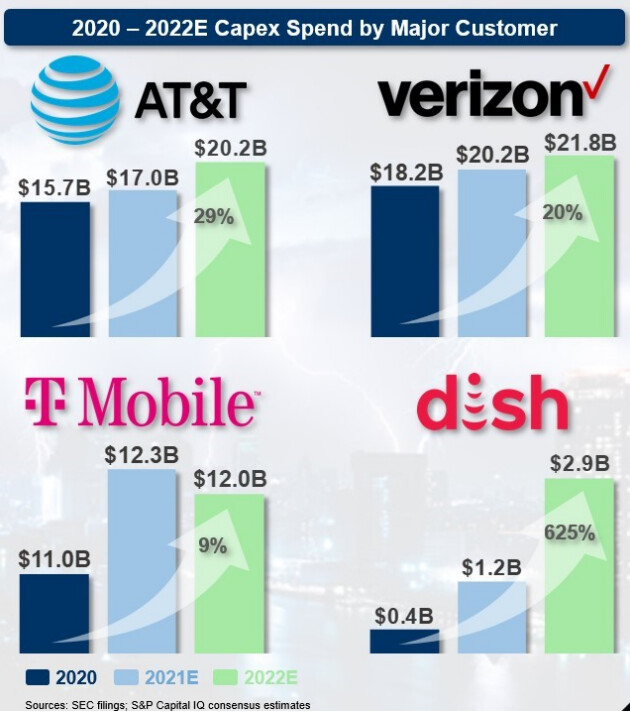

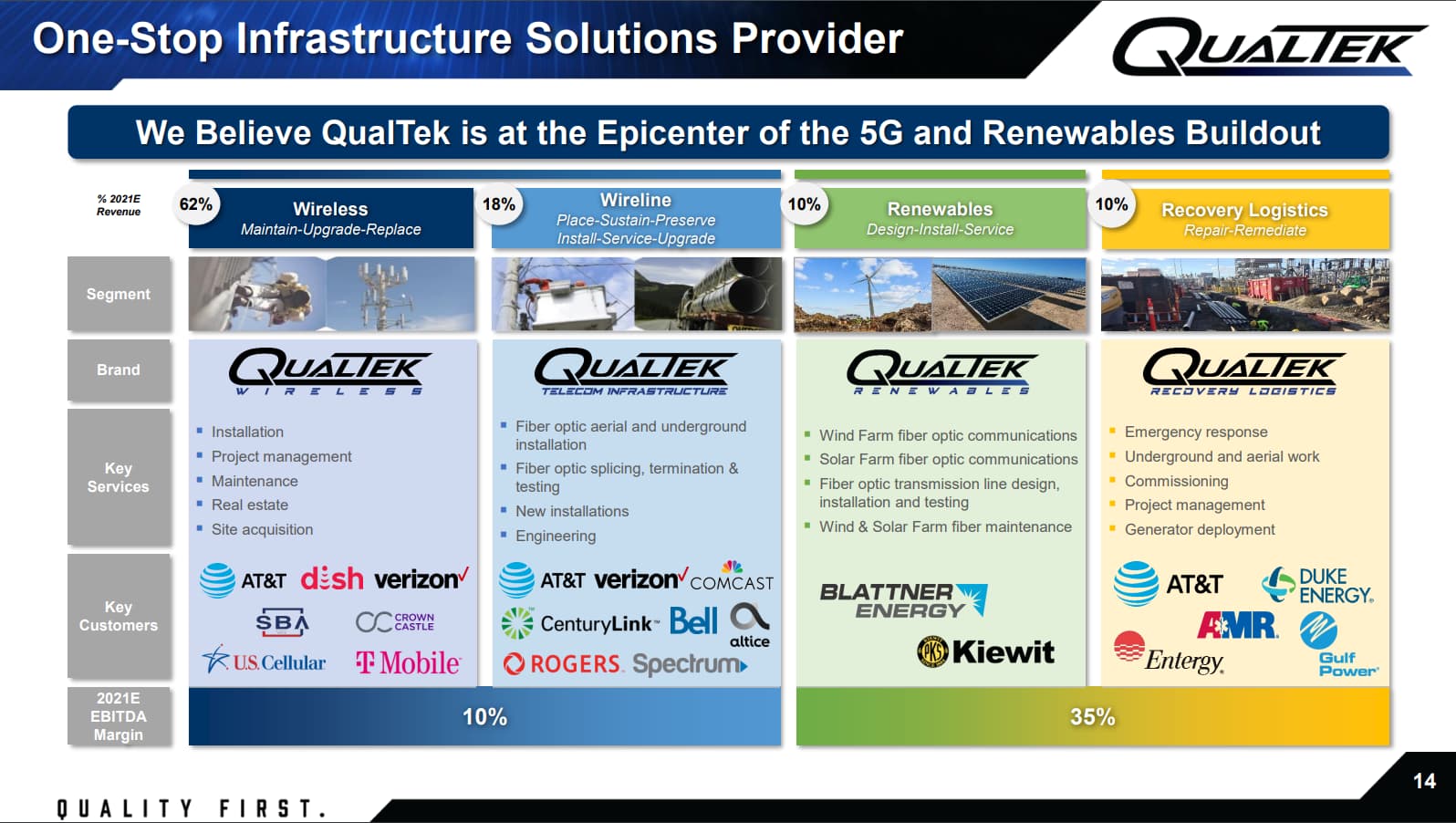

QualTek Services Inc ($QTEK) on US markkinalle fokusoitunut infran rakentaja. Kohteena erityisesti langattomat verkot, mastot, 5G tukiasemat jne. Toinen merkittävä osa on kuituverkkojen asennukset. Pienempiä, mutta nopeammin kasvavia uusiutuvan energian infran rakentaminen sekä poikkeustilojen logistiikka, uutena myös radioverkkojen konsultointi.

Taustaa

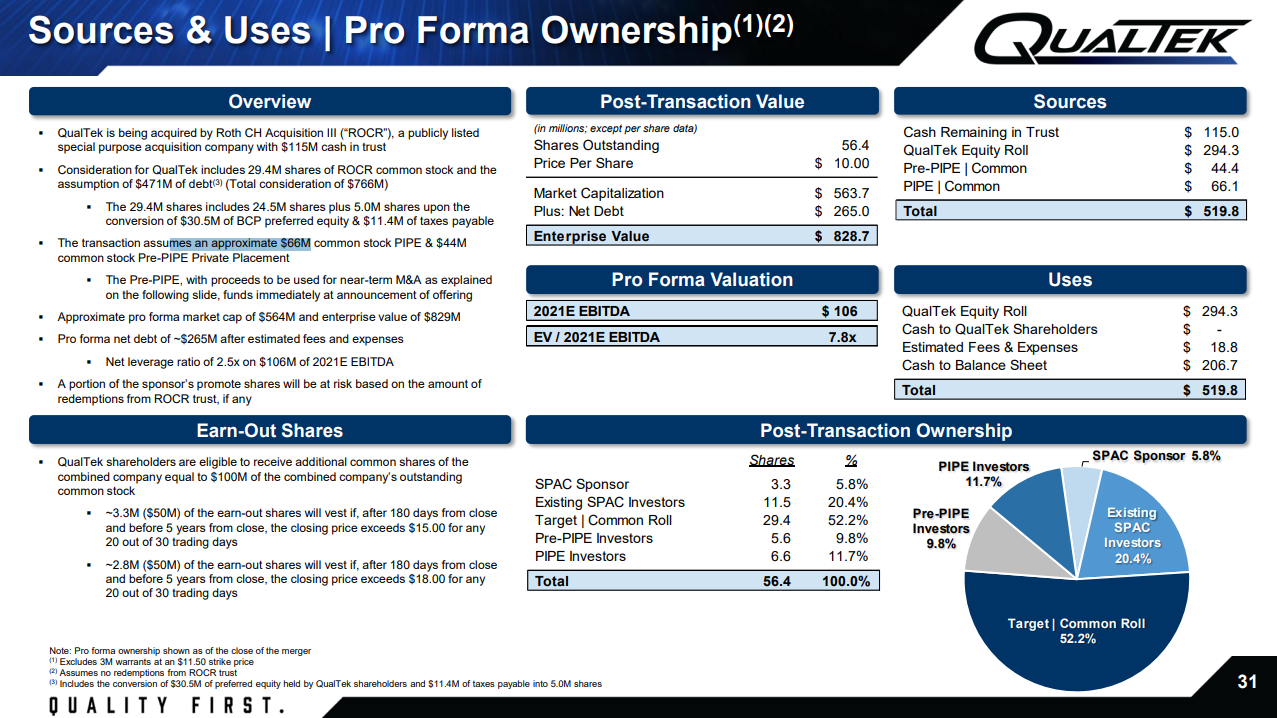

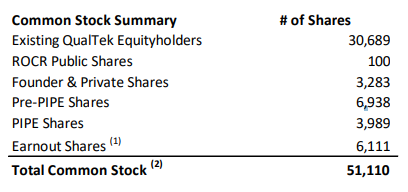

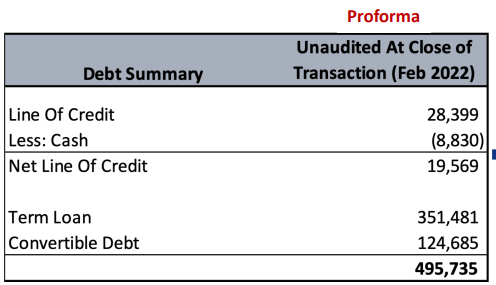

Listautuminen SPAC mergerin kautta 15.2.2022

Useita yritysostoja 2021, esim:

https://qualtekservices.com/News/1013/qualtek-expands-wireless-services-segment-with-acquisition-of-vinculums

https://qualtekservices.com/News/1014/qualtek-expands-northeast-presence-with-acquisition-of-aerial-wireless-services

https://qualtekservices.com/News/1007/qualtek-acquires-fiber-network-solutions-a-premier-provider-of-fiber-optic-and-e

Langattomat ja kuituverkot yhteensä 80% liikevaihdosta

Uusiutuvan energian rakentaminen 10% liikevaihdosta

Pelastus- ja suojalogistiikka (tms suomennos, Recovery Logistics) 10% liikevaihdosta

Lisäksi uutena SiteSafe, joka on radioverkkoihin liittyvää konsultointia:

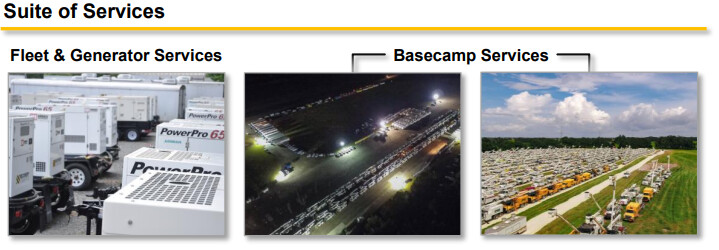

Palvelut tarkemmin kuvattuna

Sijoittajapresis 06/2021 - eli ennen yhdistymistä ja listautumista

Materiaaliin tulee suhtautua varauksella, muutoksia on tullut ja yhdistymisessä ei saatu kaikkea pääomaa. PIPE (private investment placement) ja vakuudettomat vaihtovelkakirjat kuitenkin toivat hyvän määrän pääomaa.

“2021 was a critical year for the company. We successfully closed our SPAC transaction creating over $80 million of additional liquidity to allow us to execute on our strategic growth plan.”

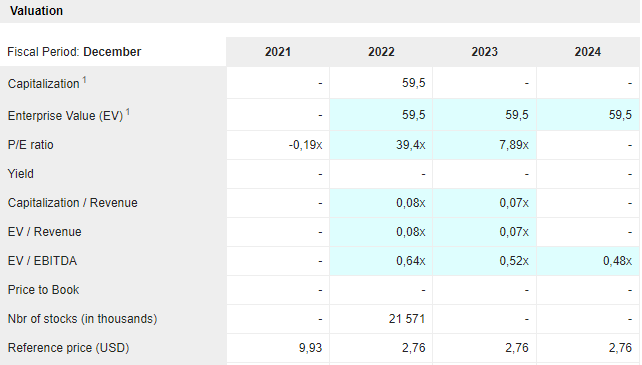

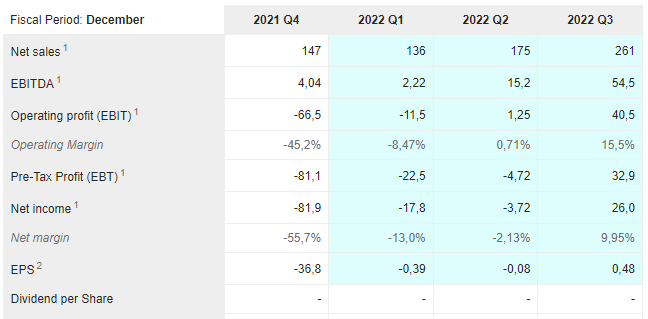

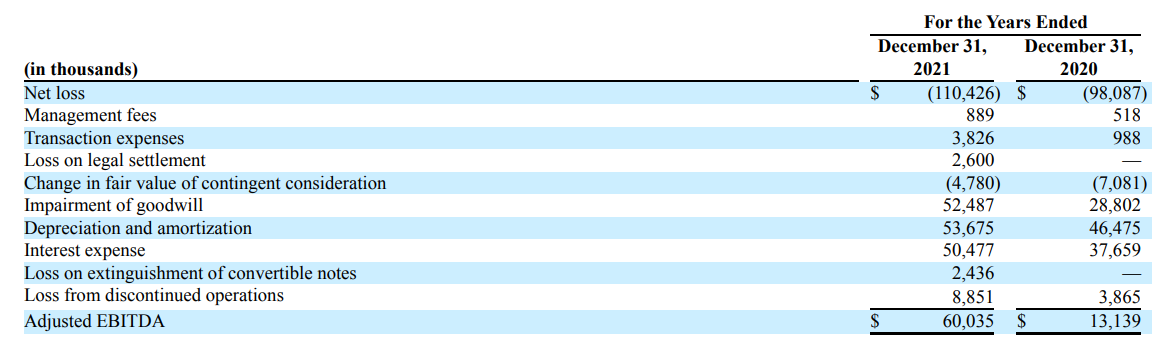

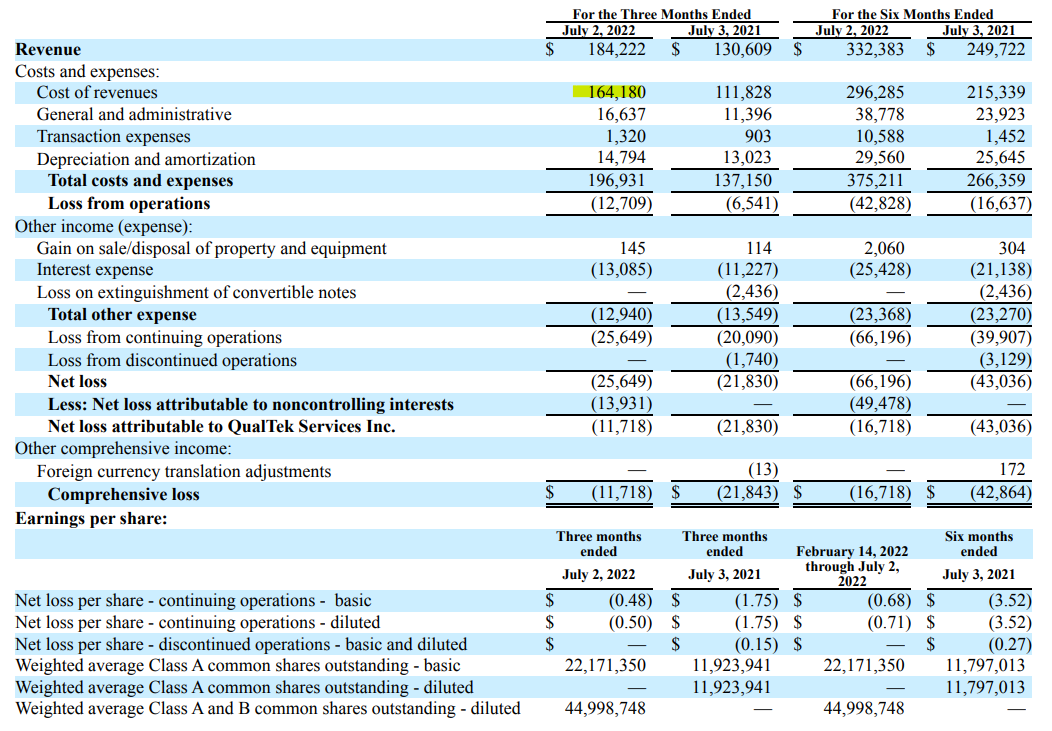

2021 ja Q4 tulokset

For the Fourth Quarter 2021:

Fourth quarter 2021 revenue was up 11.0% to $147.1 million, compared to $132.4 million for the fourth quarter of 2020. Net loss from continuing operations for the fourth quarter 2021 was $81.1 million compared to net loss from continuing operations of $56.3 million in the fourth quarter of 2020. Excluding one-time impairment of goodwill, Net loss from continuing operations for the fourth quarter 2021 was $28.6 million compared to a net loss from continuing operations of $27.5 million in the fourth quarter of 2020. Fourth quarter 2021 adjusted EBITDA was $4.0 million compared to a loss of $13.5 million for the fourth quarter of 2020. Backlog at the end of the fourth quarter was $2.1 billion which is a 22% increase over the fourth quarter 2020.

For the Full Year 2021:

Full year 2021 revenue was $612.2 million, a decline of 6.7% from $656.5 million for the full year 2020. Net loss from continuing operations for 2021 was $101.6 million compared to net loss from continuing operations of $94.2 million in 2020. Excluding one-time impairment of goodwill, Net loss from continuing operations for 2021 improved to $49.1 million compared to a net loss from continuing operations of $65.4 million in 2020. Full year 2021 adjusted EBITDA increased 356.9% to $60.0 million, compared to $13.1 million for the full year 2020. The increase in adjusted EBITDA was driven primarily by margin improvement initiatives across both the Telecom and Renewables & Recovery segments. On a pro-forma basis, assuming the recently closed acquisitions had been owned for the full year ending December 31, 2021, QualTek estimates adjusted EBITDA would be approximately 72.0 million. For the full year 2022, guidance remains unchanged.

The company is issuing fiscal year 2022 adjusted EBITDA guidance of $100-$120M

S1- filing, josta löytyy kaikki olennainen yhdistymisestä. En ole kunnolla käynyt läpi. Mukana siis ROCR eli Roth Acquisition III SPAC