Uniperin tilinpäätös löytyy täältä:

https://ir.uniper.energy/websites/uniper/English/3000/reporting.html

Uniperin tilinpäätös löytyy täältä:

https://ir.uniper.energy/websites/uniper/English/3000/reporting.html

Jos ei halua itseään kiusata selaamalla tuota Uniperin 252 sivuista rapparia ( ![]() ), niin tästä varsin mallikkaasta esityksestä saa mielestäni jo hyvän kokonaiskuvan Uniperin kehityksestä:

), niin tästä varsin mallikkaasta esityksestä saa mielestäni jo hyvän kokonaiskuvan Uniperin kehityksestä:

Tuossa ei kuitenkaan ole kuin 36 slideä ja tärkeimmät tekijät on aika hyvin saatu myös visualisoitua. Uniper on kyllä parantanut näissä IR-presiksissä viime vuosina ![]()

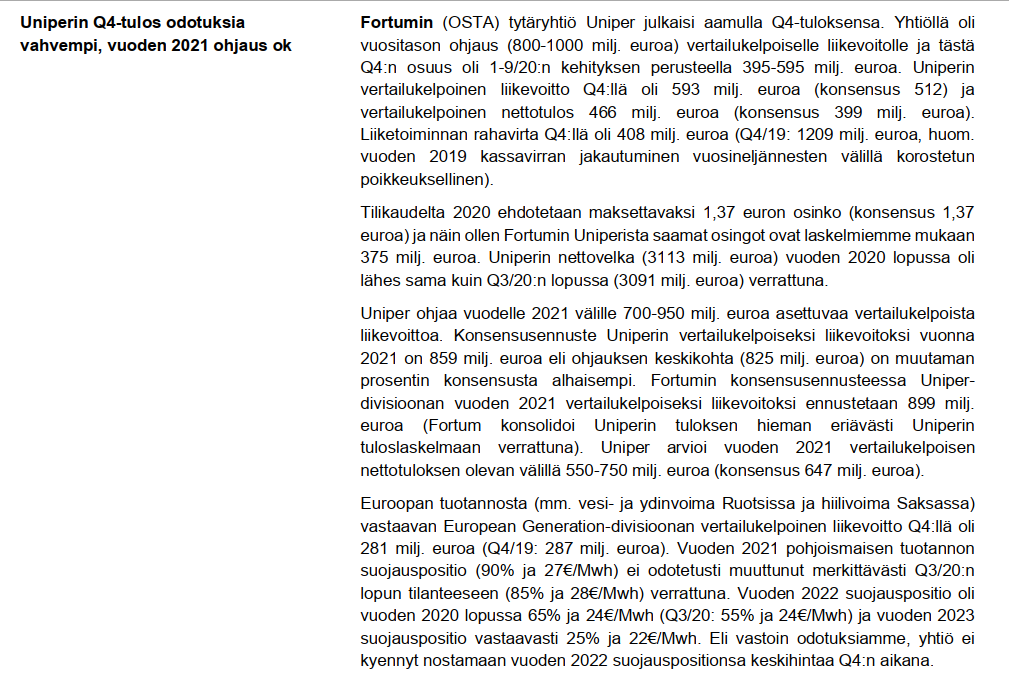

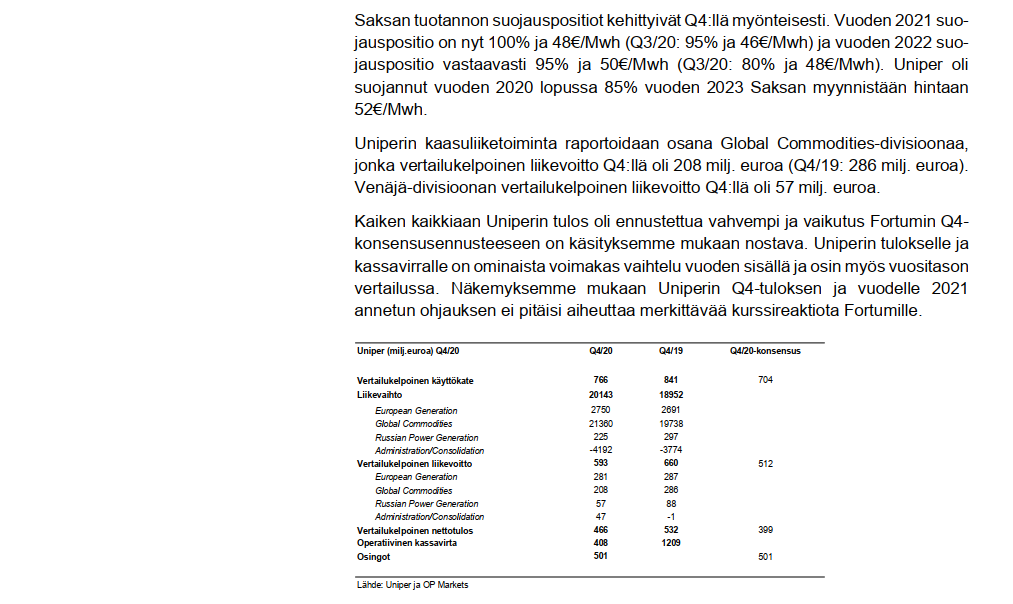

OP - Uniper Q4-tulos 4.3.2021

Uniperin CEO:n Andreas Schierenbeckin kommentteja Bloombergin haastattelussa:

Bloombergin sivuilta nähtävissä: https://www.bloomberg.com/news/videos/2021-03-04/gas-market-volatility-to-wane-in-2021-uniper-ceo-says-video

Kaasubisneksen ajurit?

Our gas business was helped at the end of the year that we got some cold period in Europe which helps us to drain our storages. Having a kind of normal winter is good for our business.

Neutraali, varovainen ohjeistus vuodelle 2021?

I think in the last year we got extraordinary volatility in the gas market. Very low gas prices and some activities which we don’t think will repeat again in 2021. That’s why we are a little bit cautious on that. Last year was very successful from our point of view. We nearly reached a billion of EBIT, our adjusted net income was up. So it was a very successful year with some extraordinary impacts. We cannot say that it will be repeated in the same way this year.

Ollaanko hyödykkeiden supersyklissä?

“I would not say that we are probably in the super cycle but we have to say that the commodity prices are pretty much depressed last year due to Covid and other impacts. And I think there is definitely some recovery needed and necessary and ongoing which is good for us.”

Huolestuttaako uusiutuvien energian tuotantolaitosten hintataso?

I think our competitive advantage is a very interesting one because we said buying these assets can be pretty expensive. But we have a lot of sites which we’re exiting due to the coal exit. We’re using these sites to develop our own renewables. We have access to the site. We have normally the permissions and place already. We have a very good grid connection, which is sometimes a big hurdle on that. And of course, We control the timeline on these developments. So we’re developing our own assets. So exiting from coal could be is considered to be creating liabilities but actually we are turning these liabilities into assets.

Uniper kommentoi myös Alankomaiden hallituksen suunnitelmia sulkea kaikki maan hiilivoimalat. Uniperin CEO:n mukaan oikeustoimet mahdollisia.

@Juha_Kinnunen kirjoitti eilen aamulla:

“Uniperin kontribuutio Fortumin Q4-liikevoittoon oli ennusteissamme aikaisemmin vain 458 MEUR, missä on ollut -25 MEUR:n oikaisu suhteessa Uniperin raportoimaan oikaistuun liikevoittoon. Konsensus oli kuitenkin korkeampi eli noin 525 MEUR. Alustavasti Uniperin liikevoittokontribuutio nousee noin 565 MEUR:n kokoluokkaan, joskin tämä riippuu tarkemmasta tuloksenmuodostumisesta. Edellä mainittu oikaisu johtuu osin erilaisista kirjanpitokäytännöistä sekä ristiinomistuksista (pääosin ydinvoimaloita Ruotsissa). Oikaisujen takia Uniperin näyttämä tulos on lähtökohtaisesti korkeampi kuin Fortumin raportoima tulos Uniper-segmentistä. Joka tapauksessa alustavien lukujen perusteella tulemme nostamaan selvästi Fortumin Q4-ennusteita.”

Tämän perusteella Fortum kirjaa Q4/2020 → n. 565 M€ oikaisun jälkeen. Melko mukava muutos Q3:seen, jossa Uniperin vaikutus oli n. -300 M€.

Venäjän tulos lienee kehno. Vuoden 2019 tilinpäätöksessä EUR/RUB oli n. 72. Viime syksystä se on ollut liki 90, joten valuuttakurssin muutos pudottaa tulosta liki neljänneksen. Ehkä tämä on vain kirjanpidollinen, kun ei niitä ruplia sieltä Venäjältä pois tarvitse rahdata ![]()

Toivotaan että tuo Venäjän liiketoimintojen myynti toteutuu tänä vuonna.

Torstaina sitten nähdään huipputulos myös Fortumilta. Tuskin vaikuttaa kuitenkaan robottien algoritmeihin juurikaan mitään.

Laskin hiukan odotettavissa olevaa vertailukelpoista käyttökatetta (EBITDA).

Q4/2020 1083 M€ (Q4/2019 552 M€)

2020 2268 M€ (2019 1764 M€)

Liiketoiminnat:

| ennuste | ennuste | ||||

|---|---|---|---|---|---|

| Q1/2020 | Q2/2020 | Q3/2020 | Q4/2020 | 2 020 | |

| Generation | 273 | 212 | 181 | 280 | 946 |

| Russia | 138 | 74 | 73 | 100 | 385 |

| City Solutions | 106 | 32 | 10 | 130 | 278 |

| Consumer Solutions | 48 | 35 | 33 | 35 | 151 |

| Uniper | 184 | -147 | 568 | 605 | |

| Other Operations | -22 | -26 | -19 | -30 | -97 |

| 1 083 | 2 268 |

Tuo tekee 2268 M€ voutin osa pois niin EPS on yli 2 €. Osinkoa voisi jopa vähän nostaa.

Ei suositus ja omistan itse jonkin verran Fortumia ![]()

Muita mukavia uutisia saattaa olla Intia aurinkovoimahankkeidin kaupan klousaaminen (500 M€), Venäjän statukseen päivitys sekä jotain infoa NS2:sta.

Uniperin toimari ei voinut olla kehaisematta kuluvaa kvartaalia eikä se näillä pakkasilla huono ole Fortumillekaan. Ehkä Q1/2021 on sitten sellainen tulos että pankkiiriliikkeet joutuvat korjailemaan noita algoritmejaan uudelle levelille.

EDIT: korjailin hiukan EPSiä, kun en ollut huomioinut veroja. Laskelmia on kyllä vaikea tehdä kun lukuja Fortumin tilinpäätöksissä riittää. Onneksi @Juha_Kinnunen tekee alkuviikosta kunnon laskelmat ![]()

Juhan Q3/2020 kommentissa Fortum Q3-pikakommentti: Pitkälti odotettu tulos, 2022 suojaukset hyvällä tasolla | Inderes: Osakeanalyysit, mallisalkku, osakevertailu & aamukatsaus on seuraava maininta:

“Sen sijaan raportoitu osakekohtainen tulos (0,23 euroa) oli meille positiivinen yllätys (ennuste 0,15 euroa). Alustavasti uskomme, että tässä merkittävä rooli on tuloksen jakautumiselle vanhan Fortumin ja Uniperin välillä. Koska Uniperin tulos oli ennakoitua enemmän tappiolla, tämä tappio jakautui myös Uniperin 25 %:n vähemmistölle.”

Löysin tämän eron tuloslaskelmasta. Jakson tulokseen summataan mystinen “hallitsematon korko”. Yleensä se on ollut summa joka vähennetään tuloksesta, mutta Q3 oli erilainen kuin edellisillä kvartaaleilla eli olikin halitsematon 60 miljuunan korkosaaminen. Ei ihme että Juhan ansiokkaat laskelmat eivät tällaista “vakiota” keksineet. Ero 15 sentin ja 23 välillä tulee juuri tuosta.

Yllä oleva on hiukan sama kun aikoinaan opiskeluissa konetekniikan maikka laski laskujaan taululle. Kun vastauksesta ei syntynyt oikealle hehtaarille olevaa vastausta, hän nykäisi jostakin oman vakion, jolla tuloksen kertoi lopuksi ![]()

Vara Research on tänään päivittänyt Fortumin ennusteitaan » Detailed Consensus (vara-services.com)

Samoilla hehtaareilla kuin omani.

Myös tavoitehintoihin on tullut päivityksiä. Inderesin arvio osuu tismalleen mediaaniin eli parikymppiä.

YES!!!, sanoo eräs Forzan omistaja. ![]()

Ja on syytäkin, koska talvi on ollut kylmä ja sähkön yksikköhinnat pilvissä eli Masselan mahtava sähkölasku on paisunut männä-talvena entisestään ![]()

Lopputulos: +/- nolla.

Masse-setä, FA, On se vaan ihmeellistä tämä massen ikuinen kiertokulku taskusta toiseen ![]()

![]()

![]()

Pieni korjaus tuohon torstaihin. 12.3. onkin perjantai ![]()

Loppujen lopuksi pitkällä tähtäimellä ihan sama tuleeko huipputulos nyt vai 5 vuoden päästä. En ole myymässä ihan lähiaikoina Fortumin nippuani.

@Juha_Kinnunen ennusteessa luvataan EPSiä vain 24 senttiä. Tämähän ei oikein kummoinen tulos ole. Jos Uniperin tuloksesta tulee 565/888 = 64 senttiä niin muu liiketoiminta tekee -40 senttiä?

Vai lasketaanko EPS Uniperin osalta vain heidän maksamista osingoistaan 500 M€, josta Fortumille tulee 350 M€. Täytyy varmaan perehtyä paremmin koko vuoden tilinpäätökseen, kun sen uunituoreena perjantaina saa kätösiin.

Pakkasiin liittyvänä pienenä huomiona, Fingrid uutisoi jokin aikaa sitten 2020 tilinpäätöstiedotteessaan alla olevan mukaisesti. Tosin tuo poikkeuksellisen lämpimä sää taitaa pääosin viitata alkuvuoteen.

Fingrid Oyj:n tilinpäätöstiedote tammi-joulukuu 2020: sää vaikutti merkittävästi tuloksen muodostumiseen

- Fingridin taloudellinen tulos 2020 oli suunniteltua huonompi, mikä johtui lähinnä poikkeuksellisen lämpimästä säästä. Operatiivisesti vuosi sujui kuitenkin suunnitelmien mukaisesti koronapandemiasta huolimatta. Kantaverkkosiirron hinnat pidettiin vuoden aikana ennallaan.

Vuosi 2020 oli Suomessa mittaushistorian lämpimin, minkä seurauksena sähkönkulutus laski edellisestä vuodesta keskimäärin kuusi prosenttia. Sää näytteli pääroolia laajemminkin pohjoismaisilla sähkömarkkinoilla. Poikkeuksellisen leuto talvi ja siitä seurannut merkittävä sähkön kulutuksen lasku, kovat sateet ja niiden myötä hyvä vesivoiman saatavuus sekä voimakkaat tuulet ja runsas tuulivoiman tuotanto aiheuttivat Pohjoismaissa erittäin alhaiset sähkön markkinahinnat ja suuret hintaerot eri alueiden välillä. Suomi toi Ruotsista sähköä hyödyntämällä maiden välisen siirtokapasiteetin täysimääräisesti, mutta siirtokapasiteettimme ei riittänyt täyttämään markkinoiden tarvetta. Rajasiirtoyhteytemme toimivat kuitenkin erittäin hyvin ja kykenimme antamaan tehokkaasti markkinoiden käyttöön olemassa olevan siirtokapasiteetin.

Tämän talven pakkaset onkin olleet 2021 puolella. Viime talvi taisi olla leuto.

No jaa, ei ainakaan Espoossa nyt mitään oikeita pakkaspäiviä ole ollut kuin ehkä 2-3 kpl, jolloin oli karvan -20 C alapuolella. Lunta on toki ollut, mutta muuten aika leuto alkuvuosi. En sitten tiedä kuinka suuri osa Fortumin tuloista tulee PK-seudun ulkopuolen tehtaista vs. kotitaloudet, joista iso osa on PK-seudulla. Muualla porukka varmaan ostaa sähkönsä enemmän muilta sähköfirmoilta.

No pakkasellahan energiakulutus on korkeampaa, Espoossa ollut ~12 pv yli -20c pakkaspäivää ja miinuksella noin 50 päivää… Viime vuoteen verrattuna varmasti noussut kulutus.

No en usko että pks tai espoo hurjasti tulosta heiluttaa… ihan vain viikinkipäällikön mielipide