Danskellakin pysyi 52 € hinta ja ostosuositus. Aamukatsauksessaan myös vähän spekuloivat Topin ostolla ja sen vaatimalla preemiolla (4-23 % vrt. Hastings arvostus).

12 tykkäystä

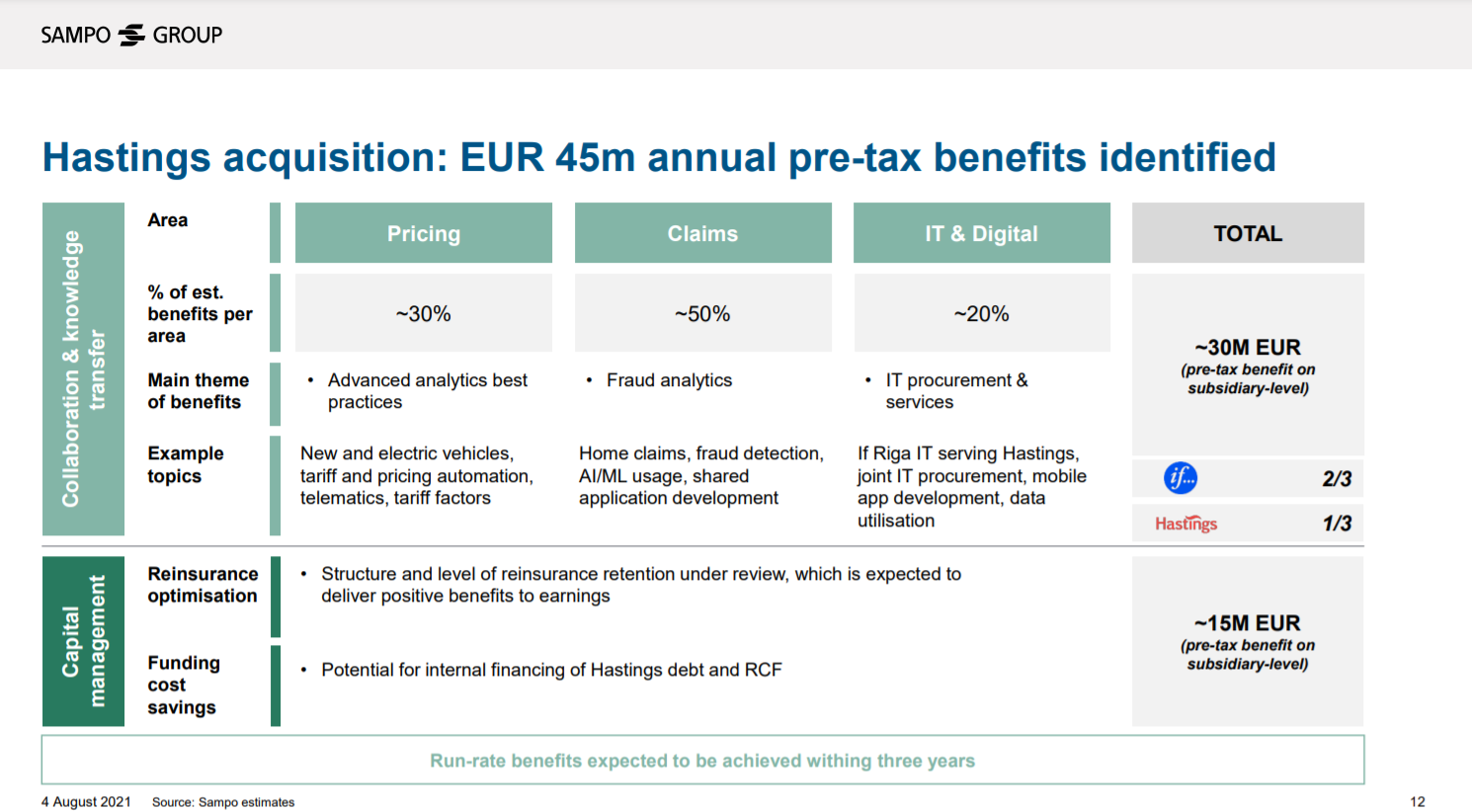

Synergiat ovat aika vähäiset kustannuspuolella.

Jos Hastings muutettaisiin IF:in haara-konttoriksi (i.e. “Branch”) pääomaa saattaisi vapautua (isompi diversifikaatio SII - IF solo) ja Hastings pystyisi vähentämään jälleenvakuuttajan osuutta (korkeampi omapääoma, korkeampi oma pidätys). Tosin Brexit tilanteessa tämä lienee haihattelua. Business puolella ilmeisesti on olemassa Know-How synergioita (i.e. myynti/hinnoittelu/vahinkojenkäsittely).

Itse omistusosuuden nosto, ei sinänsä nosta synergioita, ainoastaan avaa tuon haarakonttori vaihtoehdon.

TopDanmarkissa kustannussäästö potentiaali olisi huomattava.

9 tykkäystä

26 tykkäystä

Kyllä tämä tarkoittaa, että Sampo on tekemässä tarjousta Topdanmarkista. Joko ennen vuoden loppua tai tammikuussa 2022, jotta tarjous saadaan hallituksen hyväksyntä ennen yhtiökousta. Eli ennen ensi kesää Topdanmark on sulautunut Sampoon.

3 tykkäystä

Hastings omaa tuntuvan kasvumahdollisuuden.

Oma tulkintani on että Sampo halusi ostaa sen kokonaan itselleen, nyt kun sen sai vielä edellisesti.

2 tykkäystä

Tuossa vielä Sammon oma kuva Hastings-synergioista. Kuten @AP_1981 tuossa oivasti totesi, niin tämä ei ole mitään kulusaneerausta, vaan enemmän pehmeitä synergioita sekä tiettyjä skaalaetuja (esim. jälleenvakuuttajat).

32 tykkäystä

OP:n Saari oli eilisessä yhtiökommentissaan samoilla linjoilla, tarjous lopuista osakkeista lähtee pian kunhan vaan Nordea on taputeltu

9 tykkäystä

”Jos Sampo ei puolestaan osta Topdanmarkia, lisäosinko voisi olla jopa 7 €. Näin arvioi OP:n pääanalyytikko Antti Saari.

Isot osingot lämmittävät vain hetken. Siitä sekä @Sauli_Vilen että Saari ovat samaa mieltä. Tärkeämpää on pystyä allokoimaan pääomat tai ainakin iso osa niistä liiketoimintaan. Se nostaa vakuutustoiminnan arvoa.”

Toki Topin hankintahinnan pitää olla järkevä ja kyllä osingonsaaja itsekin kykenee allokoimaan potin tuottavaan kohteeseen. Mutta ilman Topdanmarkin hankintaa tilanne Tanskassa Sammon tuplarakentein (IF, osuus Topista) jää hankalaksi.

Siksi täältäkin ääni yritysostoon juuttien maassa👌

27 tykkäystä

Itse pitäisin sitä omistajien rahojen haaskauksena jos nollakorkoaikana Topikin ostettaisiin käteisenä (Hastings oli niin pieni että käteisosto oli perusteltu) eikä ainakin osalle ostohinnasta haettaisi uutta lainaa markkinoilta kun Sampo sitä todella halvalla saisi.

Velkaisuuskin oli jo Q3 tulosjulkistuksessa alle yhtiön omien tavoitteiden ja sen jälkeen Nordeaa on myyty taas yksi erä joka entisestään laskee velkaisuusastetta.

Voisi myös kysyä jos Topin yritysosto ei olisi sellainen toimi jolla velkaisuutta voitaisiin nostaa pitkän aikavälin tavoitteiden yli niin mikä sitten on sellainen toimi? ![]()

• Sampo-konsernin velkaisuusaste aleni 25,0 prosenttiin toisen vuosineljänneksen lopun 28,4 prosentista,osin siksi, että bruttovelka aleni 631 miljoonaa euroa velkojen erääntymisen ja velkakirjoista tehdyntakaisinostotarjouksen myötä. Sampo-konserni tavoittelee alle 30 prosentin velkaisuusastetta.

Kaikenkaikkiaan kyllä sieltä rahaa omistajille palautellaan ihan puhtaiden osinkojenkin muodossa vaikka Topi ostettaisiin ja eiköhän se pieni velkavipukin ole Turren pöydällä työkaluna mukana siinä kohtaa kun hankinnan rahoitusta suunnitellaan.

Mitä tulee jutun spekulaatioon siitä että ylimääräistä pääomaa ei jäisi omistajille ollenkaan palautettavaksi se olisi todella erikoista kun näitä Sammon pörssitiedotteita miettii. ![]()

Sammon johto aikoo ehdottaa, että myynnistä saatavat varat käytetään vähintään 2,00 euron osakekohtaisen lisäosingon jakamiseen ja 1.10.2021 käynnistetyn omien osakkeiden osto-ohjelman laajentamiseen, jotta omia osakkeita hankkimalla voidaan palauttaa enemmän ylimääräistä pääomaa.

35 tykkäystä

Miksi Sammolla on kaksi eri sarjaa tuolla Other OTC:ssa? Saxpy ja Saxpf, joista -pf on varmaankin 1:1 ja tuo -py olisi jonkinlainen puolikas osake hintoja katselemalla. Kunhan kyselen.

Sammolla ei ole omaa ADR-ohjelmaa. Nuo ovat pankkien liikkeeseenlaskemia instrumentteja (Unsponsored ADR).

16 tykkäystä

I was thinking of Sampo’s future value ex Nordea and all the PE investments.

My point of departure is to compare it with the best comparable company in the Nordics: Tryg. Sampo and Tryg are to many extent rather similair, with some exceptions that Tryg is not operative in Finland and I also do not think in the Baltics.

My thoughts are just to provide a context for a future valuation. And yes, my numbers do not transmit/convert into reality as such, but gives an estimation reference point.

Tryg’s current valuation metrics:

Forward P/E: 31.55, Book value: 2.26

Sampo’s:

Forward P/E 20.41, Book value: 1.93

Of these the forward P/E is a bit tricky to compare so I take book value.

From the above you can see that Tryg’s book value is 15% higher than Sampo’s now.

My assumption is then that Sampo (ex nordea) should be trading in line with Tryg’s book value (at least). In other words: Sampo’s book value as an insurence should be 15% higher than now.

So if we look at the current price Sampo is valued at 44 euro per share and deduct the excess cash from Nordea etc (8.5) we come to 35.5 euro. However, if we then apply Tryg book value estimation we come to ca 40.8 euro per share (for Sampo as full insurence company) (Yes part of the excess cash is going to distrubuted in dividends on which I pay taxes, but part of the excess cash has already increased the future earnings potential buy ca 5 %, read: Hastings and buybucks).

So at 44 euro per share today and with ca 8.5 euro in excess cash, Sampo is still a value play in the context of the Nordic insurence market

23 tykkäystä

Doesn’t share buybacks and dividends also reduce sampo’s book value 1:1 and yet to be sold Nordea shares by 7.83e per shares sold? So sampo’s book value per share will be also lower than 22,41 (Q3/21)?

Yea, just wanted to remind readers that the 41e (or BV atleast) estimate is quite flexible depending on how the extra capital will be allocated. But I appreciate ur comparisons to other insurers here, so keep them coming.

6 tykkäystä

Yes you are right. However, as I stated my numbers are not fully convertible as such. My point was to provide a context of reference.

Also, I am in the camp that belives that most of the excess capital from the rest of the unsold Nordea share will go towards buying rest of Topdanmark, so the value of Nordea share in the book will be “changed/transformed” to Topdanmak shares.

Edit: Topdanmarks market cap now ca 4,4 billion eur, and ca halv of that which Sampo does not own is ca 2.2 billion eur (plus then a premium on top of that)

Sampo 6.1 % share of Nordea is now worth ca 2,5 Billion euro.

Edit 2: Yes: this is all speculation, and depending on different moving parts. But the good think that many of these parts are fully controlled by Sampo’s upper management, which has so far (in my book) done a very good job in maximising shareholder return.

5 tykkäystä

You can not compare.

Tryg just acquired Royal and Sun - there are probably quite high expectations of future synergies (which are also reflected in the multiples, which also do not reflect P/E P/B of 2022, when RSA is fully consolidated).

Of course, a comparision will never be one-to-one. But I still think Tryg is the best comparision.

Sampo could very well be in the same position to Tryg after buying rest of Topdanmark, with regard to realizing the future synergies and perhaps eleveted book value numbers ![]()

Edit: perhaps someone has time and skill to do a normalized valuation over time between tryg and where any short-term valuation distortion metrics would be mitigated?

4 tykkäystä

Hallituksen jäsen ollut ostoksilla:

Nimi: Christian Clausen

Asema: Hallituksen jäsen/varajäsen

Liiketoimen luonne: HANKINTA

Liiketoimen päivämäärä: 2021-12-10

Liiketoimien yksityiskohtaiset tiedot

(1): Volyymi: 19 000 Yksikköhinta: 43,857 EUR

Eli ostoja n. 833K eurolla. Ihan merkittävä lisäys, kun aiempi omistus ollut 2779kpl (Hallituksen osakeomistus | Sampo.com)

30 tykkäystä

Nope - the point is that if you compare today´s multiples between Tryg and Sampo, you are comparing apples with oranges. One should try to compare forward p/e and p/b at best, but even here the figures do not really fit.

When it comes to Sampo post any TD acqusition, it is difficult to assess wo. knowing the price and future.

Potential TD synergies are high - but of the TD business > 50% is also life insurance…

…at least for me it is a mystery what Sampo is going to do with the life books (Mandatum, TD Liv).

I wont argue with you here. As you have a point. However, going back to my original posting my reflection was to offer an evaluation point of departure. Yes, my comparision has caveats, no question about it.

But instead of giving me stick, please feel free develop my logic and provide the next steps going forward. I already provided you with forward p/e: sampo 20.41 and Tryg 31.55. ![]()

Edit 1. Checked marketscreener for historical price to earning multiples and book values for Tryg (I am just copying these here). During this time they at least bought Alka, and perhaps splitted their share (if I remember correctly).

Tryg traded in 2018 for P/E 28, 2019: 21; 2020: 21. Book value 2018: 4.37, 2019: 4,93 and 2020 4,73.

My point: Tryg has traded on rather high multiplies even before any RSA acquisitions.

Edit 2. Regardless of my comparision shortcomings, Christian Clausen recent buy of 19000 sampo shares at these levels gives you an indication that Sampo might still hold some value, even as these levels.

8 tykkäystä

Topdanmarkin vuoden 2020 vuosiraportista https://www.topdanmark.com/binaries/content/assets/corporate/investor-rapporter-og-praesentationer/finansielle-rapporter/2020/4.-kvt/annual-report-2020.pdf löytyy Kanadalainen yksityisrahasto nimeltä Mawer Investment Management, joka omista 5,2% Topdanmarkista. Heidän kansainvälisen rahaston Top 25 listalta löytyy Sampo painoarvolla 1,9, mutta ei mainintaa Topdanmarkista https://www.mawer.com/assets/Fund-PDFs/3Q21-Mawer-International-Equity-Fund-Series-A.pdf Tämä luulisi olevan Sammolle helppo lisäys kohti kokonaan omistamista. Kuka tietää, vaikka juuri Sammon omat osakeostot olisi hyvä vaihtoväline tässä transaktiossa.

3 tykkäystä