Poiminta eräältä toiselta keskustelupalstalta, alkuperäinen lähde on TD WebBroker.

Hieman ainakin itselleni uutta tietoa tässä pläjäyksessä. 2 uutta (tai vanhaa?) analyytikkoseuraajaa jotka eivät näköjään Marketwatcheihin yms. poimiudu. Paradigm Capital antanut Q3 osarin jälkeen tavoitehinnaksi 1.6$

On today’s Breakouts report, there are 73 stocks on the positive breakouts list (stocks with positive price momentum), and just one stock is on the negative breakouts list (stocks with negative price momentum).

Discussed today is a stock that would have appeared on the positive breakouts list; however, its market capitalization is below the screening threshold. On Friday, the share price closed at a record high on high volume.

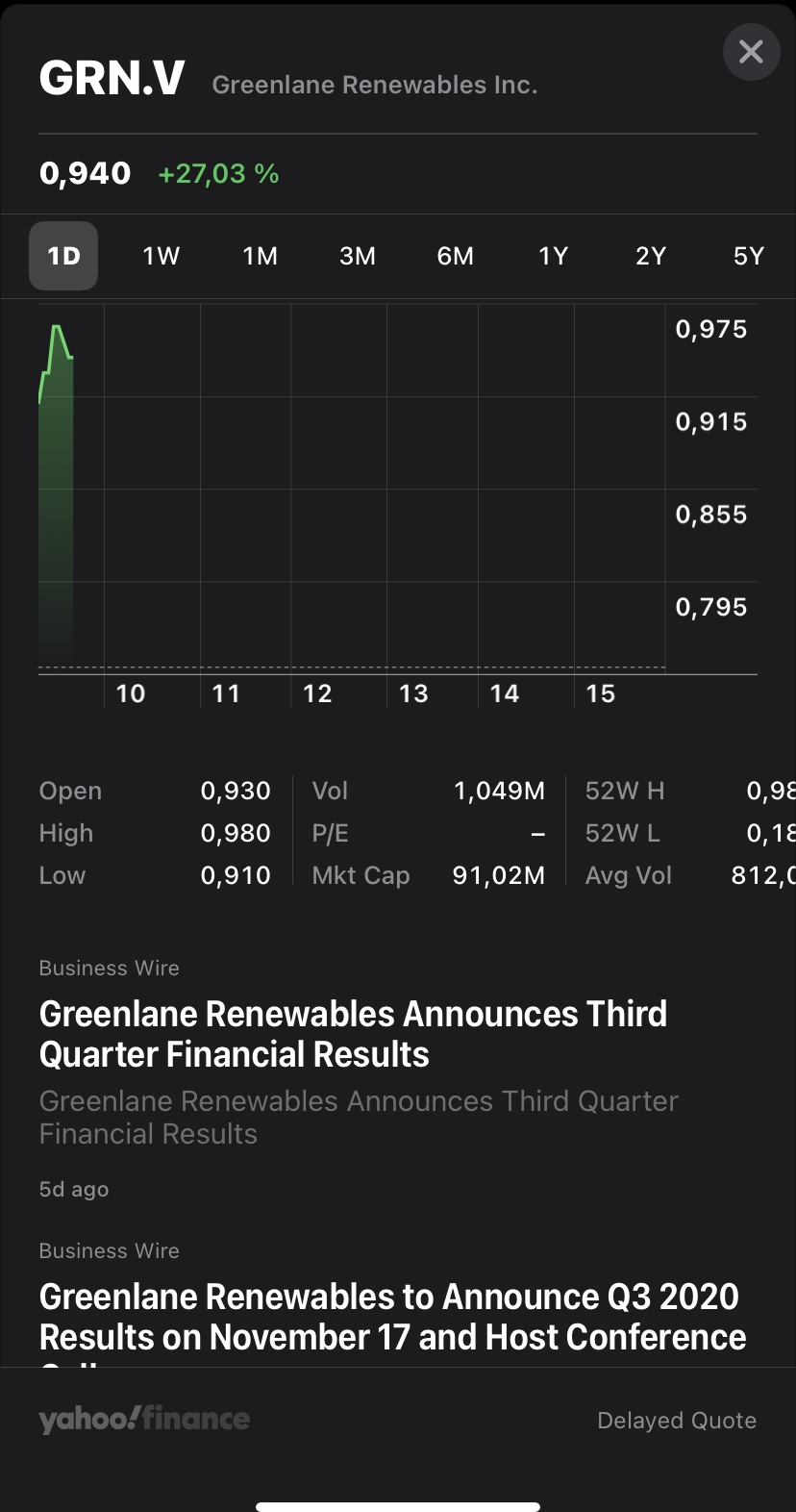

The stock has six buy recommendations and an average one-year target price that implies a 51 per cent return - on top of its 107 per cent year-to-date gain. The security discussed today is Greenland Renewables Inc. (GRN-X), which is listed on the TSX Venture Exchange.

A brief outline is provided below that may serve as a springboard for further fundamental research when conducting your own due diligence.

The company

B.C.-based Greenlane is a provider of biogas upgrading systems. Renewable natural gas (RNG) is produced through its three core technologies: water wash, pressure swing adsorption, and membrane separation. Its systems remove impurities and carbon dioxide from biogas created by organic waste at places such as landfills (methane emissions), wastewater treatment plants and farms. The RNG produced can fuel natural gas vehicles and can also be used as an alternative to conventional natural gas.

Investment thesis highlights

Climate change and greenhouse gases. There is increasing demand for clean energy and Greenlane is a pure play in the RNG market. In B.C., the CleanBC plan targets 5 per cent RNG usage by 2022 and 15 per cent by 2030. The province of Qubec targets 1 per cent RNG usage by 2020 and 5 per cent by 2025.

Robust revenue growth. A strong backlog and sales pipeline reflects continued growth potential.

Turning EBITDA positive in 2021.

Build-own-operate model presents opportunities for recurring revenue generation.

Attractive valuation. Room for multiple expansion.

Seasoned management team. The CEO Brad Douville previously worked at Westport Fuel Systems, a manufacturer of clean fuel systems.

Insider ownership. The CEO owns roughly 4 per cent of the shares outstanding. Chairman Wade Nesmith and director Deavid Demers each own approximately 3 per cent of the shares outstanding. Consequently, the interests of company leaders are aligned with the interests of its shareholders.

ESG investing is gaining momentum.

Quarterly earnings

After the market closed on Nov. 17, the company reported its third-quarter financial results. The company reported record revenue of $6.5-million, up 30 per cent year-over-year but shy of the Street’s forecast of $7.7-million. Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) came in at a loss of $0.2-million, slightly below the consensus estimate of a loss of $0.2-million. Backlog stood at $43.8-million at quarter-end. The share price rallied 2.7 per cent the next day on high volume with over 6.1-million shares traded on Nov. 18.

In the earnings release, President and Chief Executive Officer Brad Douville remarked on the company’s strong growth, “From Q1 [first quarter] 2020, our quarterly revenues have ramped sequentially on average by 50 per cent. This is consistent with the growth rate of our sales order backlog since Q3 [third quarter] of 2019. Sales order backlog growth precedes revenue growth. Our sales pipeline, which feeds our sales order backlog, currently stands at over $690 million and continues to expand year-over-year, which provides more evidence of a growing global focus on the low-carbon energy transition.”

The CEO also provided a positive outlook, saying: “Our signed agreement with the SWEN Impact Fund for Transition announced during the quarter puts Greenlane in an enviable and unique position in the European market, and we remain optimistic on a strong finish to 2020 as we started off the fourth quarter with a new repeat-customer system supply contract for a Brightmark RNG project in Florida. Chevron’s joint venture with Brightmark further demonstrates the increasing pull by the oil majors to secure attractive RNG offtake in the market including making the necessary project investments. With visibility to more than 180 project opportunities globally, proposed or proceeding, Greenlane remains well positioned to capture a growing share of the RNG value chain as a leading technology and solutions provider.”

Dividend policy

The company does not pay its shareholders a dividend. Capital is retained in order to fund future growth opportunities.

Analysts’ recommendations

There are six firms providing research coverage on this micro-cap stock, of which four analysts have “buy” recommendations, one analyst has a “strong buy” recommendation, and one analyst (Yuri Lynk at Canaccord Genuity) has a “speculative buy” recommendation.

The firms providing research coverage on Greenlane are Beacon Securities, Canaccord Genuity, Haywood Securities, Paradigm Capital, PI Financial, and Raymond James.

Revised recommendations

Earlier this month, two analysts increased their target prices:

** Paradigm Capital’s Jason Tucker to $1.60 from $1.40.*

** Canaccord Genuity’s Yuri Lynkto $1.30 from $1.20.*

Financial forecasts

The Street is forecasting revenue of $23-million in 2020, $42-million in 2021, and $49-million in 2022. The Street is anticipating the company to report an adjusted EBITDA loss of $0.7-million in 2020, and turning positive thereafter. The consensus EBITDA estimates are $3.9-million in 2021 and $5.7-million in 2022.

Revenue estimates have been relatively stable for this year but have increased for next year. To illustrate, four months ago, the Street was forecasting sales of $24-million in 2020 and $37.5-million in 2021.

Valuation

According to Bloomberg, the stock is trading at an enterprise value-to-sales multiple of 2.1 times the 2021 consensus estimate, below its peak multiple of approximately 2.5 times. The stock is trading at an EV/sales multiple of 1.8 times the 2022 consensus estimate.

The average one-year target price is $1.33, implying the stock has 51 per cent upside potential over the next 12 months. Individual target prices are as follows in numerical order: three at $1.25, two at $1.30, and $1.60 (from Jason Tucker at Paradigm Capital).

According to Refinitiv, industry peer Xebec Adsorption Inc. (XBC-X) is trading at an EV/sales multiple of 4.7 times the 2021 consensus estimate and at an EV/sales multiple of 3.5 times the 2022 consensus estimate.

Insider transactions

Looking back to the beginning of the second quarter, only one insider has reported trading activity in the public market.

On July 2, Pressure Technologies PLC sold 7,663,920 shares at a price per share of 46 cents, leaving 4,093,230 shares in this account. Prior to that, Pressure sold 2,525,610 shares at a price per share of 39 cents on June 10.

Chart watch

The stock has a brief trading history, limiting technical analysis. The initial public offering (IPO) was completed in Oct. 2018 with shares priced at 10 cents.

Year-to-date, the share price has more than doubled, increasing 107 per cent. On Nov. 20, the share price closed at a record high of 88 cents on high volume with over 6-million shares traded. This is well above the three-month historical daily average trading volume of 1.4-million shares.

In terms of key resistance and support levels, there is a major ceiling of resistance around $1. Looking at the downside, there is initial technical support around 70 cents. Failing that, there is technical support around 60 cents.