Olen postannut tämän varmaan aiemminkin tänne, mutta erityisesti Qt:n kaltaisen pääomakevyen, superkannattavan, supernopeasti kasvavan firman arviointi mututuntumamultippelein on tosi vaikeaa. En välttämättä ymmärrä kaikkea tästä hyvin teknisestä tekstistä, mutta ymmärrän sen että multippeleiden juontaminen perustuu hieman monimutkaisempiin laskelmiin.

"Investors generally “value” businesses using multiples. The most common are price/earnings (P/E) and

enterprise value/earnings before interest, taxes, depreciation, and amortization (EV/EBITDA).4 Multiples are not valuation. They are a shorthand for the valuation process. Importantly, multiples obscure the value drivers that investors most care about. These include growth, return on incremental invested capital, and the discount rate. As a consequence, investors who do not think in first principles will not understand the justified changes in multiples as the result of changes in these value drivers…

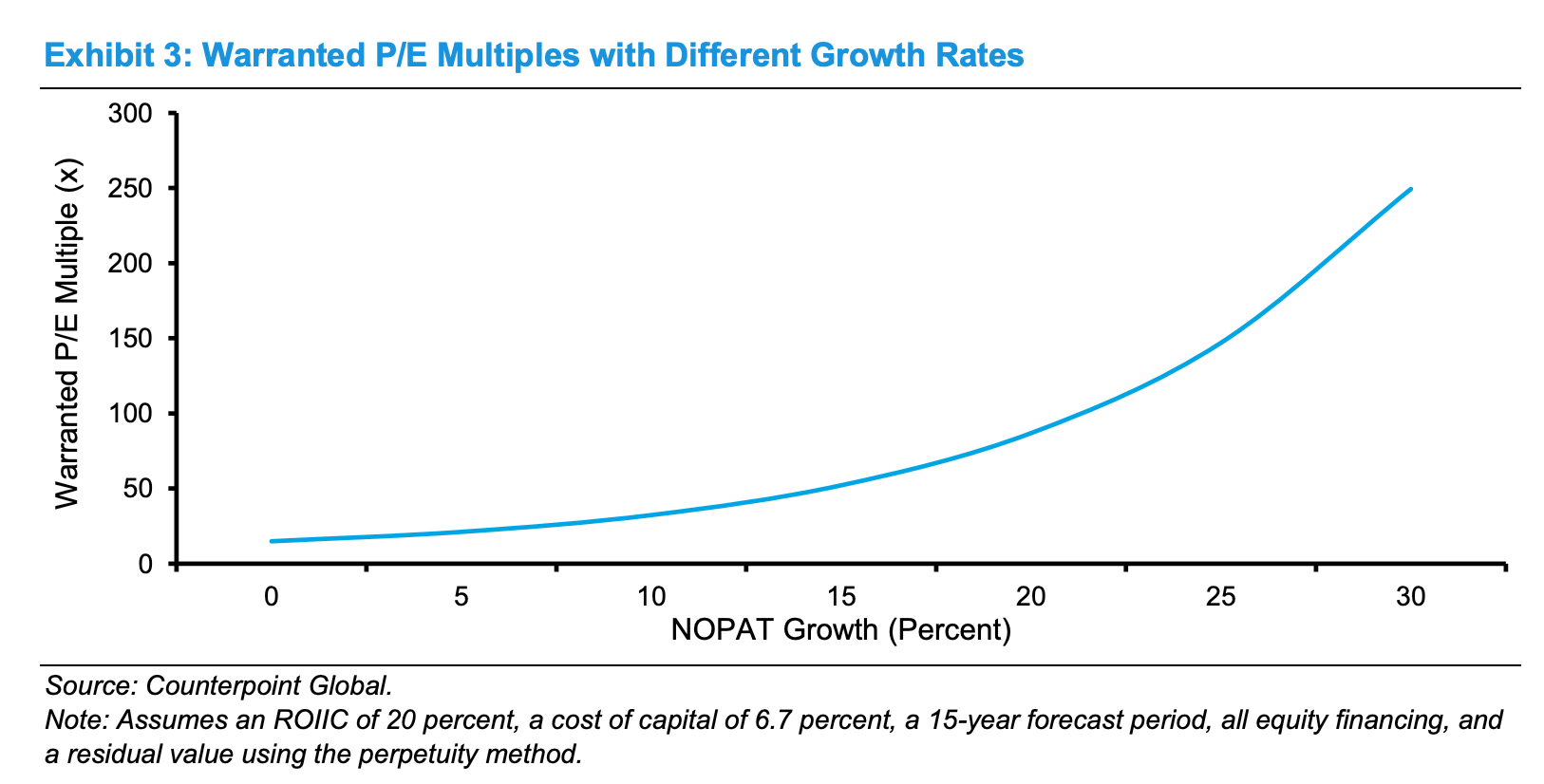

The goal of this report is to show how valuations change as we vary assumptions about growth, return on incremental invested capital, and the discount rate. We will discuss these changes in terms of P/E multiples, but a discounted cash flow model drives the calculations. We can measure the impact of various assumptions because we can control the value drivers in the model. "

Kts. esim. tämä kuvaaja missä näkyy miten P/E 250x voi olla perusteltua yhtiölle, jos tuloskasvu jatkuu 15 vuotta 30 % vauhdilla ja ROIIC (jaa a mitenhän tuo kääntyy suomeksi… Tuotto sijoitetulle kasautuvalle pääomalle. Tässä kohtaa minun taloushistorian maisterin paperit pettävät pahasti, parempi keskittyä kvalitatiivisiin tekijöihin… )

Kansankielisesti Qt:n tapauksessa joudutaan katsomaan pitkälle, pääoman tuotto on monsterimainen ja eippä nollakoroissa hirveästi rahoille ole muutakaan paikkaa mihin laittaa jolloin kieltämättä rajut arvoskertoimet ovat perusteltuja tällaisilla poikkeustapauksilla. Toisaalta pienikin muutos oletuksissa voi heiluttaa niitä kymmeniä prosentteja. QT:n tapauksessa TAM elää ja potentiaalia voi maalata monenlaiseksi kuten täälläkin on ansiokkaasti tehty, minkä takia lopputulemia voi olla älytön määrä. Aika näyttää ja nautitaan kyydistä.  Tähän asti yllätykset ovat olleet positiivisia mutta nykyhinnan perustelemiseksi joutuu katsomaan pitkälle joten eiköhän matkaan mahdu kaikenlaisia vaiheita.

Tähän asti yllätykset ovat olleet positiivisia mutta nykyhinnan perustelemiseksi joutuu katsomaan pitkälle joten eiköhän matkaan mahdu kaikenlaisia vaiheita.

Lisäys: ehkä tämä tekstin lopetus on hyvä pitää täälläkin mielessä…

"While our core hypothetical examples assumed a business with very attractive economics, it is important to bear in mind that ROIICs eventually drift lower as a consequence of factors such as competition, maturation, obsolescence, and disruption.

Bruce Greenwald uses the example of an imaginary company called Top Toaster. Top Toaster’s high initial returns gradually drop as competitors come along and drive incremental returns toward the cost of capital. Once ROIIC is equal to the cost of capital, Top Toaster will trade at the commodity multiple and an enterprise value equivalent to its invested capital. This is in the future of almost all companies. Sometimes this reality is near and sometimes it’s distant. To bring the point home, Greenwald says, “In the long run, everything is a toaster.”

Myös Qt tulee joskus olemaan “toaster”, toivottavasti ei kuitenkaan tämän vuosisadan aikana… ;D