Oyj:n jakama osinko toiselle Oyj:lle on verovapaata tuloa. Tuo 10% koskee ainoastaan jos Oyj maksaa osinkoa Oy:lle.

Tosiaan Nordean osakkeet olleet Sammon käyttöomaisuutta ja luovutuksen verovapaus perustuu EVL 6b§.

Oyj:n jakama osinko toiselle Oyj:lle on verovapaata tuloa. Tuo 10% koskee ainoastaan jos Oyj maksaa osinkoa Oy:lle.

Tosiaan Nordean osakkeet olleet Sammon käyttöomaisuutta ja luovutuksen verovapaus perustuu EVL 6b§.

Kappas niin olikin, että listayhtiöiden välillä tämä oli verovapaata - hyvä näin.

Tilanne päivitys:

Tähän mennessä on siis ollut ostopäiviä: 79 kpl

Yhteensä ostettu: 11268905 kpl

Ostettujen määrä kaikista osakkeista: ~2,029 %

josta saadaan keskiarvona: 142644 kpl / päivä

ja prosentteina per päivä (per 750milj.) : 0,843 %

ja prosentteina nyt hankittu (per 750milj.) : 66,60 %

Yhteensä käytetty : ~499,5 Milj. €

Keskihinnan ollessa nyt noin: 44,324€

Muutamana viime päivinä on hankittu enemmän kuin 1,1% hankittavasta määrästä versus normaalin 0,8xx% sijaan on selvää että perälauta lähenee nopeammin ja jos vielä se osinkokiima pääsisi iskemään, niin silloin nopeutuu entisestään. Nyt siis näyttää vahvasti siltä, että omien ostot saatetaan saada päätökseen @Aatu mainitsemassa ajassa 21.3. (Juuri nyt laskennallinen 23. tai 24.3.) Mukavasti on viime päivinä keskihinta pudonnut, eikä haittaisi vaikka alehinnat pitäisivät ostojen loppuun ![]()

A new speculative exercise with regard to Sampo buying the rest of Topdanmark.

The idea is to challange the view that buying Topdanmark is expensive at these levels.

I will use the same principle Sampo used when it bought Hastings.

My math is a bit off (and input from others are welcomed). My aim is to provide general numbers not exact to showcase my point.

–

Sampo started buying Topdanmark in 2008. The share was trading around 60 - 70 dkk. Sampo acquired ca 10 - 15% ownership.

In 2011 Sampo increased its ownership to 20 - 25% of Top. The share was around 70 - 90 dkk.

First conclusion:

Sampo first 25% of Topdanmark was acquired at levels below 90 dkk.

–

In 2013 Sampo increased again to 25 - 33 % ownership of Top. The share was trading at levels around 13 - 150.

In 2016 Sampo increased its ownership to the final 46.6 %. Share between that time 160 - 180 plus.

Assumption:

Sampo has on a general basis acquired its share based on the basic and general logic of first 25% at 90 dkk and the rest ca 20 % at 180 (yes these are not correct numbers, but that is not the point here, my point is to show some rough estimates).

So 90 plus 180 is 270 and that would give an average of ca 135 dkk is what Sampo has bought its current 46.6 %. (again rough numbers).

So lets assume that the rest of Topdanmark what Sampo does not own is acquired for 30% premium of today’s numbers. It trades around 370 now which would make a premium of ca 480 dkk per share.

So then a basic and rough calculation: 135 (avr so far price paid) + 480 (price for rest) is 616 dkk divided by 2 (again general numbers): give an average of ca 308 dkk.

To sum up

So Sampo could get complete ownership of Topdanmark for little over 300 dkk. I would argue that this not exactly expensive assuming that Top is able to generate ca 20 dkk eps per year (that is what marketscreener had as an estimate).

These numbers could be translated to that Sampo buys Topdanmark at levels of 15 price to earning. Currently all are Nordic peers trade around p/e 20.

Again this is all speculative, but I am using the same logic Sampo applied to buy Hastings.

My point is that to show that buying the rest of Topdanmark at a premium is not necessarily that expensive from this ‘speculative’ exersice (which has some flaws and is not exactly precise).

Ehkä tuohon laskelmaan voisi lisätä saadut osingot? Voiko niiden ajatella maksaneen osittain takaisin jo tehtyjä hankintoja ja siten alentaa tehtyä investointia? Voisiko tuosta tulla liki 10v ajalta jonkinlaista merkittävää suuruusluokkaa oleva summa?

Hmm, I would not calculate it that way. What valuation Sampo pays for rest of Topdanmark needs to be considered based on the individual valuation of that part only, not considering what they paid for the first part.

Looking from opportunity cost perspective:

So the investment of xx€ is the same in both cases, difference is the return that shareholders get for spending that money on Topdanmark or something else.

What has already been paid for Topdanmark earlier has been spent, and the return on that investment is already included as part of Sampo’s value, so in a sense it would be “double counting” from ROI perspective to use that old value to justify new investment.

Yes, you have a logical point. And a fair one also.

But, the logic I applied is the one Sampo used to defend is rationale when they bought the rest of Hastings. Some market actors also criticized Sampos logic.

I would defend the logic I used and which Sampo used is to ‘contextualize’ the optimal way of using the proceedings from the sell of Nordea shares.

My logic builds on the idea of buying rest of Topdanmark will never get cheap and Sampo will not have this opportunity again (excess of extra money). Buying at a later stage with debt financing is not optimal. Compare this with Tryg and all the associted costs of buying RSA operations with diluation of own shares and other financing costs.

And given how the Nordic insurence market works (see my earlier post) Sampo will need to buy Topdanmark to stay competitive in Denmark. And to realize synergy potentials.

Yes you are right in the sense that you could probably get better ROI elsewhere.

But for example any M&A moves in the Nordics (except Top) is out of question (regulation). And any M&A in UK involves in my view a higher risk than buying Topdanmark at a premium.

But again this is just my 2 cents ![]()

To be clear, I actually agree that buying Topdanmark has a clear logic and may in any case be very good use of capital on hand. So don’t want to judge the logic of that as such, as there are people who are much better equipped than me to estimate the value of such a deal.

Only wanted to point out that this would need to be considered as a separate capital allocation decision that needs to make sense in itself and in comparison to other uses today.

When I saw the Hastings deal and argumentation behind it I also thought that you could use the same logic to justify the high price without “eating your words” (Sampo has stated many times that the current price is too high).

However I completely agree with @jangsteri_vain that from shareholders’ perspective this is pure sleight of hand and you obviously should not include sunken costs for future ROI calculations.

I also agree with @916 that Sampo is between the rock and the hard place and the possibility to buy it cheap is close to zero. There are major synergies on the table and the risk of If losing competitivness in Denmark is real.

When you think of this, the whole situation is somewhat weird. Most of the market players would actually like Sampo to acquire Top regarding the price due to the operational synergies and Sampo’s excess capital. Sampo also would like to buy, but they are chasing the valuation which not achievable and have put themselves in very difficult situation communicationwise ![]()

To conclude on my part on this topic:

Sampo has really ‘shot themselves in the foot here’ (bad analogy, but you get my point).

A personal example:

Even this week I have added to my wife’s stock account Topdanmark shares several times (around 365-366). Note: she has owned Topdanmark shares since 2016 and has an average ca 300 now. So basically I am averaging up.

Why?

Well I view owning Topdanmark is a rather low risk investment for her long-term and her rather low cost average. Its not too volatile and the risk downside is limited (due to Sampos interest in the company). And there is a potential bonus waiting ![]()

So why have money in the account when she can own Topdanmark and collect annual dividends from the share? Even after this year the expectations is that Topdanmark will almost pay out 100% of their EPS. Estimates are round 20 dkk per share going forward. That is around 6.7% dividend on 300 based average. Much better than having money in the account which is subject to inflation. So if Sampo does not buy, she will collect rather high dividend every year for sitting on the shares.

My point: I/we am not the only one acting like this. Which implies why the Topdanmark share wont ever get cheap again. This will eventually force Sampos hand to act.

pari lisähuomiota:

-Magnunsoni aina sanoo ostoargumentteihin, että liian kallis ja myös johto on osakkenomistajia, mutta tämä nyt on vaan puhetta, että saisi hintaa alas. lisäksi sampohan on myös kallis ja silti ostetaan omia osakkeita. ristiriita on ilmeinen, koska synenergiat olisivat topissa.

-sampo haluaa vain vahinkopuolen topissa. onko sampolaiset tosiaan niin munkkeja topin hallituksessa, että katsovat vain topin etuja. itse uskon, että life saa mennä, mutta topin hintahan saattaa silloin vielä suhteessa nousta. ehkä toppi kannattaisi ostaa ja myydä top-life itse pois?

Aiemmin Sampo on myynyt Nordeaa heti kun on ollut tilaisuus. Nyt ei. Odottavatko hinnan nousua ehkä vai säätävätkö koko loppumäärästä isoa möykkyä ostajan kanssa. Vai antavatko ehkä yllätys-vaihdossa Topin omistajille Nordean osakkeita ja hieman käteistä Topin osakkeita vastaan ![]()

Osakkuusyhtiön (Nordea) tuloskommentit:

Varmaankin vaikutusta tällä Nordean tulosjulkistuksen ajankohdalla, eli odottavat nousua. Oma veikkaus että lähipäivinä kuullaan uutisia myynneistä

Sisäpiirisäännösten perusteella Sampo ei ole kaiketi edes voinut myydä ennen Nordean tulosjulkistusta. Eli nyt on hyvä paikka odottaa myyntien tapahtuvan.

Keskiviikkona Sampo julkaisee Q4-tuloksensa, sitä odotellessa kannattaa lukea alla oleva juttu. ![]()

"Operatiivisesti raportti tuskin tarjoilee suurempia yllätyksiä ja iltapäivän konferenssipuhelu tuleekin todennäköisesti pyörimään pitkälti Nordeasta saatavien pääomien käytössä sekä koroista. Sampo-liveä voi tuttuun tyyliin seurata InderesTV:ssä 09.20 alkaen."

Tässä linkki Sampo-tulosliveen inderes.fi:n puolella. Ajastan myöhemmin itse tubeliven.

Täällä on vähän pohdittu että miksei Sampo ole myynyt Nordeaa heti rajoitusten jälkeen. Käsittääkseni Sampo ei olisi voinut myydä Nordean hiljaisella jaksolla, koska tj istuu hallituksessa. Lisäksi en olisi 100% varma että Nordealla olisi kaupankäynti-ikkuna auki tälläkään hetkellä, koska CMD ensi torstaina (17.2). Vaikka uudet tavoitteet annettiinkin ulos jo tuloksen yhteydessä, niin on hyvin mahdollista että Nordealla olisi päällä vielä ns. suljettu jakso mikä estää sisäpiirin kaupankäynnin.

Uskon että Sampo tulee painamaan myyntinappia heti kun se on mahdollista ja ensimmäinen erä Nordeaa lähtee pihalle jo Q1 aikana. On toki mahdollista, että Sampo odottaisi maaliskuun yhtiökokouksen ja sen jälkeisen osingon irtoamisen, mutta en usko tämän olevan ohjaavana tekijänä.

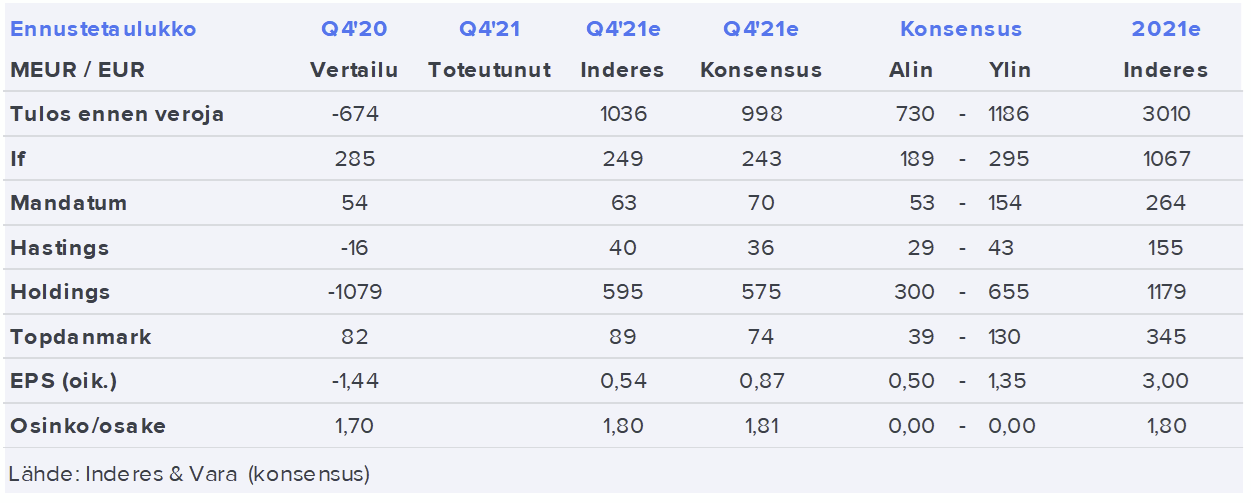

Yksi tyhmä kysymys: Inderes ennusteessa “1036 milj eur voitto ennen veroja, konsensus 998”. Sitten tuolla

lukee että 2021e group PBT (profit before taxes) 2973 … ilmeisesti miljoonaa euroa, yksikköä ei näy kyllä missään.

Miten tämä pitäisi ajatella niin että numerot täsmää?