Aika neutraalin oloinen tulos mielestäni. Tulosta ilmeisesti vieläkin painaa nuo M&A kulut. Ei tämä nyt silti vaikuta erityisen kalliilta, jos uskoo noihin 40% ebitda ennusteisiin. Rahaakin hyvin palanut, joten toivoisin ettei heti tulisi lisää hankintoja ja anteja. Q4 ja Q1 pitäisi jo numeroiden parantua, saa nähdä käykö näin.

EPS jäi pakkaselle 0,11NOK, joka itselle oli hienoinen pettymys. Fokus oli kannattavuuteen, joten odottelin lähemmäs breakeven -tasoa. Joskin kertaerien ja poistojen ajoitukset vaikuttaa kvartaaleittain paljon.

Kasvu ihan ok ja odotetulla tasolla. Hieman alle 800MNOK ARR odottelin, mihin päädyttiinkin.

Isojen rahastojen ja/tai instikoiden myynnit painaa kurssia ja voi tehdä niin vielä jonkin aikaa. Ostajia ei taida olla jonoksi asti. Niiden loputtua suunta muuttunee, kun vaan kasvutarina on ennallaan. Norskien välittäjäseurantaa ei taida oikein olla saatavilla ![]()

Linkit raportteihin

Q3 raportti

Q3 Esitys:

Pitää tutkia vielä tarkemmin ajan kanssa, työt häiritsee harrastuksia ![]()

1 tykkäys

Kiitos pika-analyysista. Tosiaan viestini jälkeen katselin lisää ja lukasin tämän viestiketjun pari edellistä viestiä ja huomasin tuon Epsin jäämisen tappiolliseksi, minkä odotit kääntyneen jo plussalle. Katselin tuossa myös, että hankinnat poisotettuna asiakaspoistuma (churn) olisi sekä q3 (-16) että YTD (-55) isompi kuin asiakkaiden uushankinta (vastaavat 14 ja 46). Pitäisiköhän tuosta olla huolissaan? Kasvua siis lähinnä lisämyyntien kautta (upselling)…

2 tykkäystä

On tuo ihan oleellista tuotakin miettiä. Ei tässä ainakaan vielä voi suuremmin todeta orgaanisen kasvun olevan mitenkään erityisen kovaa, kun asiakkaita myös poistuu. Itse tosin odotankin yhtiöltä maltillista kasvua ja perus bisneksen tuottavan voittoa hyvällä marginaalilla.

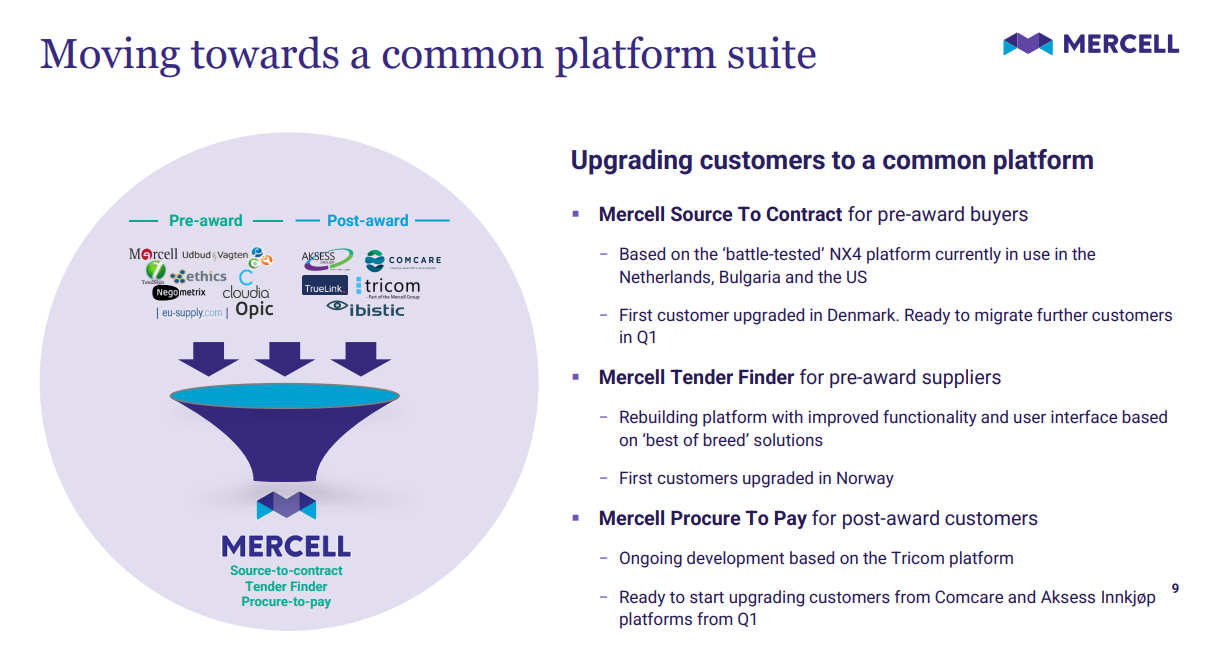

Vähän vielä kysymysmerkki miten integraatiot tulevat onnistumaan. Käsittääkseni tuossa oli tarkoitus, jossain vaiheessa tulla yhteinen platformi palveluille.

Yhtiön ohjeistus:

As described on the Capital Markets Update in May,

Mercell sees potential for 15%-20% average annual growth

in ARR from 2020 to 2025, although growth trajectory will

vary between quarters and years depending on product

launches and market introductions. The company expects

increased scale and improved efficiency from the ongoing

platform integration program to gradually strengthen the

EBITDA-margin towards the target level of 40%+

2 tykkäystä

Pitää laittaa seurantaan. Churn on kuitenkin maltillinen, mutta vaatii vastaavasti toisesta päästä putkea lisää myyntiä.

Upsell ainakin kommenttien perusteella olisi potentiaalinen eriotyisesti Supplier side -puolelta, joka ainakin tähän mennesä on puuttunut kokonaan mm. Cloudian osalta. Myös muita lisäpalveluita on kehitteillä, joilla tähän on tulossa lisäkehitystä. Asiakaskunta huomioiden kovin merkittäviä määriä uusia asiakkaita ei välttämättä ole edes odotettavissa, tarjoajien puolelle ehkä enemmänkin. Ja sitten yksityinen sektori tietysti myös ostajien puolelle on mahdollinen, mutta nykyinen asiakaskunta ostopuolella on enemmän julkiset palvelut.

Juurikin näin ja yritysostoissa sekä integraatioissa on aina riskit olemassa koko toteutuksen onnistumisen että kulujen kasvun osalta.

The many acquisitions also means that Mercell currently operates and maintains a wide range of different platforms for both buyers and suppliers in both the pre-award and post-award markets. As described in earlier reports, the company is currently investing heavily into product development to move towards a common platform suite with new products and solutions for both buyers and suppliers

2022 on tulossa siirtoa uudelle yhteiselle alustalla, jonka jälkeen ylläpitokuluissa pitäisi saada synergioista tulevaa säästöä

As we gradually upgrade our customers to these solutions and sunset our old platforms over the coming years, we expect to save additional costs such as server costs on the multiple platforms we operate today. As we transition towards a common platform, we will deliver improved solutions to our customers and do it in a more cost-efficient manner. The upgrade of the first customers has started and the solutions will be rolled-out in volume throughout 2022.

Uniikkien asiakkaiden määrä laskee Q4:n aikana, kun eri asiakastilejä yhdistetään. Laskutusmäärään ei pitäisi olla merkittävää vaikutusta

The ongoing consolidation of customer accounts will have very limited effect on the underlying value of the contracts, although the change to unique customer IDs is expected to lead to a decline in the number of registered customers of approximately 2,000 in the fourth quarter.

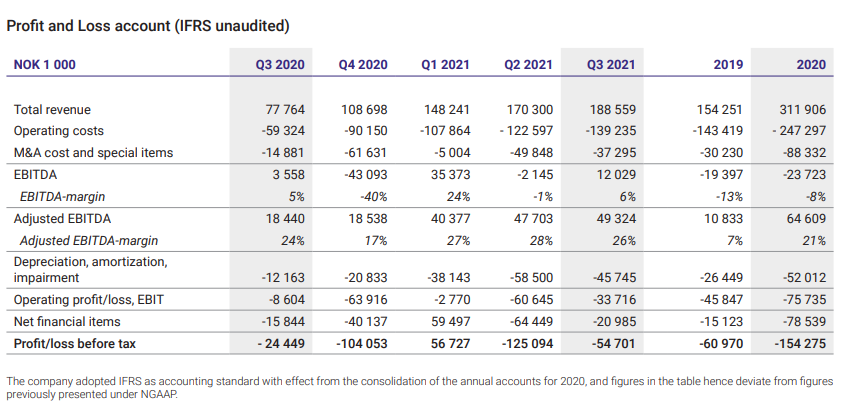

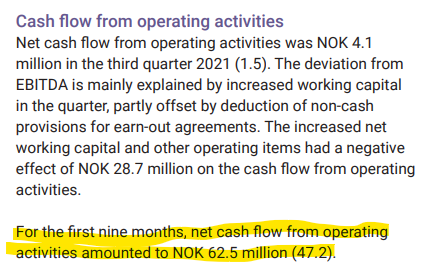

M&A ja muita poistoja, arvonalennuksia on merkittävästi. Loogista stratega huomioiden, mutta näyttää ikävältä alariveillä. Kassavirta kuitenkin selkeästi positiivinen, mikä on olennaista.

Pientä jarrua vedetään yritysostoissa, että ei osteta liian kovalla valuaatiolla ![]()

1 tykkäys

Konffapuhelun Q&A:sta poimittuna:

Cloudian supplier side on tarkoitus julkaista Q4:n loppuun mennessä. ARR lisäystä olisi siis tulossa jo Q1:n aikana

2025 mennessä Cloudian ARR pitäisi olla tuplat nykyiseen, supplier side merkittävässä osassa tältä osin.

Olisi kyllä toivottavaa, että jotain IR ja PR -tyylistä tulisi ulos myös Q-raporttien lisäksi. Nykyisellään mennään niin tutkan alla, että edistyminen menee arpomiseksi. Hyvää on sentään kvartteriraportit, jotka taitaa nykyisellään olla pakollisia listan vaihdon myötä.

Markkinakaan ei nyt täysin tyrmännyt, mikä on positiivista moniin aiempiin Q3-raportteihin nähden ![]()

1 tykkäys

Naapuripalstalta lainattuna Pareton kommentit

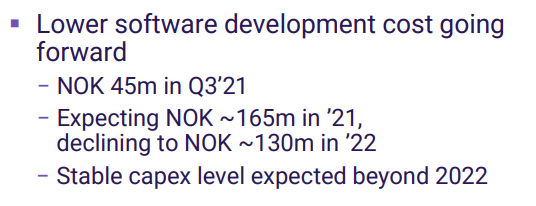

Mercell - Capex to decline going forward

Mercell reports Q3’21 ARR of NOK 792m, up 134% y/y and roughly in-line with our expectations of NOK 795m. This converts to an organic growth rate of 21% y/y, reflecting both new sales & up-sales, but including NOK 4m in negative FX movement. Reported revenues amounted to NOK 189m for the quarter (7% below PAS expectations), while adj. EBITDA ended at NOK 49m, 15% below our exp. and equal to a margin of 26%. The company reiterates its long-term target to ‘more than double ARR in existing markets organically from the end of 2020 to 2025, translating to an annual growth rate of 15-20%. In addition, Mercell states that ongoing capex cycle related to the new platform is set to decline from next year on. The company expects capitalized software costs of NOK ~165m for FY’21e and NOK ~130m for FY’22e (30% below our estimate), before stabilizing at lower levels beyond ‘22e. We expect to lower our ARR and EBITDA adj. estimate in 2021 with ~1-7%, but also lower ’22-23e capex spend with ~30%. BUY reiterated

Pareto Securities beholder TP 14.0

1 tykkäys

Disclaimer: Täysin huhutasolla, yksi lähde, johon en pääse itse enempää käsiksi.

Heitetään nyt kuitenkin ilmoille, sillä valuaatio on sillä tasolla, että ei ole mitenkään pois suljettua.

Mercell siis on mahdollinen ostokohde jopa lähiaikoina.

UNCOOKED ALERT: Mercell Holding AS said to …

Monday, 24 January 2022, 3:16 pm

Mercell Holding AS, the Norway-listed software business, is at the centre of takeover talk.People following the situation have heard Mercell Holding AS - which provides software that allows suppliers to find public sector tenders and contracts - has drawn interest from a mystery suitor interested in acquiring the business.

One person following the situation suggested the bidder for Mercell Holding AS could be a private equity firm looking to carry out a leveraged buy-out.

However, the identity of the suitor interested in Mercell Holding AS remains unclear, said people following the situation.

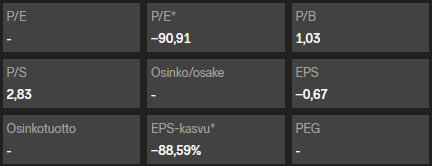

Nordnetistä lainattuna: P/S 2,83 P/B 1,03 ![]()

Positiivinen kassavirta, reipas kasvutahti, Pohjoismaissa lähes monopoli…

2 tykkäystä

Mitä odotuksia Q4 osalta?

Keskustelua yhtiöstä löytyy valitettavan huonosti, varsinkin nyt kun avanzan forumi on täysin alhaalla. Ymmärsin että tarkoituksena keskittyä edelleen kannattavuuden parantamiseen.

Oma osallistuminen tuli tähän lynchmäisesti käyttäjäkokemuksen kautta. Näppärä palvelu, joka yhdistää datan yhteen paikkaan. Mitä työntekijöiltä olen koettanut udella, niin töitä ja tekemistä riittää.

Mercell on kyllä haastava seurattava, kun uutisvirta on niin vähäinen.

Nopealla vilkaisulla omat odotukset menisi 690-710M NOK revenue, lv-kasvun pitäisi vähän tasaantua loppuvuotta kohden, jos katsoo ARR-lukua. Q3:lla oli kasassa jo 500MNOK. Loppuvuoteen voi tosin olla, että budjettiostoja on tehty ja sitä kautta nousee suhteessa enemmän. Tästä olikin jo mainintaa, Q3-raportista poimittua

![]()

ARR odotuksissa vähän yli 800M NOK, eli pientä kasvua jatkuvassa laskutuksessa ilman uusia yritysostoja.

Kannattavuuden pitäisi taas olla parantunut sekä kehityskulujen ennusteet tulla alas. Näistäkin oli jo Q3:lla mainintaa, toteumaa odotellessa.

Valuaatiohan on tullut merkittävästi alas, joten tätä saa ostella nyt tasearvostuksella P/B 1 ![]()

Nousuvaraa pitäisi olla, varsinkin jos kannattavuudessa on saatu parempia merkkejä. Yritysostojen ja integraatioiden kulut painanee vielä EPS:n miinukselle. Kassavirta pitäisi kuitenkin pysyä plussalla

2 tykkäystä

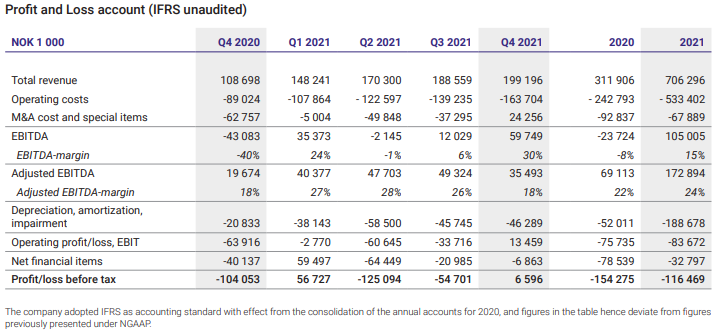

MRCEL: Mercell reports growth and margin improvement in 2021

· Continued ARR growth to NOK 793 million, +44% year-on-year with organic growth

of 18%

· Revenue +83% to NOK 199 million in Q4 and +126% to NOK 706 million in 2021

· Reported EBITDA of NOK 59.7 million in Q4 and NOK 105.0 million for 2021

· Earn-out provisions reversed after downward revision of ARR in Cloudia

· Adjusted EBITDA of NOK 35.5 million in Q4 and NOK 172.9 million for 2021

· Current focus on enabling continued strong and profitable growth in the

existing businesses

· Expecting improved EBITDA-margins in 2022, and solid free cash flow from

2022 onwards

· On track for more than doubling ARR in existing markets in 2020-2025

Oslo, February 24, 2021: Mercell Holding ASA (Mercell) reports 44% growth in

Annual Recurring Revenue (ARR) to NOK 793 million at the end of 2021, combining

18% organic growth and acquisitions.

Revenue increased by 83% to NOK 199 million in the fourth quarter. Reported

EBITDA was NOK 59.7 million, including special items with a net positive effect

of NOK 24.3 million. Adjusted EBITDA was hence NOK 35.5 million, with an

adjusted EBITDA margin of 18%.

In the current market environment Mercell is putting the M&A strategy on hold

and will rather deploy its resources to enable continued strong and profitable

growth in the existing business.

-Our focus is on profitable organic growth in our five core markets in Norway,

Sweden, Denmark, Finland, and the Netherlands. We will be working to bring both

existing and new customers onto a new and common product platform and expect

this to both save costs and generate new revenue opportunities. We see the

potential to more than double ARR in our existing businesses from 2020 to 2025,

says CEO Terje Wibe in Mercell.

Revenue for the full year 2021 more than doubled to NOK 706 million, with

reported EBITDA of NOK 105.0 million. Adjusted EBITDA was NOK 172.9 million, and

the adjusted EBITDA-margin improved from 22% in 2020 to 24% in 2021.

- We expect our existing businesses to generate continued revenue growth and

improving margins in 2022, and solid free cash flow from 2022 onwards, says CEO

Terje Wibe in Mercell.

Jutussa myös linkki raporttiin, jota ei voi jostain syystä suoraan linkata tänne:

4 tykkäystä

Presentaatio

Ja raportti

Pareton kommentit lainattu naapurifoorumilta:

Mercell just reported Q4 results, seemingly on the weak side in our view, including a NOK 20m negative ARR revision and higher than expected costs. ARR of NOK 793m is thus 20m below our estimate of NOK 813m, Q4 revenues of NOK 199m is 1% below exp. and EBITDA adj. of NOK 35m is 35% below our exp. The latter equals a margin of 18%, down from 26-28% in previous quarters, and is mainly a reflection of higher personnel and other costs. Mercell also posted a quarterly cash burn of NOK 38m, leaving the YE’21 cash position at NOK 97m. The company states, however, that it is fully funded, and that it will generate a solid positive free cash flow after investments from 2022 onwards. The share will likely trade lower today. TP under review

Tämä erityisesti hyppäsi silmille, fokus edelleen kannattavuudessa, uudet yritysostot jäädytetty

In the current market environment Mercell is putting the M&A strategy on hold and will rather deploy its resources to enable continued strong and profitable growth in the existing business.

…

We expect our existing businesses to generate continued revenue growth and improving margins in 2022, and solid free cash flow from 2022 onwards, says CEO Terje Wibe in Mercell.

2 tykkäystä

Hieman lisää omia ajatuksia, kun ehti vähän perehtymään tarkemmin. Markkina ei pitänyt luvuista, tosin tähän synkkään päivään ei varmaan mikään olisi auttanut.

EBIT kääntynyt takaisin plussalle Q4:lla.

Poikkeavista eristä plussaa, johtuen Cloudian ennustettua pienemmästä ARR:sta, josta johtuen tulossidonnaiset palkkiot kirjattu plussaksi, mutta ARR:in osalta vähennystä.

Adjusted EBITDA marginaali % putosi rankasti.

Kustannukset selvästi korkeammat johtuen nousseista palkkakustannuksista sekä loppuvuoden bonuksista.

Valuutat vaikutti negatiivisesti myös ARR-lukuihin. Ilman tätä olisikin ollut yli sen 800M NOK.

Kokonaisuutena ristiriitainen raportti, pitänee taas katsoa sitä pitkää peliä ja yrittää nähdä sinne isojen muutoksien taakse viime vuodelta. Olettaen, että tällä vuodella uudet yritysostot vedetty pois pelikirjasta, niin kannattavuuden pitäisi parantua selkeästi. Tämä on toivottu näkökulma omasta mielestä, osoittaa toiminnan kannattavuus sekä kerätä puskuria jatkoa ajatellen. Toivottavasti myös valuaation paranemisen kautta, jolloin osakkeita olisi parempi käyttää yritysostojen maksun osana. Nykyisellään tämä ei olisi edullista.

Vastaavasti pelikirja strategiavuoteen 2025 ja tavoitteen osalta ARR tuplaamiseen tulee lisää haastetta. Toteutustapoja tuohon on tietysti monia, yritysostot joka tapauksessa se pääasiallinen työkalu. Toivottavasti tämä tehdään jatkossa osakkeenomistajien etuja mukaillen, ilman ylihintaisia ostoja.

1 tykkäys

Kauhean vahva luotto ei ole kyllä johtoon, mutta aika näyttää taas mihin tässä aletaan menemään. Tuo ARR tuplaaminen kyllä kuulostaa juurikin kovalta tavoitteelta, kun nyt yritetään vielä kannattavuuden parantamiseen keskittyä. Tuokin mielestäni vähän huolestuttavaa miten iso Churni tuntuu olevan verrattuna uusiin myynteihin.

Eli liikoja en odottelisi, mutta katsotaan. Juurikin kun itsellänikin ollut käyttäjäkokemuksia vain tästä niin ehkä liian vahva bias ollut firmaan ![]() .

.

1 tykkäys

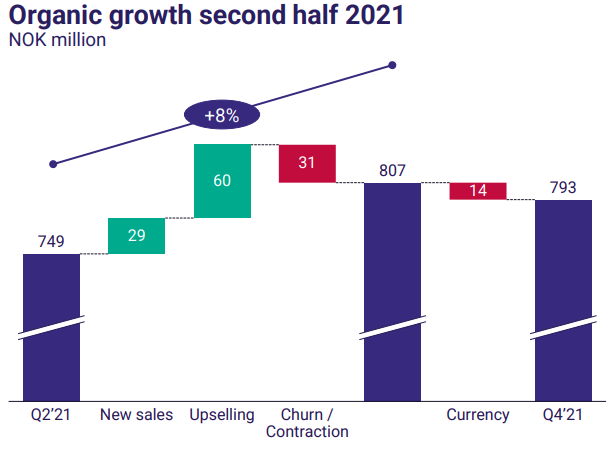

Tarkennuksena vielä, että kuvan Churn/Contraction sisältää Cloudian 2M€/20MNOK ARR vähennyksen. Mistä tämä sitten kertoo, on erittäin hyvä kysymys, johon ei ole näkyvyyttä tällä hetkellä. Siitä korjattuna churn paljon pienempi, mutta toki merkittävä.

Kokonaisuus jättää kyllä jonkin verran kysymysmerkkejä ilmaan, kuinka paljon esityksissä on mainospuhetta ja kuinka paljon todellisuuteen perustuvaa näkemystä. Joka tapauksessa kannattavuuden pitäisi parantua oleellisesti ilman uusia yritysostoja. Niiden toteuttamiseen ja integrointiin on mennyt runsaasti resursseja, joka toki on ollut tiedossa.

Tavoitteen mukainen ARR tuplaus 2025 mennessä vaatii nykyiseen verrattuna “enää” 50% lisäyksen. Yritysostoin tämä on ainoa mahdollisuus saavuttaa, mutta sitä ennen pitää kyllä nähdäkseni saada valuaatio nostettua ja se onnistuu vain kannattavan toiminnan kautta.

1 tykkäys

https://live.euronext.com/index.php/en/node/9395659

Oslo, March 22nd 2022: The Chief Financial Officer Fredrik Eeg and Chief

Commercial Officer Lars Vangen Jordet of Mercell Holding ASA will step down from

their roles in the Mercell Group. They have both contributed to positioning

Mercell as the clear market leader in the Nordics and the Netherlands, and will

now pursue other opportunities.

Effective immediately, Erik Hokholt will assume the role as interim CFO for the

Mercell Group while Werner Risberg will take on the role as interim CCO. The

Company has initiated a recruitment process to find permanent successors.

![]()

3 tykkäystä

Jatkoa tiedotteeseen, lihavoinnit omia

Oslo, March 22nd 2022: Following today’s stock exchange announcement about changes in the organisation, Mercell wishes to underline that it reiterates both its guidance for improved earnings and its expectations for a positive net cash flow after investments and debth servicing in 2022. The company also states that the company sees an improving liquidity position and reiterates that the business is fully funded.

2 tykkäystä

5MNOK kustannusleikkaukset, vuositasolla tavoite 7,5MNOK

https://newsweb.oslobors.no/message/558428

Oslo, Norway, 4 April 2022. The Board of Directors of Mercell Holding ASA has approved a cost cutting initiative designed to reduce the group’s operating costs in 2022 by approximately NOK 50 million and lower the cost base by approximately NOK 75 million on an annual basis. The company has stated that it will generate positive cash flow in 2022, and these measures will further increase the company’s cash generation.

The initiatives primarily reflect an acceleration of integration work following a string of acquisitions over the past years, seeking to eliminate redundant and overlapping job functions across the different companies within the group. The initiative will commence in April 2022, with gradual effect through 2022.

Mercell is currently focusing on delivering profitable growth by realising synergies through integration, platform consolidation and implementation of best practices. The cost cutting initiative aims to streamline company operations, and this is a natural next step in the strategy to utilise the scale benefits we have built over the last years, says CEO Terje Wibe.

The cost cuts will affect approximately 40 employees. As part of these measures, the post-award area will be reorganised to enable more efficient use of current resources across markets. Sales activities will in the short-term focus on Norway and Denmark in addition to an expansion to Sweden.

Our long-term growth strategy remains intact, although we are adjusting our cost level to strengthen our cash flow and position the company for profitable growth in line with our targets.

These initiatives add further financial flexibility and robustness to pursue our growth ambitions, says Chairman Joar Welde.

2 tykkäystä

https://newsweb.oslobors.no/message/563267

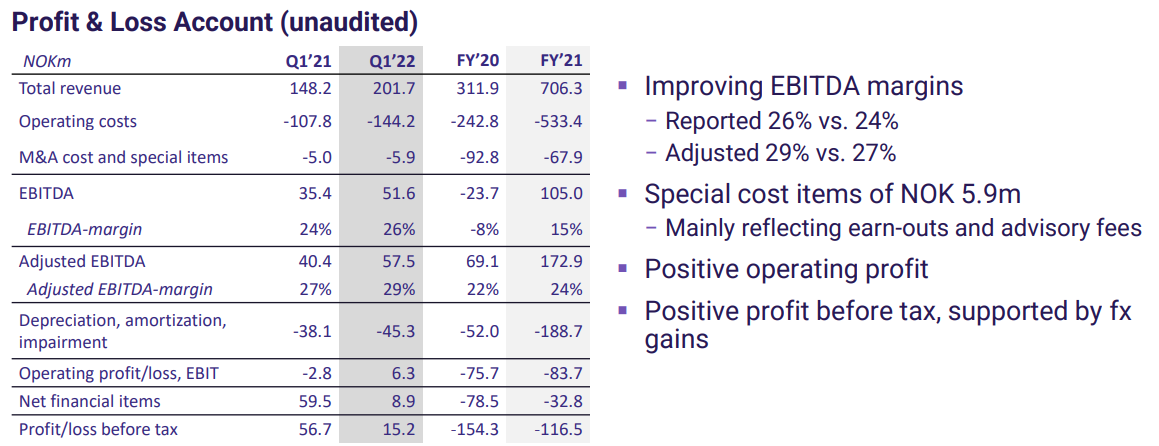

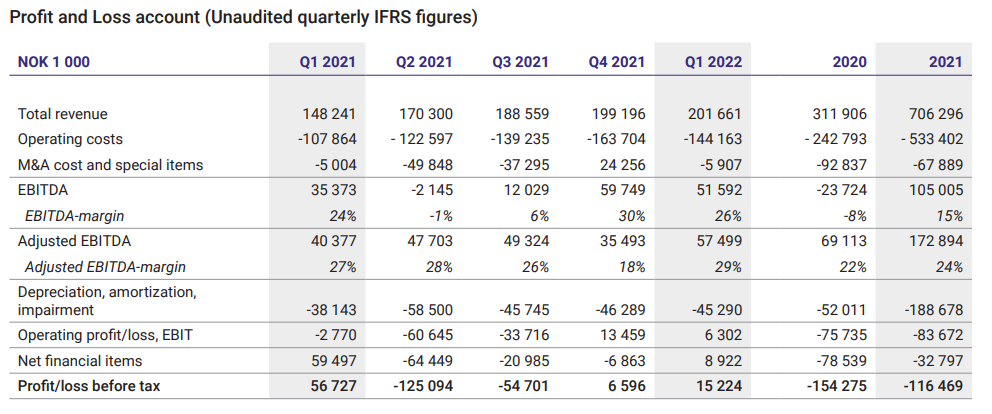

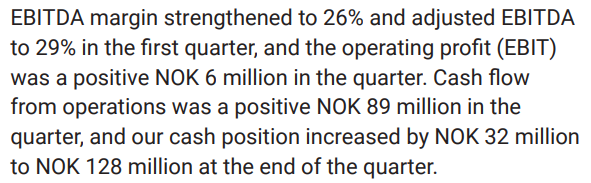

Mercell Q1 2022: Continued ARR growth and improved margins and cash flow

First quarter 2022 highlights:

• Continued ARR growth to NOK 817 million, +29% year-on-year

• Organic ARR growth of +17.5% last twelve months and +4% in Q1, in line with the target level of 15-20% annual growth

• Q1 revenue +36% to NOK 202 million

• Reported EBITDA of NOK 51.6 million with EBITDA-margin of 26%

• Adjusted EBITDA of NOK 57.5 million with adjusted EBITDA margin of 29%

• Focus remains on enabling continued strong and profitable growth in the existing businesses

• Cost efficiencies set to reduce IT spend by ~24% to NOK 170 - 185 million in 2022

• Expecting improved EBITDA-margins from 2021 to 2022, and solid free cash flow after investments and interest payments from 2022 onwards

Q1/2022

Mercell Q1 Quarterly Report 25 May 2022.pdf (1,1 Mt)

Investor Presentation

Mercell Q1 2022 Presentation 25 May.pdf (989,2 Kt)

E: lisätään vielä laajempi P&L

Vielä poiminta tälle päivälle, kassan tilanne paranee ![]()

1 tykkäys

The Board of Mercell Holding ASA unanimously recommends a contemplated voluntary cash offer from Spring Cayman Bidco, LLC to acquire all shares of Mercell Holding ASA

The Board of Mercell Holding ASA has unanimously resolved that it will recommend a contemplated voluntary cash offer from Spring Cayman Bidco, LLC to acquire all shares of Mercell Holding ASA. The Offer is a result of a strategic process conducted by the Board of Mercell Holding ASA in consultation with ABG Sundal Collier ASA and JP Morgan.

Oslo, 25 May 2022

The Board (the “Board”) of Mercell Holding ASA (“Mercell”) today announces an agreement with Spring Cayman Bidco, LLC (the “Offeror”) whereby the Offeror (through an affiliated Norwegian company to be incorporated) on certain terms and conditions will put forward a voluntary cash offer (the “Offer”) to acquire 100% of the shares of Mercell at an offer price of NOK 6.30 per share (the “Offer Price”).

The Offer Price represents a premium of:

• 110% above the Mercell shares closing price of NOK 3.005 on Oslo Børs on 24 May 2022;

• 120% above the volume weighted average price (“VWAP”) of the Mercell shares for the three-month period ending on 24 May 2022; and

• 58% above the VWAP of the Mercell shares for the six-month period ending on 24 May 2022.

https://newsweb.oslobors.no/message/563269

Huhut piti paikkansa. Kohtuullinen preemio nykyiseen, mutta menee vieläkin hieman halvalla pidemmän aikavälin näkymillä ![]()

2 tykkäystä