Beyond Meat on varmaan ihan relevantti vertailukohde samasta skenestä. BYNDin 6kk ja 12kk kehitys markkinoilla ollut jopa TTCF:ää heikompaa. BYNDin osari tulee vissiin 11.5. ulos.

Haluaisin naiivisti uskoa, että yleinen epävarmuus Ukrainan sotineen ja globaaleine inflaatiouhkineen iskee ensimmäisenä tällaisiin marginaalisiin tuotealoihin. Lehmänhermoja vaan Voin toki olla fataalisti väärässäkin…

First Quarter 2022 Financial Overview Compared to 2021 First Quarter

Revenue rose 37.3% to $72.1 million

Tattooed Chef branded product revenue increased 21.2% to $43.5 million, or 60% of total revenue

Adjusted EBITDA (1) was negative $13.4 million

Net loss was $17.6 million

First Quarter 2022 Operational Highlights

Branded SKUs rose to 90 as of March 31, 2022 from 78 as of December 31, 2021

Added more than 10,000 new points of distribution

Commenced production of frozen, ready-to-eat Mexican food items

Enterprise-wide automation initiative underway and expected to be completed by the end of 2022

Additional Operational Highlights

Branded oat butter bars set to commence production in Q2 2022

Cold storage facility operational April 2022

Inflaatio syö kyllä pohjaa pois.

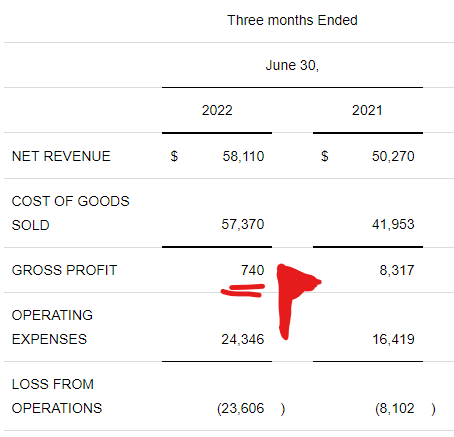

Gross profit was $8.2 million in Q1 2022, or 11.3% of revenue, compared to $7.2 million, or 13.7% of revenue, in Q1 2021. The decline in gross profit margin was due to a greater increase in cost of goods sold than the increase in revenues as a result of inflationary pressures.

Tappiot tuplattu vuodentakaiseen

Net loss was 17.6 million, or (0.22) per diluted share, as compared to a net loss of 8.2 million, or (0.11) per diluted share, in Q1 2021.

Näkymät 2022, kassa loppuu pian tällä tahdilla, 57M$ lyhytaikaisia varoja maaliskuun lopussa tiedotteen mukaan

Full Year 2022 Outlook

The Company reiterated its outlook for 2022:

Revenue of $280-$285 million, driven by a combination of new product introductions, an increase in retail distribution via new relationships and penetrating existing accounts compared to 2021, and contributions from acquisitions consummated in 2021.

Gross margin of 10-12%

Marketing expenses of $27- $32 million

Capital expenditures of approximately $20 million, with investments focused on automation and robotics at our manufacturing facilities.

Kasvua on toki paljon, uudet tehtaat toiminnassa, 10000 uutta myymälää. Bruttokate on vaan olematon aiempaan verrattuna, joten kannattavuus kärsii pahasti.

Transskripti luettavaksi, jos maistuu. Itse jätän nyt väliin, katsellaan myöhemmin uudestaan

Taitaa TTCF olla vähällä kiinnostuksella, mutta päivitellään nyt silti

Lyhyesti: Inflaatio puree pahasti. Liikevaihto kasvaa, mutta kulut vielä enemmän.

Full Year 2022 Outlook

Based on the current business environment and outlook for the remainder of the year, the Company is reiterating guidance on revenue, marketing and capital expenditures, and lowering guidance with respect to gross margin:

Revenue of $280-$285 million, unchanged from prior guidance.

Gross margin of 8-10%, down from prior guidance of 10-12%, due to continued cost inflationary pressures and the timeline for implementation of automation initiatives at our facilities.

Edit:

bruttokate ollut heikko jo tähän mennessä, mutta nyt on myyty melkein samalla kuin ostettu. Jotta alkaa olemaan mielekästä, niin tarvitaan 20-30% korotukset, jotka sitten alkaa näkymään myyntihinnoissa ja sitä kautta menekissä. Vaikea markkina, toivottavasti saa tuotantokuluja skaalattua merkittävästi alaspäin

Lisää valmistuskapasiteettia, uusia tuotteita ja Walmartin jakelu laajenee merkittävästi.

Under the agreement with Walmart, Tattooed Chef will increase the brand’s frozen shelf presence from 5 to 13 SKUs and expand the availability of these 13 SKUs from an average of 300 Walmart stores to an average of 2,000 Walmart stores. Initial availability of Tattooed Chef’s products at these new Walmart locations is expected no later than October 2022.

The Company anticipates the operations of this new facility will be cashflow neutral through the remainder of 2022 and be accretive to earnings by the start of 2023.

The firm expects 2022 revenue of $235M-$245M, well below consensus estimate of $281.20M. Its prior guidance was $280M-$285M.

2022 gross margin is projected to be 0-3% vs. earlier forecast of 8-10%, driven by continued cost inflationary pressures and impacts from the multi-vendor mailer reclassification from operating costs to contra revenue as well as lower revenue.

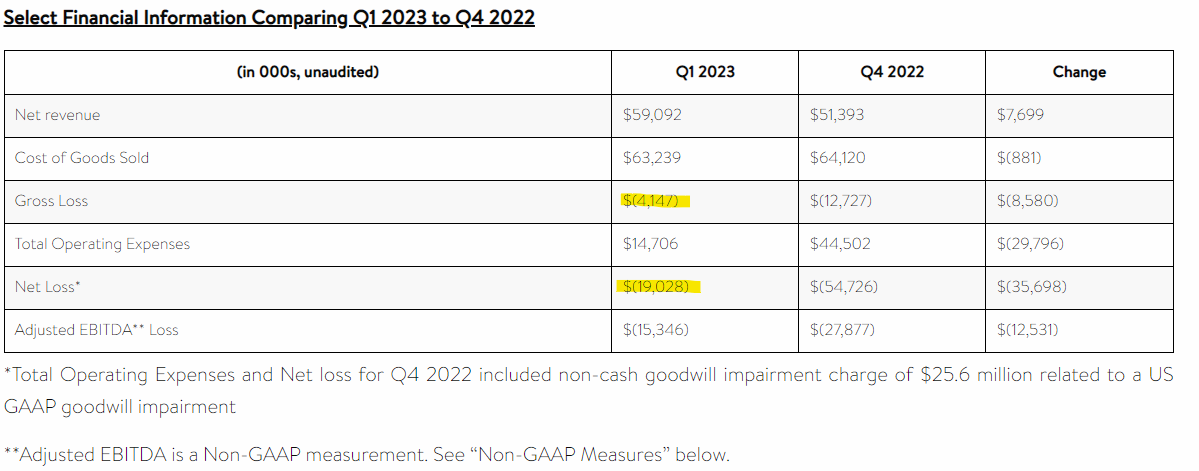

Tattooed Chef (TTCF) reported preliminary Q3 net revenue of $54.1M (-6.7% Y/Y), widely missing consensus estimate of $72.96M. Preliminary net loss was $38.3M vs. $8.3M in Q3 2021.

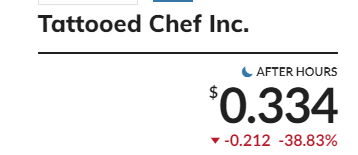

Rahat loppu.

"At March 31, 2023, cash was $3.5 million compared to $5.8 million at December 31, 2022 and the net amount drawn on the Company’s line of credit was approximately $4.0 million during Q1 2023.

"

…

“The Company is seeking to raise additional debt or equity capital in the near future”

Huonolta näyttää. Lainojen kovenantit ovat jo paukkuneet ja lainoittajat voivat vaatia koska tahansa lainojen välitöntä takaisinmaksua. Eikös tämä firma ollut mediassa esillä aika paljon yhteen aikaan?