Näkeekö jostain avoinna olevien warranttien päivämäärän ja hinnan? Mihin asti myydään, ennenkuin ”even”?

Ei varmastikaan ainoa syy, jos ollenkaan, mutta olisi hyvä tietää.

Näkeekö jostain avoinna olevien warranttien päivämäärän ja hinnan? Mihin asti myydään, ennenkuin ”even”?

Ei varmastikaan ainoa syy, jos ollenkaan, mutta olisi hyvä tietää.

Ginnie Mae jatkoi uusien MSR kauppoja koskevien rajoituksien käyttöönottoa vuodella. Ilmeisesti nämä rajoitukset tulevat vähän hidastamaan MSR kauppaa. Piti tulla käyttöön 2023 lopussa, mutta tuleekin vasta 2024. Ei kyllä ymmärrystä tarkemmasta vaikutuksesta, mutta koska BWn tj Al Qureshi peukuttaa tätä uutista LinkedINssä, niin pakko tämän on olla hyvä juttu ![]()

Ja lainojen prepaymentit 22 vuoden pohjissa. Tämä oli MSRien suurin riski refinancen kanssa.

Ihan mielenkiitoista mutuilua Kanadan foorumilta.

Voxtur on eilen antanut 304 359 optiota Christopher Mallon nimiselle kaverille. Oletettavasti on siis aloittanut työt Voxturilla, vai voiko optioita antaa kenelle tahansa? Nimimerkki helterskelter osaa kertoa että kaveri on töissä Group9 -nimisessä firmassa.

Group9 nettisivut on rumat kuin synti (Group9 Insurance Solutions), mutta löytyy esim vanha nettiartikkeli joka kertoo, että jo vuona 2004 kaveri oli rakentanut aika menestyksekkään firman.

https://www.bizjournals.com/philadelphia/stories/2004/10/25/focus5.html

Mutta se mielenkiintoinen osuus alkaa kun katsoo tätä SingleSourcen tiedotetta ACTista.An Attorney Opinion Letter Offers Similar Protection As A Title Insurance Policy – PROGRESS in Lending

Sieltä löytyy kappaleet: “ACTs™ are available on loans up to $1 million. Each ACT™ is backed by a Mortgage Service Providers Errors & Omissions (E&O) insurance policy issued by carriers that are A-rated by AM Best. The policies cover the full value of the loan for the life of the loan and are fully transferrable in the secondary market. Both SingleSource and law firms issuing ACTs™ are covered by the policies as service providers, with the lender named as a third-party beneficiary.”

“We have had a great relationship with SingleSource over the years providing a number of warranty products,” said Chris Mallon, Executive Vice President of Group 9 Insurance Solutions, an E&O policy provider based in Pennsylvania. “We are excited to expand our partnership to provide this new and innovative offering to the industry.” Jos siis oletetaan, että kyseessä on nyt sama kaveri.

Olisikohan Voxturin tarkoitus ottaa/kehittää myös tuo vakuutusosuus itselleen, vai mitä tässä voisi olla takana?

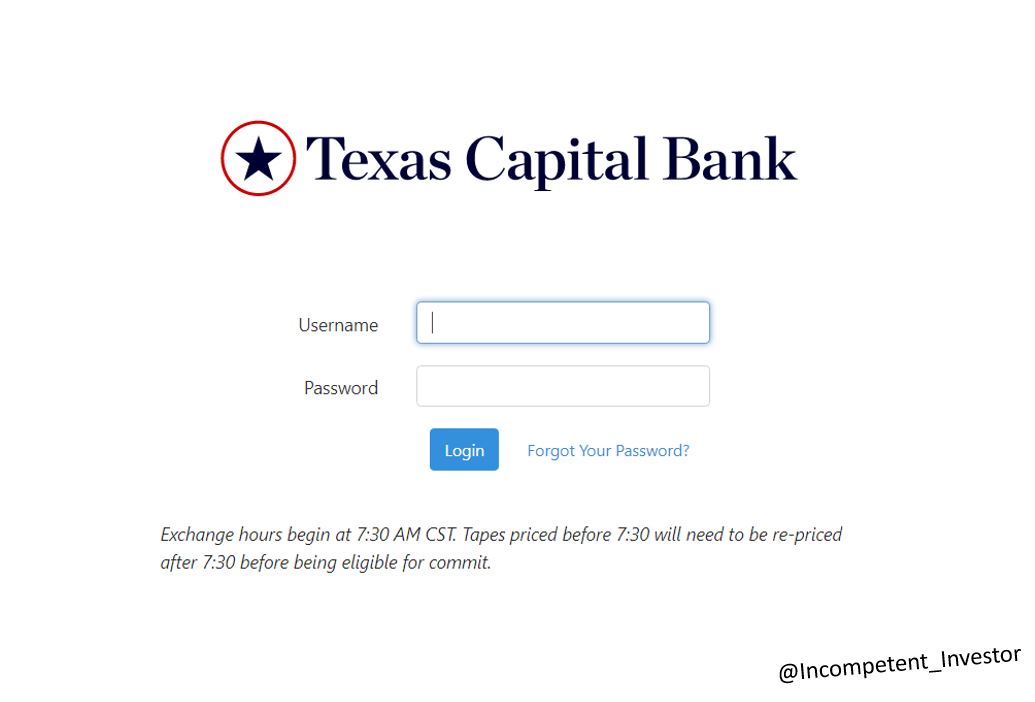

Uusi Blue Water -asiakas jälleen: Texas Capital Bank ![]()

En ole täysin varma, onko tämä palvelu jo tuotannossa vai vielä työn alla.

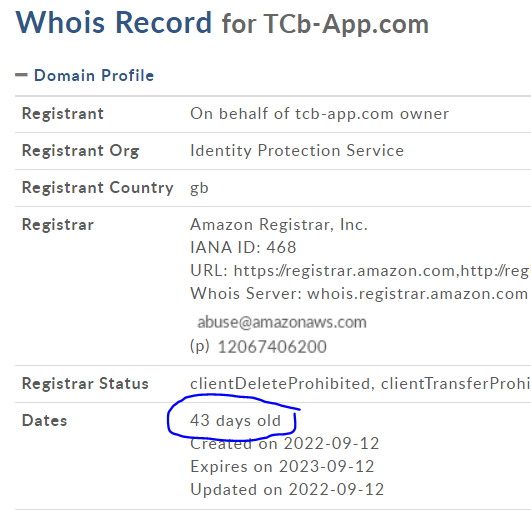

Pakko kysyä että mistä tiedät uudeksi asiakkaaksi? Domainin rekisteröinnistäkö?

Joo, domain on viime kuulta. Mutta on toki periaatteessa mahdollista, että olisi ollut aiemminkin asiakkaana ja vaikka eri osoitteessa ![]()

Ei taida mitään uutta olla tälläkään videolla mutta on tuolla kanavalla sentään 50k tilaajaa.

Nopeimmat olivat varmaan ehtineetkin jo nuuhkia tätä, mutta laitetaas tänne vielä.

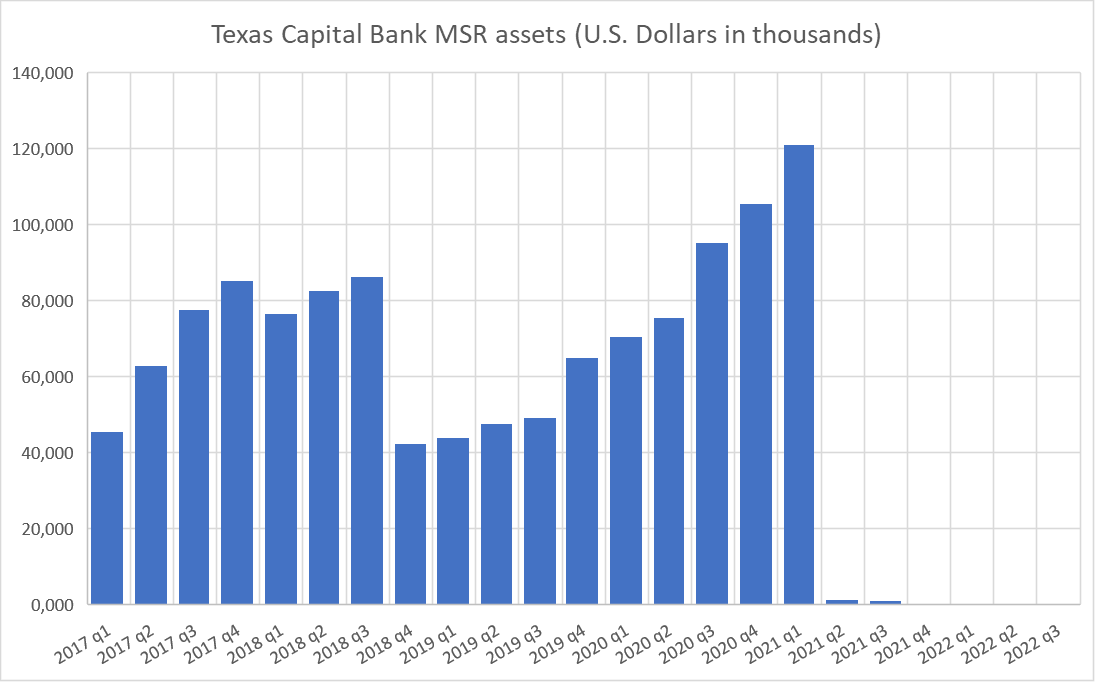

Tarkoitus oli vähän kartoittaa mikä vaikutus tuolla Texas Capitalilla olisi BW:lle, eli kävin läpi sen MSR assetit 2017 alkaen ja piirsin kuvan niiden arvosta eri hetkillä (tuossa tuo pilkku jenkkityyliin tuhansien erottimena, ei suomalaiseen tapaan desimaalien eroittimena ja arvo tuhansissa jenkkidollareissa):

Jimbo mainitsee Markun haastiksessa MSR:n liittyen (kohdassa 1:45), että MSR:n keskimääräinen arvo on $2700/kpl, eli karkeasti voisi varmaan arvioida, että MSR:ien määrän saa jakamalla tuosta kuvasta 2,7:llä(?)

Tosin tuosta ei hirveän helposti pysty arvioimaan mikä on MSR-transaktioiden määrä, ellei tiedä tarkemmin mikä on niiden vaihto (paljonko syntyy vs. paljonko myydään milläkin hetkellä), mutta jotain hahmotusta suuruusluokasta tuo kuitenkin varmasti antaa. Parhaat tilanteet BW:lle lienee, kun tullaan korkealta palkilta matalammalle.

2021 q4 - 2022 q2 rapsoissa oli erikseen mainittu MSR:n myynneistä, eli nyt trendi on se että myydään kaikki aikalailla sitä mukaa kuin niitä syntyy, mikä käy järkeen tässä markkinassa.

Tässä joku pidempi juttu msr-markkinoiden tilanteesta. Ikävästi en pääse lukemaan kun on ilmaiset artikkelit jo luettu. Jos joku referoi mikäli on jotain referoitavaa?

Kyllä vaan MSR kaupoilla Mr Cooper teki tulosta kun origination puoli kutistuu.

“The company also posted a $122 million gain, with mark-to-market mortgage servicing rights propelled by rising interest rates and a drop in loan-prepayment speed, which in turn amplified the value of MSRs because they pay out over a more extended period.”

Ja lisää MSRiä meinaavat hankkia.

“The Dallas-based Mr. Cooper posted a record level of liquidity of about $2.3 billion, which it will use for working capital needs and MSR acquisition, executives said.”

Toivottavasti käyttävät BWn alustaa kaupankäyntiin ainakin jatkossa. Eikös MrCooperilla ollut Voxturin osakkeitakin?

E. Oli XOme kaupoista ja on edelleen koska lockup period 4 vuotta 2021 tehdyistä kaupoista.

https://www.vendorsurf.com/news/voxtur-buys-xome-from-mr-cooper-kta57zh0

@Incompentent_Investo tiedetäänkö me onko MrCooper BWn asiakas? ![]()

Ei ole varmaan ainakaan tuollainen white label -asiakas toistaiseksi, siitä ei sitten oikein jää jälkiä jos käyttävät Blue Waterin omissa nimissä olevaa kauppapaikkaa ![]()

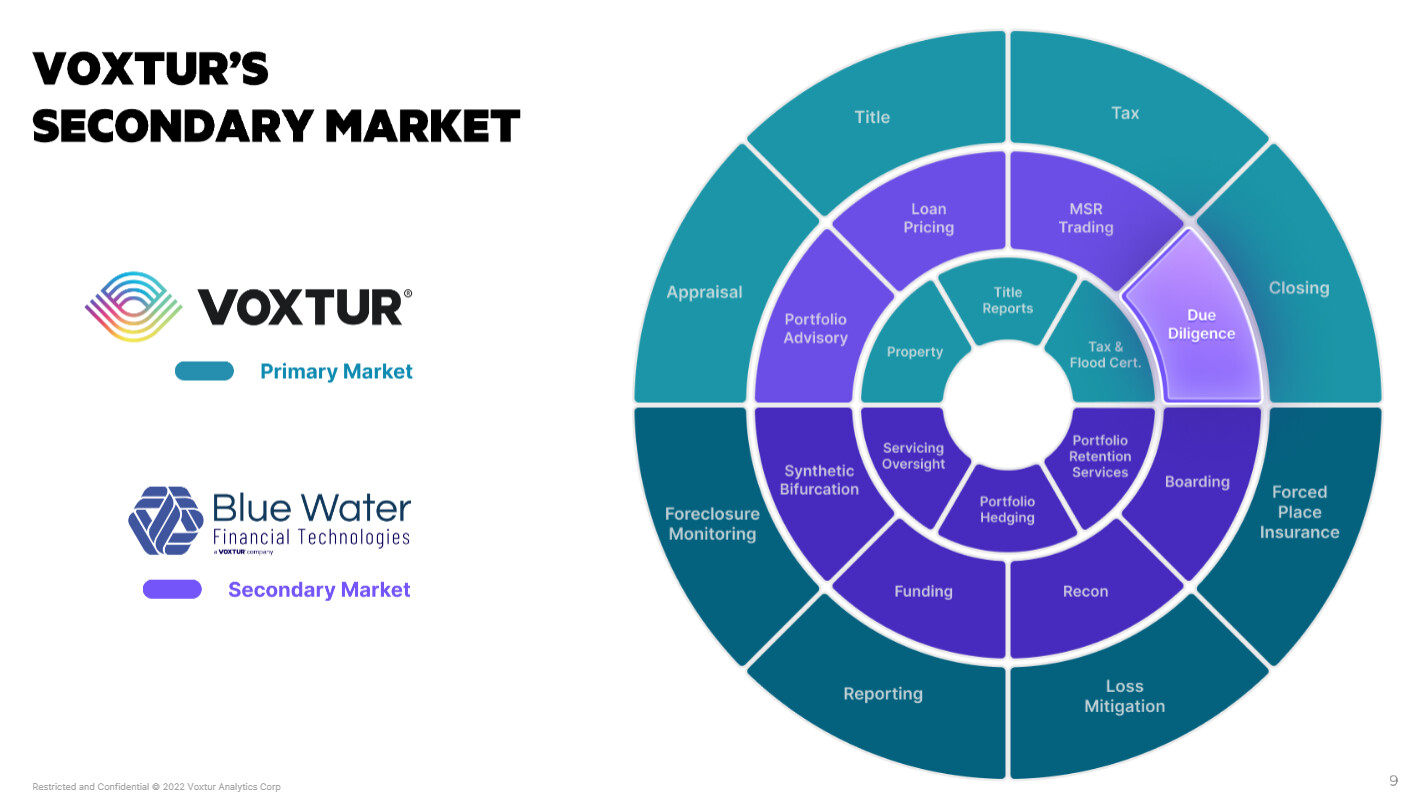

Kuuntelin muuten tänään vasta tuon uusimman haastattelun (oli myös Spotifyssä audio-muodossa), ja siitä löytyi selitys kun ihmettelin aiemmin miksi uudessa investor deckissä oli tuo due diligence -laatikko korostettuna ihan omana kalvonaan.

Haastattelussa selvisi että tuo on se kohta, missä Voxturin aiemmat palvelut liittyvät Blue Waterin secondary marketille tarjoamaan palveluun. Eli jos joku haluaa ostaa parilla sadalla miljoonalla MSR:iä, niin he eivät halua luottaa pelkästään myyjän aiemmin tekemään arvonmääritykseen ja title searchiin, ja Voxtur pystyy tässä tarjoamaan ne palvelut.

EDIT: toinen juttu mikä korostui kommenteissa oli että nyt tarvitaan aikaa sekä Blue Waterin ja Voxturin rajapintojen integrointiin että AOL-käyttöönottoon. AOL:lla on “noin kaksitoista” asiakasta, mutta mielestäni myös Gary ja/tai Jim varoitteli tuosta käyttöönoton hitaudesta, eli varmaan aika hidas ramp up -jakso menossa kun tuota niin korostetaan.

Ihan mielenkiintoinen artikkeli on kyllä. En kuitenkaan jaksa referoida, niin alla copy-paste ![]()

E. @Incompentent_Investo on aikaisemmin antanut vahvan mutun, että esim tuo Freedom Mortgage, eli toiseksi suurin MSRien kaupankävijä tänä vuonna olisi BWn asiakas ![]()

The MSR sector continues to shine, but there is a looming concern

If the economy worsens, loan delinquencies in Ginnie Mae mortgage servicing portfolios will accelerate

October 24, 2022, 10:00 am By Bill Conroy

The mortgage-servicing rights market just keeps on ticking even as the overall housing market takes a licking. And while depository banks that are fueling that growth, concern is mounting over Ginnie Mae MSRs held by nonbanks.

Mortgage advisory firms **Prestwick Mortgage Group **and partner Mortgage Capital Trading (MCT); Incenter Mortgage Advisors; and **MIAC Analytics **are out with a total of 10 bulk mortgage-servicing rights (MSR) offerings with bid-due dates in October. The 10 offerings together involve Fannie Mae, Freddie Mac and Ginnie Mae loan pools valued collectively at $12.77 billion.

MIAC is handling one of those bulk offerings, one of the largest, valued at $2.44 billion and involving a combination of Fannie, Freddie and Ginnie MSRs.

Prestwick is marketing four separate deals, two in partnership with MCT, valued in total at $2 billion — which together also feature MSRs for single-family residential loan pools from all three agencies.

What’s happening in an inflationary environment is everything’s getting more expensive.

TOM PIERCY, MANAGING DIRECTOR OF INCENTER MORTGAGE ADVISORS

Incenter has the highest deal count and the largest deals by volume, at five offerings valued collectively at $8.33 billion, Together they involve MSRs for single-family mortgage pools across all three agencies. Two of those offerings, one an all-Ginnie package and the other a Fannie and Freddie bulk offering, each involve loan-servicing pools valued at $4.1 billion.

Over the first nine months of this year, banks have far outstripped nonbanks in buying up MSR packages. Banks have been net purchasers of MSRs, to the tune of $107.8 billion — compared with $51.1 billion for all of 2021, according to a report by mortgage-data analytics firm Recursion.

Tom Piercy, managing director of Incenter Mortgage Advisors, said many independent mortgage banks stockpiled huge volumes of low-rate loans in 2021, understanding that rates would eventually rise, and they are cashing in on the new rate environment — a climate that also is wreaking havoc on loan-origination volumes. In addition, banks who are now buying, he added, can take advantage of the product cross-selling opportunities through loan servicing and, more importantly, they can leverage the escrow float opportunities MSRs offer.

“The deck is stacked in favor of the depositories when it comes to owing MSRs, and that is because of what they can do with the escrow [accounts],” Piercy explained. “Banks can leverage these [escrow] deposits [using them as collateral to borrow] through the Federal Home Loan Banks to reinvest into higher yielding assets.

“And so that’s why banks have always been in a much better position to own the MSRs.”

Digging down deeper into the numbers, the Recursion report shows that over the first nine months of 2022, banks have been net buyers of Fannie Mae and Freddie Mac MSRs and net sellers of Ginnie Mae MSRs, while nonbanks are selling off Fannie and Freddie MSRs and still far outstripping banks in issuing and buying Ginnie Mae MSRs.

In stark contrast to banks, nonbanks had a legacy portfolio of $1.77 trillion Ginnie Mae MSRs as of the end of September, the Recursion report shows. That’s more than five times the size of the banks’ aggregate Ginnie MSR portfolio of $334 billion as of the same date. Those Ginnie MSRs, however, represent a weak link in the nation’s housing system when the economy is under stress, as it is now.

Ginnie serves as the government-backed securitization pipeline for loans insured by government agencies that provide loan-level mortgage-insurance coverage through their lending programs. Unlike Fannie and Freddie, however, Ginnie does not purchase loans.

Rather, under the Ginnie program, lenders originate qualifying mortgages that they can then securitize through the agency. Ginnie guarantees only the principal and interest payments to purchasers of its bonds, which are sold worldwide.

The underlying loans carry guarantees, or a mortgage insurance certification, from the housing agencies approving the loans — which include single-family mortgages backed by Federal Housing Administration (FHA), the U.S. Department of Agriculture’s Rural Development program, the U.S. Department of Housing and Urban Development’s Office of Public and Indian Housing and the U.S. Department of Veterans Affairs (VA).

The largest volume of loans, however, is delivered through the FHA and VA lending programs.

The holders of Ginnie Mae MSRs, primarily nonbanks today, are the parties responsible for assuring timely payments are made to bondholders. And when the underlying loans go unpaid due to delinquencies, those servicers still must cover the payments to the bondholders.

And in the FHA program, in particular, according to Richard Koss, chief of research at Recursion, 30-day loan delinquencies have been ticking up since the beginning of the year. The same is true, but to a lesser degree, for the VA program, he said.

As of September, the 30-day delinquency rate for FHA loans stood at 3.77%, up from 3.02% as of the beginning of the year, Recursion data shows. The overall FHA delinquency rate — for loans 30-days late or more, excluding foreclosures — stood at 8.85% as of the second quarter of this year, compared with 4.22% for VA loans and 2.64% for conventional loans, according to the Mortgage Bankers Association.

It’s a source of concern I don’t think is broadly understood. The main mitigating factor is the still-huge amount of equity most buyers have in their homes.

RECURSION’S RICHARD KOSS ON GINNIE MAE MSR RISKS.

“The demographic of the FHA borrower is the first-time homebuyer, with very little to no down-payment,” Piercy explained. “The profile has shown over the years to be susceptible to poor performance when national economic numbers start slowing.

“And what’s happening in an inflationary environment is everything’s getting more expensive.”

The deep downside risk for nonbanks holding a large volume of Ginnie Mae MSRs is loan defaults. Defaults kick in the underlying loan insurance provided through the agency guaranteeing the loan, such as FHA. Another wrinkle in the picture for the short-term for mortgage servicers is that in most cases, borrowers can still “request an initial COVID hardship forbearance as long as the COVID-19 National Emergency is in place,” according to the Consumer Financial Protection Bureau.

Although principal recovery is ultimately guaranteed through FHA in the event of a default, there often is a bureaucratic time lag in obtaining interest due, according to a report by Kroll Bond Rating Agency (KBRA). In addition, interest rate recoveries are at the HUD debenture rate, “which is typically substantially below the loan note rate,” according to KBRA. That could potentially create cash-flow issues for some of the nonbanks holding the Ginnie MSRs.

“Yes, it’s a source of concern I don’t think is broadly understood,” Koss said. “The main mitigating factor is the still-huge amount of equity most buyers have in their homes.

“It’s the most recent cohort of buyers [with the highest-rate loans] that can be struggling with this to a large degree.”

Piercy, however, said the nonbanks originating the loans and issuing the Ginnie Mae securities are prepared to handle an uptick in defaults, which he said has been anticipated by the industry.

“I don’t think you’re going to see the calamity of the Great Recession,” Piercy said. “These servicers have acted very responsibly in fortifying balance sheets and anticipating what their capital requirements will be.

“So, delinquencies will increase, and there’s really little to no modification capabilities right now because of where interest rates are. And home prices will devalue, so we’re going to have a decrease in home prices, and that means default curves will pick up, and [MSR holders, like the nonbanks] will have to run those [payment] advances, and all of these services are aware of this and are positioned to handle it.”

Whether Piercy’s prediction will hold true remains to be seen, but it is the case, he said, that much of the all-agency MSR sale activity we are seeing now still involves loans made at lower interest rates, which Koss points out are at lower risk of default than the higher-rate loans just now coming into the nation’s mortgage pipeline.

Overall, the MSR asset should remain strong in 2023, because most of the servicing holders have built very low WAC [weighted average coupon] portfolios that should experience favorable [low] prepayment speeds.

BILL SHIRREFFS, SENIOR DIRECTOR AT MCT

“So much servicing was stockpiled in 2021 by all originators because of what they perceived as the historical low rates and the inequitable value that was being offered for it at the time,” Piercy said. “They knew … rates were going to spring back in some capacity at some point, and sure enough, that’s what they began to do the first quarter of 2022.”

In fact, the weighted average interest rates for the loan pools for the nine MSR deals being marketed by Incenter, Prestwick/MCT and MIAC, reflect those lower rates from last year. The rates in those MSR offerings range from 2.94% to 4% — with the higher rate involving a Ginnie Mae MSR bulk-servicing offering being marketed by Incenter. The average rate for a 30-year fixed mortgage as of Oct. 13 was 6.92%, according to Freddie Mac’s Primary Mortgage Market Survey.

“Overall, the MSR asset should remain strong in 2023, because most of the servicing holders have built very low WAC [weighted average coupon] portfolios that should experience favorable [low] prepayment speeds,” said Bill Shirreffs, senior director and head of MSR services and sales operations at MCT.

Leo Wong, a partner with Waterfall Asset Management, a global alternative investment manager with some $11 billion in assets under management, said the MSR market is still strong, but concedes some of the froth is starting to settle. He said prices for MSR offerings reached multiples of “around 5.5 in the second quarter of this year,” but are now in the “high 4s” and likely “to dip into the low 4s in the fourth quarter.”

A multiple is a measure of the price of an MSR loan pool expressed as percentage of the unpaid principal balance divided by the servicing fee.

Tom Capasse, managing partner and co-founder of Waterfall Asset Management, said the downward pricing dynamics in the MSR market currently are being driven by the fact that there’s more supply than demand. “There’s more sellers and a fixed amount of buyers,” he added.

Piercy echoed Wong and Capasse’s analysis.

“We just don’t have the pricing that we did in the first half of the year,” he said. “But we still now have reasonable pricing for an asset that does provide value to the purchasers,” Piercy said. “MSR volumes and activity remain robust.”

Shirreffs added that MSR portfolios grew substantially in 2020 and 2021, “and the revenue generated from those portfolios has undoubtedly softened the blow of dramatically reduced mortgage production revenue.”

“But a number of factors will impact the MSR asset materially in the coming year,” he added. “The cost of servicing continues to rise, particularly labor cost.

“With sustained lower production volumes and higher servicing costs, this could potentially lead to increased M&A [merger and acquisition] activity during 2023 and 2024.”

The top buyer of MSR portfolios overall (all three agencies combined) year to date through September 2022 was J**.P. Morgan Chase**, $99.9 billion, Recursion data shows. Freedom Mortgage was second, at $96.8 billion, followed by Onslow Bay Financial LLC [a subsidiary of Annaly Capital Management], $82.2 billion.

Mr. Cooper, at $78.8 billion, and Lakeview Loan Servicing, $72.5 billion, rounded out the top five purchasers over the period. The top sellers over the first nine months of 2022 for all-agency MSR portfolios were United Wholesale Mortgage (UWM), $107.4 billion; Home Point Financial Corp., $68.9 billion; Rocket Mortgage, $50.5 billion; loanDepot, $25.3 billion; and AmeriHome Mortgage Co., $22.9 billion.

Wells Fargo is the largest holder of all-agency MSRs based on loan principal balance, $615 billion as of the end of September, or 7.4% of the market, followed by Pennymac, at $515.5 billion, 6.2% market share; and J.P. Morgan Chase, $488.4 billion, a 5.9% market share, Recursion data shows.

For Ginnie Mae MSRs only, as of the end of September, Freedom Mortgage led the pack, with a $253.1 billion portfolio, or a 12% share of outstanding Ginnie MSRs based on loan-pool principal balance. Pennymac was second, at $241.8 billion, 11.5%; followed by Lakeview Loan Servicing, $239.1 billion, and an 11.4% slice of the market.

Freedom’s portfolio accounted for 14.4% of all Ginnie MSR loan delinquencies 30 days or more past due as of the end of September, according to Recursion. For Pennymac, the same loan-delinquency ratio was 10.3%; for Lakeview it was 13.8%. Overall, nonbank’s portfolios combined accounted for 88.4% of Ginnie MSR loan delinquencies 30 days or more overdue as of the end of the third quarter, according to Recursion.

In total, as of the same date, banks controlled 15.9% of the Ginnie MSR market, with nonbanks held an 84.1% market share, according to Recursion.

Vahvistettakoon muuten myös että Amerihome on 100% varmuudella Voxturin AOL asiakas! ![]()

Amerihome on #1 Correspondent lenderi: Scotsman Guide (kiitokset @Incompentent_Investo lle tästä listasta)

" What Is Correspondent Lending?

Correspondent lending happens when a lender originates and funds a mortgage, but then sells it typically to Fannie Mae or Freddie Mac or a government entity like the FHA or VA. These agencies then will package the mortgages and sell to investors as mortgage-back securities.

Correspondent lending helps the mortgage industry overcome many of the problems inherent in portfolio mortgage lending. Portfolio mortgage lending involves a lender giving you money for a mortgage and then holding that loan for up to 30 years while waiting for the mortgage to be paid off at the end of the loan term."

Ei ole tietoa, että onko Amerihome myös BWn MSR asiakas, mutta loogistahan se olisi. Edelliseen postaukseen liittyen Amerihome on myös yksi suurimmista MSR kauppiaista.

Onko 100 % varma? Tai siis mistä tiedetään. Voxtur ei ole käsittääkseni ainut AOL-tarjoaja, vaan esim. https://ititletransfer.com/ tarjoaa samanmoista setuppia.

Kyllä on 100% varma. Sain vahvistuksen toimittajilta itseltään.

E. On muuten iTitle transferin kotisivut kehittyneet/parantuneet huomattavasti. Tuo Testimonials -sivu kuitenkin paljastaa, että nämä (tai tämä yksi herra?) tekee lähinnä yksittäisen AOLn loppuasiakkalle/kuluttajalle vaihtoehtona Title insurancelle. Testimonials - iTitleTransfer

Vaikea kuvitella, että saisivat yhtä skaalautuvaa palvelua pystyyn kuin Voxtur, ainakaan tässä ajassa.

Juu. Ja tuo iTitletransfer taitaakin olla ainut muu toimija jolla on edes jonkinsuuntaista AOL:ia kuin Voxturilla, tai ainakaan en itse julkisista lähteistä löydä tietoa.

Tuon firman toimari on muuten hyvä AOL:in puolestapuhuja linkedinissä, vaikka harmillisen pieni näkyvyys:

Seuraava ostokohde ?

Maaliskuulta 2021 löytyy ylläoleva viesti tähän ketjuun. Jos oletetaan, että tästä title joint venturesta tuli ulos AOL, niin mikä on tämä large mortgage originator? ![]() F&F ei kuvaukseen istu ja jos/kun Jimin mukaan AOLn synnyttämiseen meni kolme vuotta, niin tuskin 2021 on enää mitään puhdasta title insurance juttua alettu kehittää?

F&F ei kuvaukseen istu ja jos/kun Jimin mukaan AOLn synnyttämiseen meni kolme vuotta, niin tuskin 2021 on enää mitään puhdasta title insurance juttua alettu kehittää?

Tähän oli esitetty arveluna Freedom Mortgagea joka olisi Voxturille asiakkaana/kumppanina kuin nenä päähän, mutta eipä löydy mitään tietoa/jälkiä että näin olisi.

Ei tainnut löytyä muuta kuin eXp Realty ja AnnieMac, joita ei oikein kumpaakaan voi ”major lenderiksi” helposti kuvailla ![]()