For example: competitive landscape; Sampo has two separate organisations in Denmark, partly competing with each other whilst others competitors are streamlining their operations. This is not sustainable for Sampo and If in Denmark. Time is not on their side. For example even small time operators in Denmark has gotten their house in order now, not only the big players.

In addition: current Topdanmark shareholders hold the upper hand. Not Sampo.

Sampo is backed into a corner.

Most Topdanmark shareholders are institutional shareholders and the small time shareholders including me have sat on our shares for many years.

And I we will continue to sit on in them in future as well. Because of Topdanmarks high dividend pay out year after year. And Sampo needs these dividends more than I do to support future dividend payouts. Because Sampo cannot loose face one more time with regard to the dividend (read Stadigh mess up some years ago).

And as an Topdanmark owner I am not in a hurry to buy or own Sampo shares (I do own both). Why would I? The upside is bigger in Top than in Sampo at the moment, and the downside is limited in Topdanmark

Oletan, että ymmärrät suomea ja vastaan nopeasti suomeksi. Sammon päätöksiä vastaan on tällä hetkellä Topdanmarkissa erittäin vaikea taistella, koska se vaatii lähes kaikkien pienempienkin sijoittajien tuen. Sampo saa taas aina kaikki äänensä kokouksiin.

Arvostan silti mielipidettäsi ja en voi oikeastaan väittää ettei asia olisi näin, se on ollut vuosia näin. Minusta kaikeasta huolimatta Sampo on mielestäni vuosi pakittanut sieltä nurkasta ja on jo nyt lähes keskellä huonetta enää alle 4% päässä keskustasta. Sammon omistusosuus on hiljalleen noussut jo vuosia ja tänään saimme tietää noussut edelleen.

And I think everyone who ownes Topdanmark is fully aware of Sampo position and strenght in the company. And most are actually looking forward to that Sampo takes full controll and buys the company.

I also like to think that Sampo will not be hostile in getting the rest of the shares, because then there would be a mutiny among Top shareholders where everyone would loose.

But for them to buy the rest of company, if they dont want to buy blockshare during the next years or decade, they need to show some

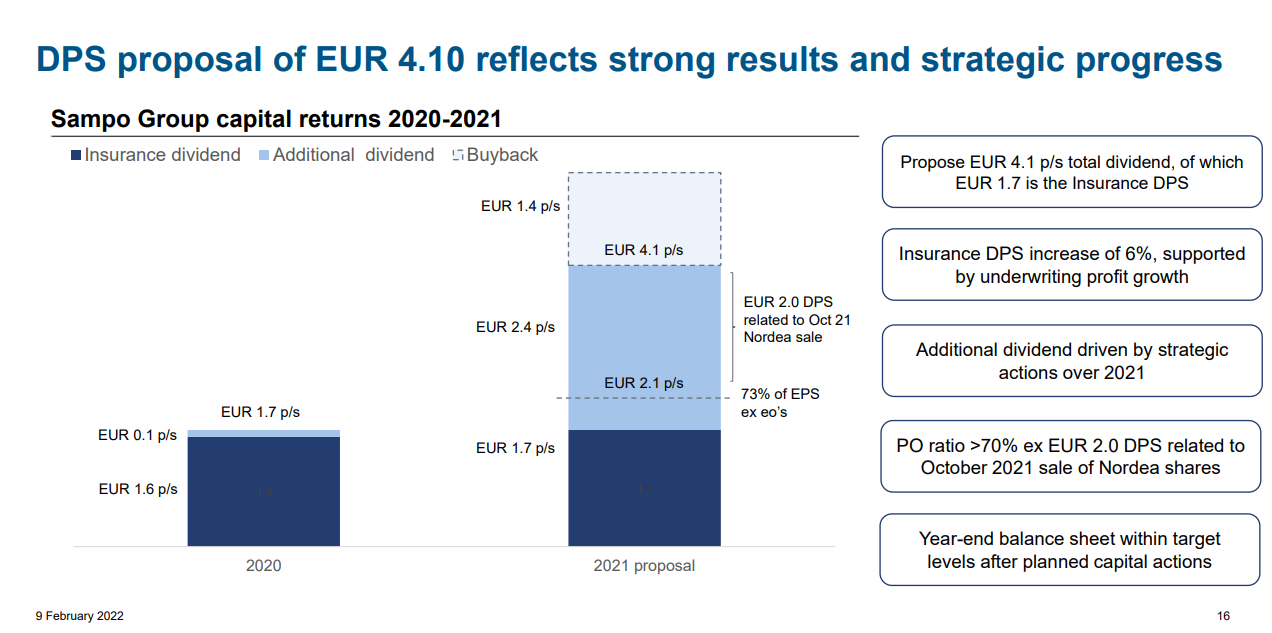

Osaatko @Mirko_Sampo_IR kertoa miksi Sampo päätti pitää vakuutusosingon tuossa 1,7 eurossa?

Sampo toki luopui kasvavan osingon tavoitteesta 2020, mutta olisihan viime vuoden tuloksessa (2,86) ollut tilaa maksaa esim 1,75 euron perusosinkoa ja sitten vaikka “vain” 2,35 euron lisäosinkoa. Samassa kassassa nuo rahat kai lepäävät vaikka rahan lähde olisikin eri?

Enemmänhän tuo kai on tekninen juttu, mutta käsitääkseni aika moni (instituutio) maailmalla pitää kasvavasta osingosta.

Oma näkemys on on se, että osingon ennustettavuuden lisäksi myös osingon kasvutahdin ennustettavuus on avainasemassa lisäosinko-perusosinko -splitissä.

Vaikka Sampo olisi voinut maksaa vaikka 2€ vakuutusosinkoa (+25%) niin tämä perusosingon kasvattaminen +6% tahtia on varmasti parempi indikaatio siitä, mikä on Sampon vakuutusosingon kasvattamiskyky tulevina vuosina.

Sijoittajat arvioivat jatkuvasti tulevaisuuden osingon maksukykyä ja kasvun"keskihajonta" tekee tulevaisuuden arvioinnista vaikeampaa. Ja tälläkin foorumilla on varmasti hyvä käsitys siitä, että epävarmuudella on hintansa ja käänteisesti matalammalla epävarmuudella voidaan ansaita hintapreemiota.

Yleisesti tuntuu asia olevan juuri näin, että perusosingon tulisi olla matalasti kasvavaa ja sitä kautta ennustettavaa. Voisi kuvitellla hintapreemiota tulevan huomattavasti enemmän, jos osinkoa kasvatetaan 5-6% vuositahtia ja mikäli ylimääräistä on, niin niille keksitään sitten muuta käyttökohdetta. Esimerkiksi omien osakkeiden ostoa, jos osakkeen arvostustaso sitä puoltaa. Jos nyt olisi tullut isompi vakuutusosinko niin heti ensi keväänä oltaisiin petytty kun vakuutusosinko olisi laskenut “normaalille tasolle”.

Mainonnassa, jossa Sampoa mainostetaan sijoituskohteena käytetään sloganeina muun muassa “Tylsyys on hyvästä” ja “Jatkossa entistäkin tylsempi”. Samposta voi olla varsinkaan tulevaisuudessa vaikea saada sitä paljon puhuttua bumtsibumia.

Kepler Cheuvreux toteaa arviossaan, että vahvasti menee ja antaa ostosuosituksen sekä ohjehinnaksi 52 €:

Q4: If fortsätter att gå bra

Sampo redovisade en vinst före skatt för fjärde kvartalet på 1 197 miljoner euro, 27 procent bättre än konsensus på 947 euro (InFront). Justerat för en Nordea-relaterad positiv redovisningseffekt på 662 miljoner euro och 84 miljoner euro relaterade till Nordax, uppgick resultatet före skatt till 452 miljoner euro. If skadeförsäkring rapporterade en vinst före skatt på 260 miljoner euro, 6 procent bättre än konsensus, där bruttopremierna steg 5 procent jämfört med föregående år på efter valutajustering. Den rapporterade totalkostnadsprocenten uppgick till 82,9 procent, fortfarande understödd av en positiv covid-19-effekt på 2 procentenheter. Exklusive effekterna av stora förluster och tufft väder, föregående års utveckling och covid-19-effekter, förbättrades IF:s riskkvot med 1,2 procentenheter i år. Efter denna rapport förväntar vi oss att aktien går 2-3 procent bättre än marknaden idag. Vi upprepar Köp med riktkurs 52 EUR.

jos pahoitan jonkun mielen niin pyydän anteeksi. tiedostan myös, että mielipiteet sisältävät voimakasta jälkiviisautta.

+IF teki huipputuloksen yritysvakuutusten hinnankorotuksilla vaikka syömähammas eli autovakuutukset olivat monessa maassa varsinkin tärkeimmässä maassa ruotsissa alamaissa uusien autojen ostojen pienen kysynnän vuoksi.

-minusta tuo Hasting oli virheliike. Hastings kasvoi vuosia uuden liiketoimintamallin ansiosta todella hienosti. mulla on kuitenkin se käsitys, että tällaiset kasvuluvut on raa-an kilpailun vuoksi mennyttä enkä oikein ymmärrä Wahlroosin innostusta yhtiöstä. Sammon kokonaishankintahinta on melko kallis.

-Nordeapossa saatettiin myydä tulevaisuuden kassavirtoja ajatellen alle P/E 10 (nousevat korot) ja nyt joudutaan ostamaan vakuutustoimintaa (hastings) ehkä historian kalleimmassa syklissä jopa P/E 25 (topdanmark). minusta tällä tavalla on vaikea tehdä rahaa. samalla ostetaan korkealla sammon kurssilla omia osakkeita.

Kuten Sauli toteaa yllä, niin todellakin Sammon Topdanmark blokkikauppa viime joulukuulta voi hyvinkin osoittaa Sammon ostotarjouksen Topdanmarkista jo tälle keväällä. Niille joille keplaa osakevaihto, niin tyrkyllä on 4,1€ jossa sisällä vakuustusosingon 6% nousu 1,7€ ja Sammon omien osakkeiden osto. Niille joille kelpaa vain raha, niin siihen löytyy hyvin loppujen Nordea osakkeiden myynti. Tosin Nordean hyvä osinko kuin omien osakkeiden osto voi olla myös vaihtoehto Topdanmark osakevaihtoon. Eiköhän tämä ole jo taputeltu juttu, odetaan vaan että tylsä osinkolinko Sampo uskaltaa tulla ulos kaapista.

Auts. Tuossa jutussa on kyllä nyt virhe jos toinenkin. Pyydämme KL:ää korjaamaan jutun.

Hallitus siis ehdottaa yhtiökokoukselle valtuutusta omien osakkeiden hankintaan - samalla tavalla kuin aiempinakin vuosina. Mitään päätöksiä uuden osto-ohjelman aloittamisesta ei ole tehty. Mahdollisen osto-ohjelman aloittamisesta päättää hallitus yhtiökokoukselta saamansa valtuutuksen nojalla.

@TomiP Meidän päässä tosiaan virhe, jota ehdin jo vähän oikomaan välittömästi jutun julkaisun jälkeen, mutta johon jäi vielä väärä osto-ohjelma-sana kummittelemaan. Virhe lähti alkujaan liikkeelle Bloombergilta, joka oli tulkinnut tuota rutiininomaista ilmoitusta rohkeasti otsikolla “Sampo unveils $2.6 billion plan to buy back more shares”.

Kuten Mirko sanoikin, niin ei siis todellisuudessa mitään uutta auringon alla.

Tämä oli hieno ja odotettu päivä. Henkilökohtaisesti odotan 50 euron kurssitason läpimenoon hyvissä ajoissa ennen osingon maksua. Nyt tuli enemmän ylimääräistä osinkoa, mitä markkina odotti ja tulevaisuudessa tulossa vielä rekkakaupalla lisää. Topin ostolla ei ole mikään kiire ja ennemmin ostaa sitä markkinoilta niin paljon, kuin saa ja varmasti jatkuvasti vapautuu isoja blokkeja myyntiin suurilta sijoittajilta. Miksi maksaa Topin omistajille mitään preemiota, kun markkinoilta saa ”markkinahintaan” Kannatti pitää tätä lappua ylipainossa, hieno päivä:champagne:

Vielä lisäyksenä omaan kommenttiini, että suuria blokkikauppoja ei toteuteta yleensä mrkkinahintaan vaan noin 5% alennuksella. Ei siis mitään järkeä maksaa Topin omistajille mitään preemiota ja ostaa vain markkinoilta. Siinä vaiheessa, kun Sammon omistusosuus Topista todella suuri voi lopuista maksaa jonkin pienen preemion.

Compare this to Tryg (biggest competitor) where cost ratio in 2021 was 14.1 % (this is on a group level, could not find by country). The big difference may be partly due to different definitions relative to cost levels but anyhow: going forward Sampo cannot compete for ever with this cost basis in Denmark. Something need to give

Edit: dont get me wrong here I would like that Sampo would get Topdanmark as cheap as possible (ca 50% of my portfolio is in Sampo ) but I am also rational.

00:00 Q4 Highlights

01:30 Performance since launching the new strategy

02:30 Rising interest rates and inflation

08:10 Purchase of Topdanmark shares

10:40 Divesting of Nordea in hindsight

12:05 Allocation of extra capital

14:10 If guidance

Sammon CFO Vernerin haastiksessa tilinpäätöksen jälkeen.

mun mielestä toi on cost ratio, kun taas IF expence ratio oli 17,2% Q4. Vastaava Trygillä 14,1%. näitä on yhtiöiden välillä vaikea verrata, kuten sanoit.

En tiedä onko tanskanmaalla näin, mutta luultavasti sammon pitäisi tehdä ostotarjous koko puljusta jos/kun omistus ylittää 50%? Toki preemiota ei olisi pakko maksaa vaan tarjous voisi olla blokkikaupan hinnalla, mutta se saattaisi taas olla huonoa PRää. Ja eikö tämän 50% rajanylityksen-pelon takia Top ole lakannut ostamasta omia osakkeitaankin?

Kiitos nopeasta vastauksesta, eikö tanskassa ole ostotarjousvelvollisuutta kuin 1/3 osuuden kohdalla, vai johtuuko tämä jostain muusta? Esim. koska aiempi ostotarjous kariutui.

2016 ostotarjous:

Velvollisuus tehdä pakollinen ostotarjous on syntynyt, kun Sampo on 6.9.2016 ja tämän päivän välisenä aikana ostanut markkinoilta 200 000 Topdanmarkin osaketta osakkeen korkeimman ostohinnan ollessa 183 Tanskan kruunua (“korkein maksettu hinta”), minkä seurauksena Sammon omistus Topdanmarkissa on ylittänyt Tanskan lain edellyttämän yhden kolmasosan rajan kaikista Topdanmarkin osakkeiden tuottamista äänistä.

")