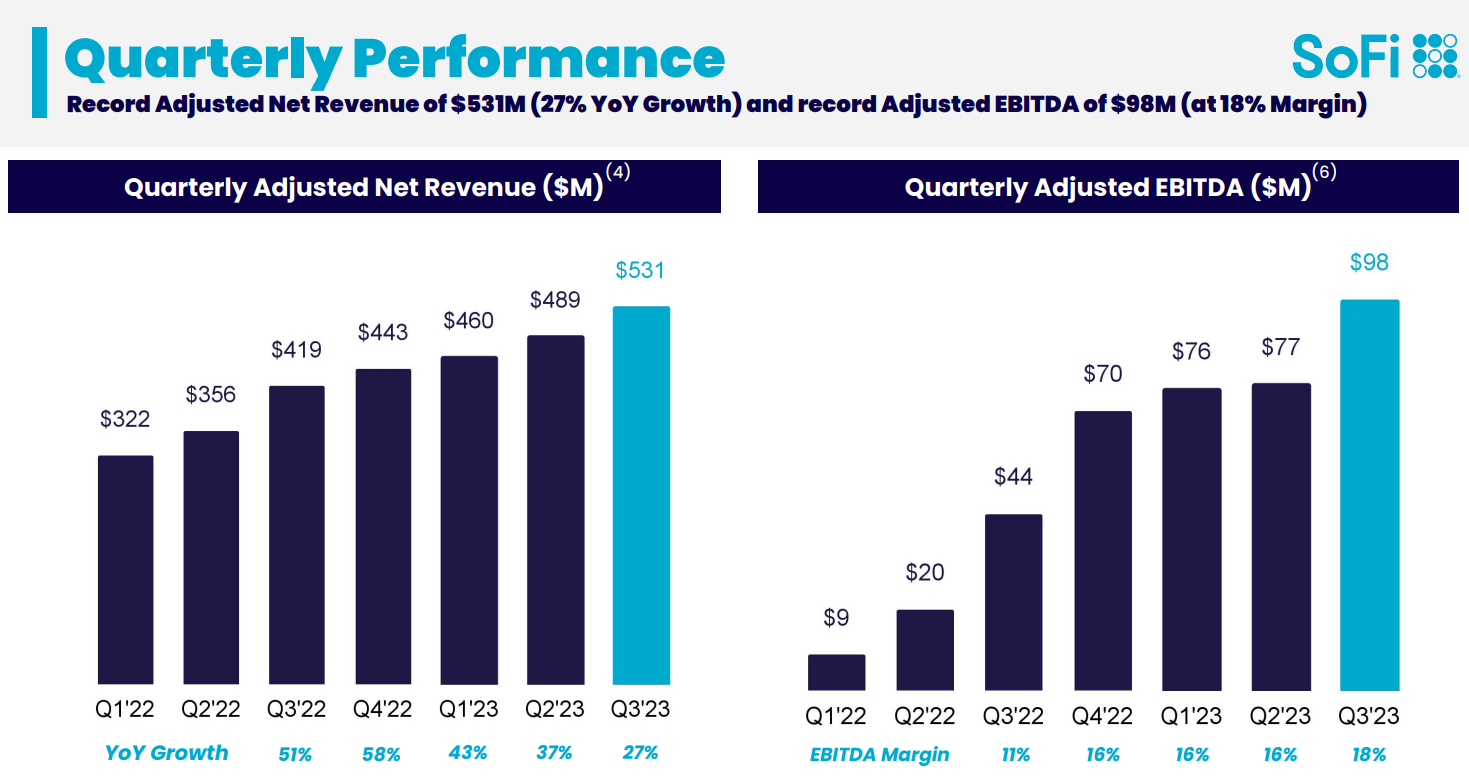

Q3 ulkona ja aiempi tahti vaan jatkuu ![]()

Q3 Earnings Release

Ja sijoittajapresis

SoFi Technologies Non-GAAP EPS of -$0.03 beats by $0.06, revenue of $537.2M beats by $21.64M

Q3 Non-GAAP EPS of -$0.03 beats by $0.06.

- Revenue of $537.2M (+26.7% Y/Y) beats by $21.64M.

- GAAP Net Revenue of $537 Million Up 27%; $531 Million Adjusted Net Revenue Up 27% Year-over-Year

- New Member Adds of Over 717,000; Quarter-End Total Members Up 47% Year-over-Year to Over 6.9 Million

- New Product Adds of Nearly 1,047,000; Quarter-End Total Products Up 45% Year-over-Year to Over 10.4 Million

- Total Deposit Growth of $2.9 Billion, Up 23% During the Third Quarter to $15.7 Billion

- $68 Million Growth in Tangible Book Value, $171 Million on a Trailing 12 Month Basis

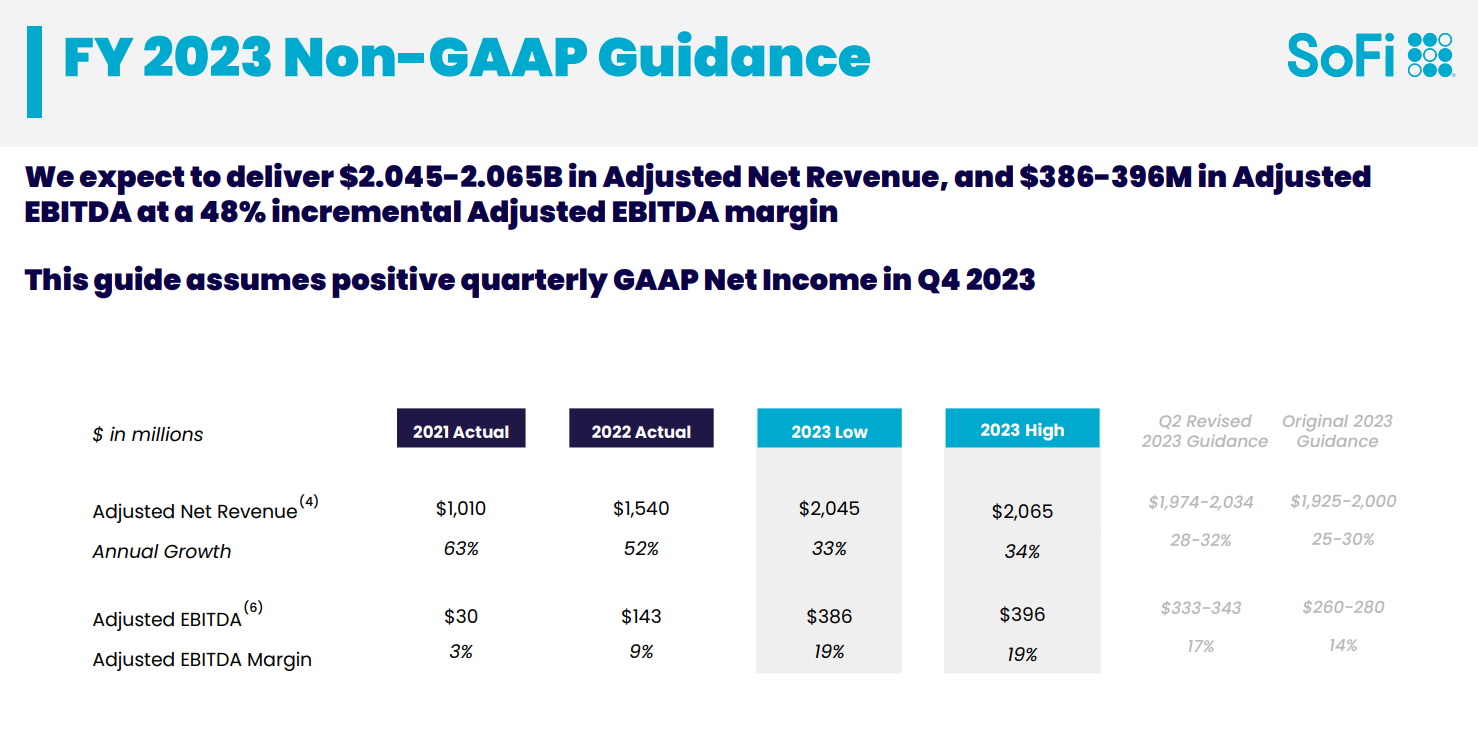

- For the full year 2023, management expects adjusted net revenue of $2.045 to $2.065 billion, up from its prior guidance of $1.974 to $2.034 billion, and full-year adjusted EBITDA of $386 to $396 million, up from its prior guidance of $333 to $343 million, representing a 48% incremental adjusted EBITDA margin and a range of 18.9% to 19.2% adjusted EBITDA margin.

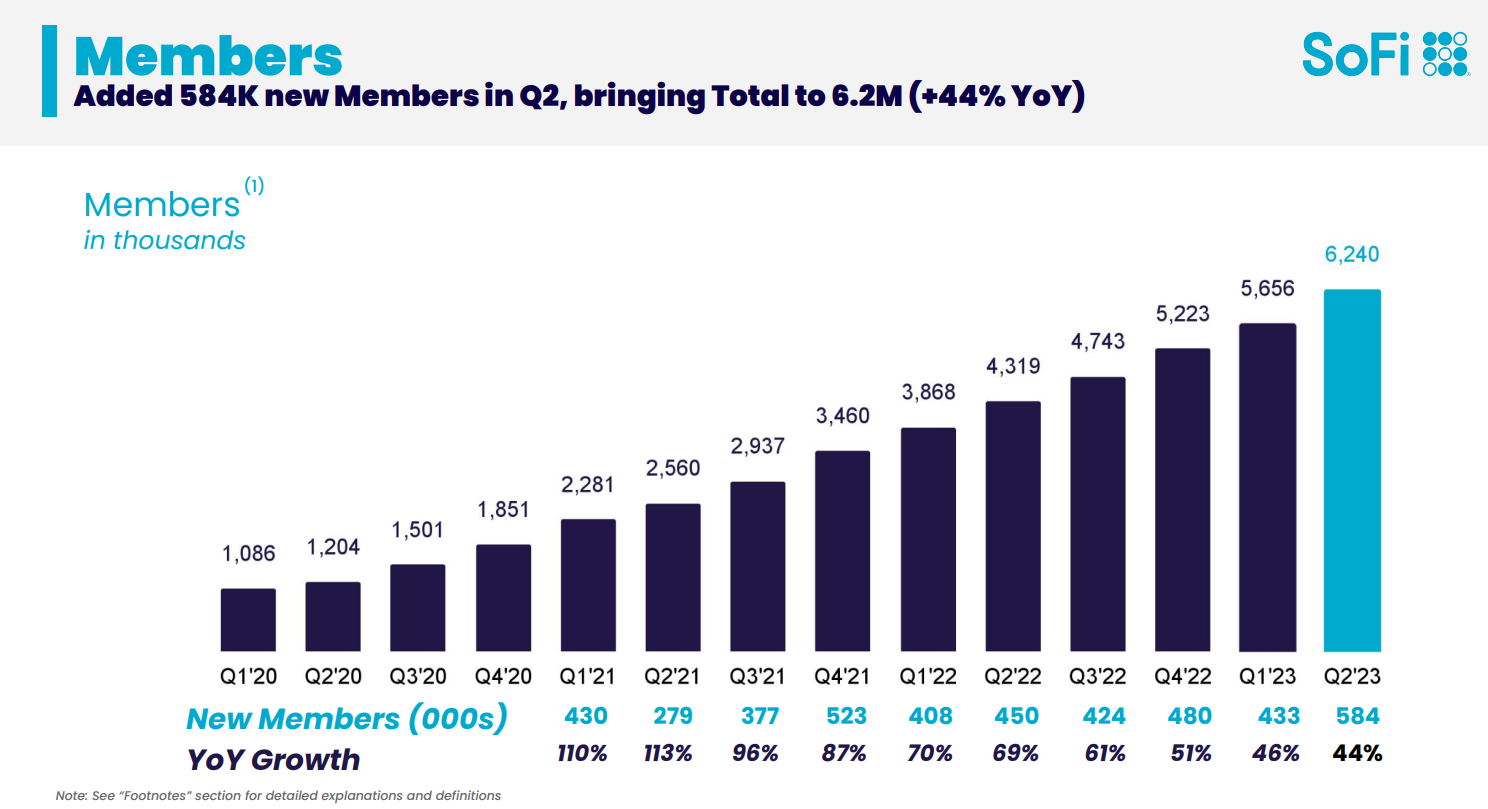

Käyttäjien lisäystä enemmän kuin aiemmin, jossain kohtaa luulisi hidastuvan.

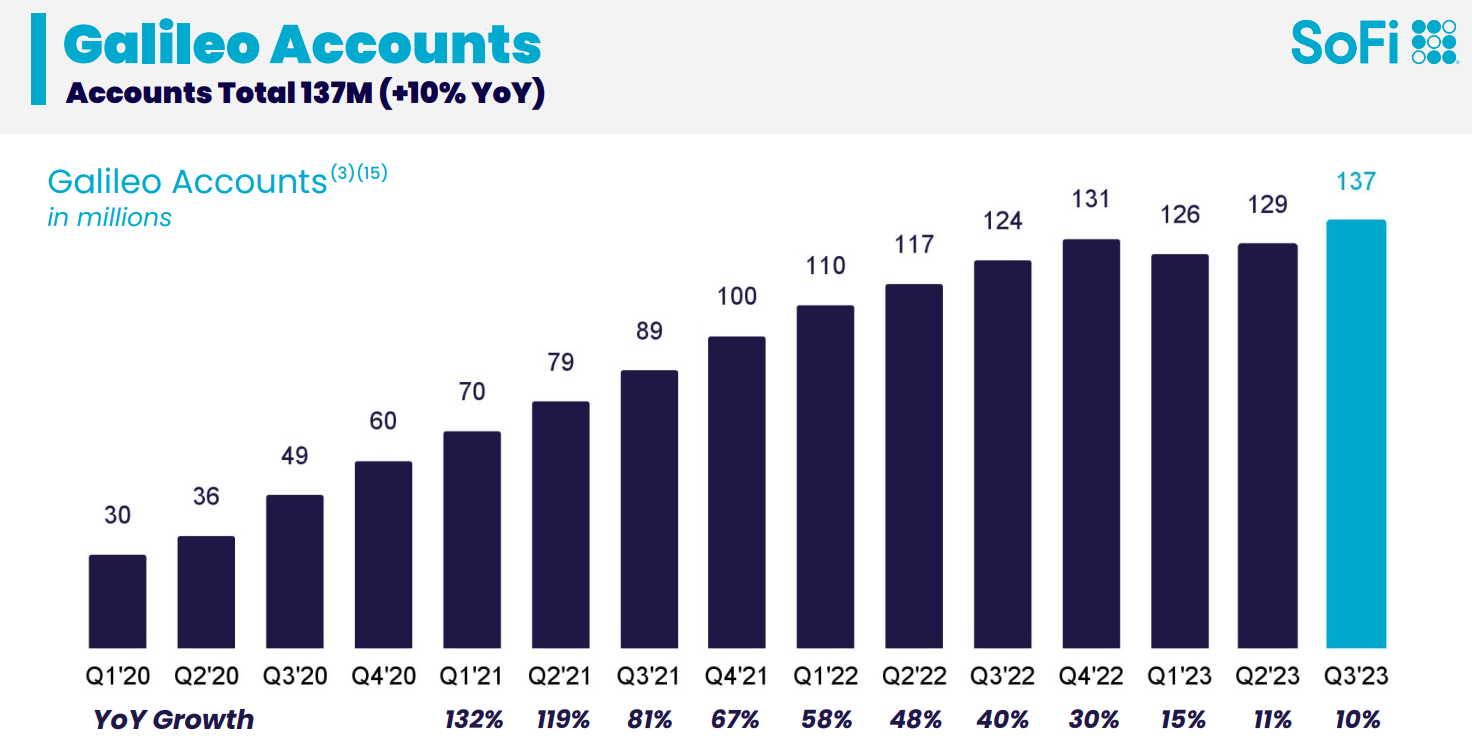

Myös Galileon tilit lisääntyi, siellä ollut pudostusta aiemmin

Nämä puhuu puolestaan ![]()

Ja näkymiä nostettu taas 2023:lle ![]()

myös GAAP positiivinen Q4 mainittu jälleen entistä vahvemmin

Ja tietysti tämä pitää taas nostaa esille:

As the company moves toward expected GAAP net income profitability in the

fourth quarter, management expects depreciation and amortization and share-based compensation expenses to increase in the mid-to-high single digit percentage range in the fourth quarter relative to third quarter results

14 tykkäystä

Jenkkianalyytikon näkemyksiä ensi vuoden osalta. Kolmessa minuutissa paljon asiaa:

8 tykkäystä

Kaikenlaisia kisoja ja palkintoja ![]() Mutta voitto on silti voitto

Mutta voitto on silti voitto ![]()

SoFi Wins 2 Banking and 1 Lending Awards, Highlighting Continued Commitment to Offering a Suite of Best-In-Class Products to Make SoFi Consumers’ One Stop Financial Shop*

SAN FRANCISCO–(BUSINESS WIRE)-- Today, SoFi (NASDAQ: SOFI), the digital personal finance company, received three 2024 Best-Of Awards from NerdWallet, Inc., a platform that provides financial guidance to consumers and small and mid-sized businesses (SMBs). SoFi was recognized by NerdWallet and selected as the Best Checking Account Overall and Best Checking Account for Overdraft Fee Avoidance for SoFi Checking & Savings, as well as Best Personal Loan Overall for SoFi Loans.

A team of trusted Nerds—composed of seasoned journalists and subject-matter experts—used a comprehensive scoring formula to objectively evaluate over 1,000 financial products. Top picks across Credit Cards, Personal Loans, Banking, Investing, Mortgages, Insurance, and Travel Rewards are featured in this year’s awards¹.

“Through our rigorous and objective evaluation process, we have selected SoFi as one of the best in banking and lending products,” said Kevin Yuann, Chief Business Officer at NerdWallet. “Consumers can trust that they’re getting one of the top products on the market to help meet their financial needs.”

9 tykkäystä

9 tykkäystä

Hyvin meni loppuvuosi:

Vähän parempaa eps estimaattia tälle vuodelle kyllä odottelin mutta katotaan, miten homma etenee…

Edit

Tässä vielä kalvot

Members sekä Galileo account kasvuluvut lupaavat kyllä hyvää jatkossa. Ja perinteisestihän ohjeistus on ollut konservatiivinen, joten varsin hyvältä tämä näyttää ![]()

16 tykkäystä

Samaan Q4 hehkutukseen on tuotu myös uutta palvelua tarjolle, joka kelpaisi kyllä täälläkin päin markkinaa. Edes ETF:iä ei saa ostettua, kun puuttuu suomenkielinen esite ![]()

Sofi sen sijaan tuo markkinoille pääsyn vaihtoehtoisiin sijoitusrahastoihin, rahastoihin ja rahamarkkinarahastoihin. Näin omistajan näkökulmasta voisi olla korkeampikin palkkio kuin 0,5% ![]()

Mutta eiköhän tuolla saada taas lisää asiakasvirtaa, jos vastaavien saatavuus muualla on rajattu vain jo ennestään rikkaille.

Initially, SoFi will offer over 6,000 different mutual funds to members on the SoFi Invest platform, as well as access to invest in the ARK Venture Fund, Carlyle Tactical Credit Fund (CTAC), KKR Credit Opportunities Portfolio (KCOP), as well as Franklin Templeton’s Clarion Partners Real Estate Income Fund (CPREX) and Franklin BSP Private Credit Fund (FBSPX). These funds feature a unique lineup of assets, including private credit, real estate and pre-IPO companies offering a diverse mix of investing opportunities. SoFi will roll out access to alternative investments, mutual funds and money market funds to all SoFi Invest members over the coming days.

SoFi will continue to be a leader in affordable investing by offering no SoFi transaction fees for mutual funds and no transaction fees for the new alternatives funds for the first 60 days. After this promotional period, SoFi will offer a competitive 0.50% purchase fee for the alternatives funds with low minimum investment.

13 tykkäystä

Asian Investor tuntuisi aiemminkin olleen hyvin perillä Sofin toiminnasta, Q4:n jälkeinen läpikäynti.

https://seekingalpha.com/article/4667009-sofi-stock-q4-earnings-proving-naysayers-wrong

Sofia varmasti painoi raportin jälkeen yleinen pankkisektorin myynti, mutta vastaava reaktio ollut viimeisten kvartaaliraporttien jälkeen. Raportista iso piikki ylös, joka myydään seuraavana päivänä alas.

11 tykkäystä

Just näin. Entistä laajemmat ja kohtuuhintaiset palvelut varmasti lisäävät niiden käyttöä ja houkuttelevat entistä enemmän uusia asiakkaita, jotka sitten käyttävät yhä enemmän SoFin palveluja, kuten tässä Lukenkin päivitetyssä artikkelissa todetaan:

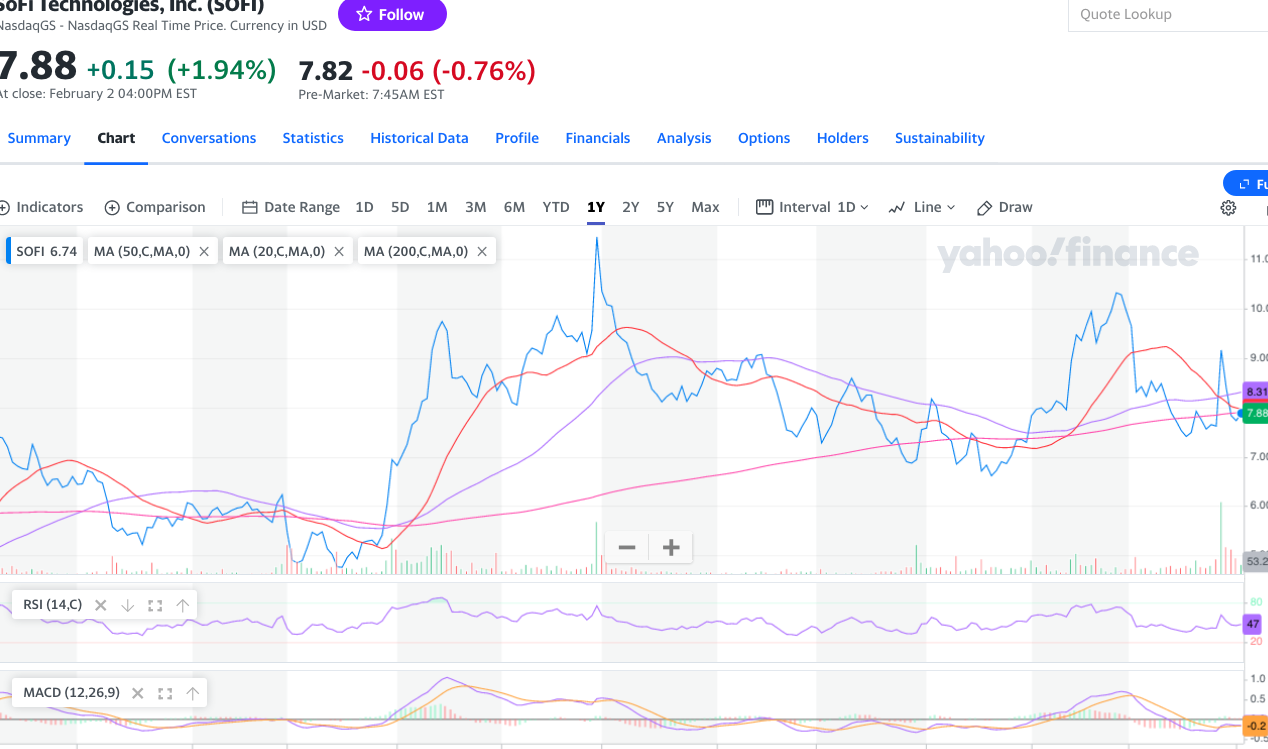

Vaikka hyvän rapsan jälkeen lyötiin taas lopulta tonttiin, edelleen ollaan nousevalla trendilinjalla, joka alkoi viime keväältä.

Kyllä SoFi varmasti on piikki lihassa monelle jenkkien investointi- ym pankille, jotka markkinalle suosituksiaan jakelevat. Esim Morgan Stanley downgreidasi juuri alipainoon. Deutsche Bank kuitenkin ihan eri linjoilla:

Tässä yksi lappu, johon tekisi mieli iskeä puolet salkusta. Mutta kun markkinapaikka on USA: manipulaation, ostettavan oikeuden ja valeuutisten kehto, on noudatettava SoFistikoituneempaa salkkustrategiaa ![]()

10 tykkäystä

Hyvin mielenkiintoinen toimitusjohtajan haastattelu. Käsitellään trendeistä strategiaan ja hyvin yksityiskohtaisiin asioihin esimerkiksi miten SoFi rakentaa oma brändinsä tunnettavuutta:

7 tykkäystä