Enpä oo nähnyt ZIMiltä uutisia pidemmistä soppareista… Q2 konffapuhelun transcriptissä vasstailevat aiheeseen liittyviin kysymyksiin ja ilmeisesti vuosidiilit tehdään vappuun mennessä:

Yes, the contract season for us on the transpacific run from the 1st of May to the 30th of April, meaning that the discussions for the yearly contracts normally start after the conference early in the year, and the discussions are concluded around mid-April. So this is ahead of us. This is a discussion that we are going to have by and large with our customers in that we will start to initiate with our customers in six months from now. And a lot can happen in the next six months in terms of the visibility of what will be the expectation for the industry into 2022 and beyond. So obviously, we will take that into consideration when we formulate our strategy in terms of allocating spot contract

Obviously, we have negotiated and agreed with customers on the 30th of April last year, volume commitment and the space protection and it, so we deliver on that. And then on the spot market, obviously, we’ve seen the rates that are going to a very high level. But it’s a bit of the mix between contracts that we have to honor, and we do. And this is important for us because this is a long-term relationship with our customers and this is something that we do value and we make sure that we protect every single time.

Eli ZIMilläkin tosiaan on pitkiä vuosisoppareita, mutta en kyllä tiedä paljonko ja millainen se suhde niiden ja spottien välillä todella on. Tämän verran he silloin avasivat hinnoista:

In Q2, we benefited from the new annual contracts with Trans-Pacific customers, which went into effect on May 1 and reflected an average rate of slightly above 50% higher than 2020 as well as strong momentum in the spot market.

Mutta jos tuo ei viittaa spottiin, niin sitten ei ole oikein mitään mahdollisuutta arvata absoluuttilukuja oikeasti…

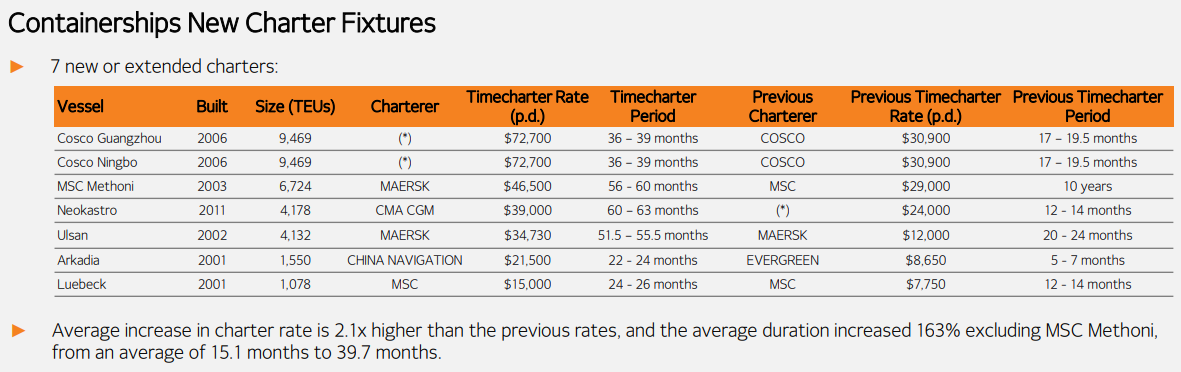

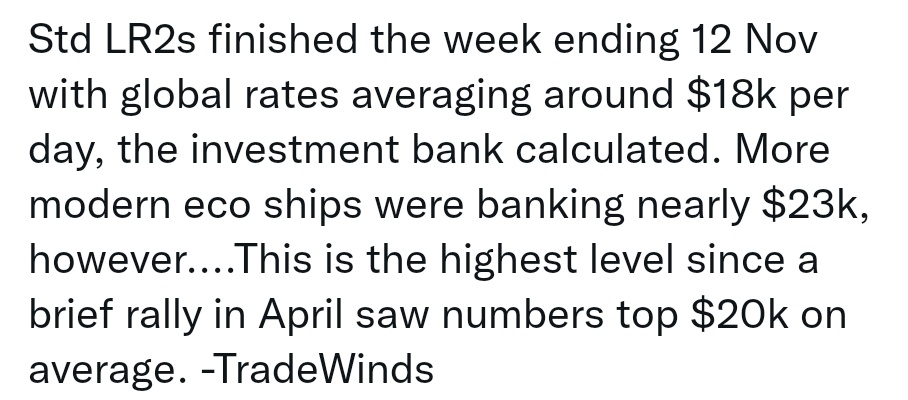

Costamarellahan oli tällainen kalvo Q2 presiksessä. Tuo toki viittaa käsittääkseni niiden laivojen päivähintoihin, enkä ole nähnyt muistaakseni missään mitään pitkää kontin hintaa tms.

Mutta kai sen pitäisi olla jossain määrin plusmiinus nolla spot- hinnan suhteen, että minkä verran niitä pitkiä diilejä on? Kysyntää ja tarjontaa häviää markkinalta saman verran kun diili tehdään? Kaikkien jäljelle jääneiden kannalta kyseessä on edelleen myyjän markkinat tällä hetkellä.

In real life tilanne toki voi olla hieman eri, kun jollain Maerskilla on varmaan ihan oikeaa hinnoitteluvoimaa kokonsa johdosta sekä spotteihin, että sen ulkopuolella. Eipä maallikko tässäkään pitkälle pääse…