mun mielestä toi on cost ratio, kun taas IF expence ratio oli 17,2% Q4. Vastaava Trygillä 14,1%. näitä on yhtiöiden välillä vaikea verrata, kuten sanoit.

4 tykkäystä

En tiedä onko tanskanmaalla näin, mutta luultavasti sammon pitäisi tehdä ostotarjous koko puljusta jos/kun omistus ylittää 50%? Toki preemiota ei olisi pakko maksaa vaan tarjous voisi olla blokkikaupan hinnalla, mutta se saattaisi taas olla huonoa PRää. Ja eikö tämän 50% rajanylityksen-pelon takia Top ole lakannut ostamasta omia osakkeitaankin?

Kenties @Mirko_Sampo_IR tietää Tanskan pörssin säännöistä?

Kiitos nopeasta vastauksesta, eikö tanskassa ole ostotarjousvelvollisuutta kuin 1/3 osuuden kohdalla, vai johtuuko tämä jostain muusta? Esim. koska aiempi ostotarjous kariutui.

2016 ostotarjous:

Velvollisuus tehdä pakollinen ostotarjous on syntynyt, kun Sampo on 6.9.2016 ja tämän päivän välisenä aikana ostanut markkinoilta 200 000 Topdanmarkin osaketta osakkeen korkeimman ostohinnan ollessa 183 Tanskan kruunua (“korkein maksettu hinta”), minkä seurauksena Sammon omistus Topdanmarkissa on ylittänyt Tanskan lain edellyttämän yhden kolmasosan rajan kaikista Topdanmarkin osakkeiden tuottamista äänistä.

6 tykkäystä

Sammolla ei ole ostotarjousvelvollisuutta edessä. Vasta sitten 90% kohdalla täytyy Suomen tapaan lunastaa vähemmistöosuudet.

57 tykkäystä

Hyvä huomio ja kiitos @Mirko_Sampo_IR nopeasta vastauksesta.

1 tykkäys

Pari huomiota juuri päättyneestä Sammon konffapuhelusta, ennen kuin transkripti julkaistaan.

- Konffapuhelussa SEB:n Per Gronborg kysyi Topdanmarkin osakkeiden ostosta.

Vastaus tallenteella ajasta 44:10 eteenpäin. → Conference call on Results for 2021

Magnusson: “We think that Topdanmark is priced in parallel with rest of Nordic P&C market. We were able to increase our holding a little bit, a tiny bit at market price. That makes sense for us.”

osakkeita tarjottu Sammolle:

“They were offered to us. What we consider a fair price. We didn’t run around looking for them.”

- Konffapuhelun perusteella voidaan ainakin sanoa, että Hastings näyttää kiinnostavan analyytikkoja. Hastingsin tilanteesta kysyivät ainakin Nordean, UBS:n, HSBC:n, Bank of American, ABG Sundal Collierin, SEB:n, Jefferiesin analyytikot.

- Hastingsin Toby van der Meer totesi markkinoilla monen yhtiön olevan hyökkäysvaiheessa (~ many players are aggressive).

- Toinen kysyjä UBS:n Hardcastle kysyi myös Hastingsin kasvusta ja hinnoittelusta (ajasta 16.50). Tobyn mukaan Hastingsin tavoin markkinoilla on hinnoittelussaan kurinalaisempia yhtiöitä mutta markkinoilla riittää myös kilpailuun keskittyviä yhtiöitä.

Aika pitkälti samat asiat sanottiin kuin raportissa. Hastings on jakanut kurinalaista hinnoitteluaan markkinoilla, joilla hintakilpailu oli kireää. Integrointi on aikataulussa, kuten lisämateriaalin s. 12 todetaan.

Hastingsin CEO taisi sanoa markkinoiden olevan uudessa tilanteessa. Murroskausi on siis meneillään. Taustalla FCA:n autovakuutusten reilun hinnoittelun säännökset, Brexitin seurauksena autojen korjauskustannukset ovat nousseet,

-

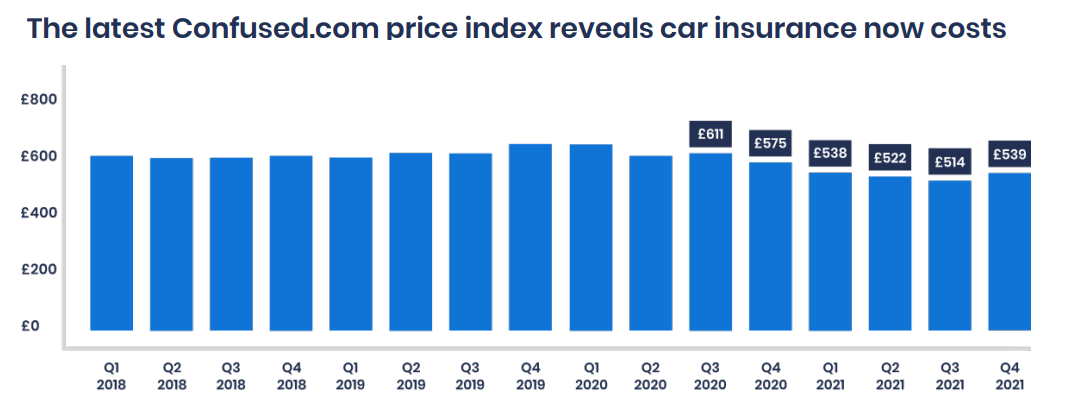

Willis Towers Watsonin ja Confused.comin päivityksen mukaan autoilijan on nyt maksettava keskimäärin 539 puntaa autovakuutuksesta. Keskihinta kääntyi nyt nousuun neljän peräkkäisen neljänneksen laskun jälkeen. Kolmannella neljänneksellä vajottiin alimmille tasolle kuuteen vuoteen (514 puntaa)

Kuvan lähde: Confused.com Price Index Q4’21 (pdf) -

British Insurers Association tiedotti 5. helmikuuta liikennevakuutuksen keskihinnan vuonna 2021 pudonneen alimmalle tasolle kuuteen vuoteen. Cost of motor insurance in 2021 was at a six-year low, but signs that cost pressures could be starting to bite according to the ABI

-

Reutersin jutussa 19. tammikuuta Willis Towers Watsonin johtaja Tim Rourke kommentoi tilannetta. Hänen mukaansa se, miten vakuutusyhtiöt reagoivat uusiin sääntöihin hinnoittelullaan ja tuotestrategiallaan, määrittää, kuinka myrskyisiä tulevista kuukausista tulee.

49 tykkäystä

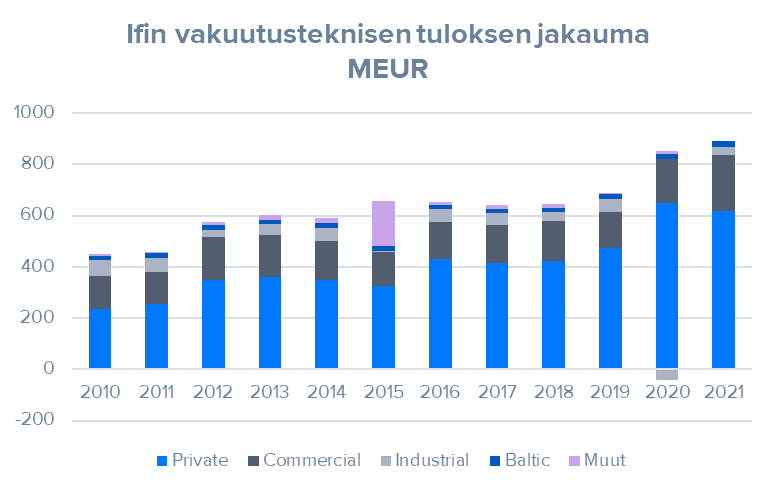

Tämä taisi jäädä kunnolla vastaamatta aamun livessä, mutta If tekee enemmistön tuloksesta kuluttajapuolelta ja siellä ajoneuvovakuutukset ovat tosi isossa roolissa.

Ifin vuoskarista (https://www.sampo.com/globalassets/vuosi2020/if/if_annual_report_2020.pdf) löytyy tarkempaa infoa myös vakuutuslajeista (esim sivu 53).

21 tykkäystä

Varmaan tuo preemio olisi oikealla pallokentällä jotta bidi menisi läpi. Pitää muistaa, että Sammon ei ole pakko tehdä bidiä, vaan yhtiö voi imuroida osakkeita markkinalta haluamaansa tahtiin, nyt kun Topin suhteen se “ensimmäinen kivi on heitetty”.

Sammon johdollahan oli ääni muuttunut ihan totaallisesti kellossa tuossa konffapuhelussa. Enää ei puhuttu miten kallis Topdanmark on, vaan yritettiin enemmänkin argumentoida mahdollisen ostotarjouksen/omistusosuuden kasvattamisen puolesta. Pidän suhteellisen todennäköisenä, että Sampo jatkaa Top ostojaan ja mitä suuremmaksi omistus kasvaa, niin sen suuremmaksi nousee ostotarjouksen todennäköisyys.

Mielestäni tämä on lopulta ihan hyvä juttu, sillä Topin ostossa on isot synergiat ja Sampo on ajanut itsensä tilanteeseen jossa Topin osto alehintaan ei ole mahdollista. Kumpi on sitten pahempi? Maksaa Topista vähän kovempi hinta ja saada synergiat vai vatvoa Topin kanssa lisää vuosia ja jättää synergiat saamatta (muistakaa, että If Tanskan tilanne ei ainakaan parane ajan myötä). Mielestäni tuo ensimmäinen on parempi vaihtoehto, vaikka se ei olekkaan optimaalinen (osta halvalla ja saa synergiat).

52 tykkäystä

Vaikka pitkään olen Sammon omistajana ollutkin kiitän teitä foorumilaisia hyvistä ja opettavaisista näkökannoista.

Ei ole varmaankaan kenellekään epäselvää, etteikö olisi saavutettavissa selviä synergiaetuja Sammon ostaessa Topin.

Toisaalta olemme saaneet lukea tälläkin palstalla Topin omistajien (tai ainakin yhden) näkemyksen siitä että omistus on naulattu kiinni, odottamaan Sammon Topin ostoon liittyvän preemion suuruuden toteutumista.

Sampo omistaa nyt a 49,4 prosenttia Topin osakkeisiin liittyvistä äänivallasta. Käytännössä puolet osakkeiden antamasta äänimäärästä Topista on Sammolla enää vajaan prosentin osakemäärän päässä.

Viime aikaisesta keskustelusta voisi päätellä että olemme osakkeiden arvostuksen lähitulevaisuuden suhteen matkalla kuplasta karhuun, jota vauhdittaa vielä korkojen nousun tarjoamat laajemmat mahdollisuudet sijoittaa pääomia mahdollisimman tuottavasti.

Itse pohdin nykyisessä tilanteessa vaihtoehtoa, jossa silkkihansikkaat riisuttaisiin pöydälle ja Sampo käyttäisi Topin 2022 yhtiökokouksessa isännän ääntä ja toteuttaisi Sammon ja Topin “kaupan” osakevaihtona tai yhdistymisenä. Tässä tilanteessa voisi ottaa esimerkkiä Valmetin ja Neleksen yhdistymisestä, jossa kumpikin yhtiö jakaisi “ylimääräisen” pääomansa osakkailleen ja tämän jälkeen astuttaisiin avioon sovitulla vaihtosuhteella.

Ovatko keskeisessä roolissa olevat Topin institutionaaliset sijoittajat valmiita tässä epävarmassa markkinassa valmiita odottamaan Sammon mahdollista päätöstä Topin ostamisesta ja reilun preemion saamista, vai tyytyykö joku nykyiseen hintaan ja tarjoaa Sampolle mahdollisuuden luopua silkkihanskoistaan.

Villiä ajatuksen juoksua mutta lieneekö millään muotoa mahdollista?

Korjaan kuitenkin tuon yhtiökokouksen vuoden 2023:ksi

12 tykkäystä

Näin pystymetsän miehenä olen samaa mieltä, että kun Sampo omistaa puolet Topista ja on varmaankin suurin omistaja, niin luulisi sillä voimalla kykenevän sanoa, että nyt tehdään whatever fuusio. Ovatko kaikki muut 50% omistajat asiaa vastaan? Vai olisiko jokin osakevaihto Sammon omistajille heikko ja siksi sitä ei nyt tapahdu. Voisiko joku asiaa tunteva kommentoida tätä asiaa? Eikös OP-Saari ajatellut tämmöistä joskus viimevuoden lopulla, muistan sanan osakevaihto.

Mikä estää Sampoa myymästä Tanskan toimintoja Topdanmarkille. Jos Top Danmark saa Tanskan toiminnot ja Sampo vastikkeeksi liikkeelle laskettavia Topdanmarkin osakkeita jolloin Sammon omistus osuus nousee ja synergiat totetutuvat.

9 tykkäystä

4 tykkäystä

koska uusien autojen vakuutukset on näin oleellinen osa IF:in portfoliota niin mielestäni tämäkin tukisi topdanmarkin hankintaa. miksi muka? koska tryg on vahvistanut asemaansa tanskan lisäksi norjassa ja ruotsissa rupeaa heilläkin olemaan kilpailukykyinen paletti eri automerkeille kilpailla IF:in kanssa soppareista. jos IF:illä olisi kaikki pohjoismaat niin etumatka Trygiin olisi vielä selvä.

Nordea julkaisi päivitetyn Sampo-analyysinsä. Suositus pysyy OSTA-tasolla, tavoitehinta nousee 50 euroon (edellinen 49 €).

37 tykkäystä

Salkunrakentajan Jorma Erkkilä kirjoitti myös Sammon hyvistä meiningeistä ja tunnelmista. ![]()

" Sammon konsernijohtaja Torbjörn Magnusson kertoo tuovansa mielellään esille konsernin edistymisen strategisessa tavoitteessa keskittyä konsernin ainutlaatuiseen vahinkovakuutustoimintaan.

Koko vuodelle tuli kasvua 19 prosenttia, joka ylittää selkeästi tavoitteeksi asetetun 4–6 prosentin vuosittaisen kasvun."

"Hulppean osinkopotin lisäksi Sammon 750 miljoonan euron suuruinen omien osakkeiden takaisinosto-ohjelma jatkuu. Osto-ohjelma ja ehdotettu osinko yhteenlaskettuna pääoman palautusten määrä nousee lähes kolmeen miljardiin euroon.

”Tulevat pääoman palautukset huomioiden taseemme on määrittelemiemme tavoitteiden mukainen ja siten kalibroitu sekä joustavuuden että tehokkuuden mahdollistamiseksi”, Magnusson toteaa."

21 tykkäystä

OPn tavoitehinta nousee 52€ (OSTA)

“Optimaalista suojaa inflatoriseen ympäristöön”

26 tykkäystä

Tätä skenaarioitahan osa markkinatoimijoista on nostellut esiin. Periaatteessa tämä on ihan mahdollinen, mutta se vaatii myös muiden osakkeenomistajien hyväksynnän. Täällä on ehdotettu “silkkihanskat pois” skenaariota, missä Sampo käyttäisi hyväksi lähes 50%:n omistajuuttaan. Tässä hyvä muistaa, että osakeyhtiölaki asettaa aika paljon rajoitteita ja luonnollisesti Topin hallituksen pitää puolustaa KAIKKIEN omistajien etuja, eli Sampo ei voi tehdä mitä haluaa vaikka omistus olisi yli 50%.

Olisiko tuo skenaario sitten mieluinen muille Topin omistajille? Periaatteessa miksipä ei? Top nousisi Tanskassa samaan kokoluokkaan Trygin kilpailemaan markkinajohtajan paikasta ja tuossa järjestelyssä olisi selkeitä synergioita tarjolla. Sammon kannalta tämä on sitten vähän niin ja näin, sillä Tanskan If revittäisi pois Sammon IT-järjestelmistä etc. ja ajettaisi sisään Topin järjestelmiin. Lisäksi brändit varmasti yhdistettäisi etc. Tämä hankaloittaisi aika paljon mahdollista tulevaa integraatiota Ifin ja Topin kanssa, eli en ole ollenkaan varma haluaisiko Sampo tehdä tätä liikettä, kun end-game on kuitenkin Topin ostaminen. ![]()

28 tykkäystä

Analyytikon aamukatsauskommentit. ![]()

11 tykkäystä

Onko muuten kukaan laskenut täällä potentiaalista Sammon tuloksentekokykyä tai EPS-tasoa, jos Toppi ostettaisiin pois?

7 tykkäystä

Topin omistajille kuuluva tulososuus verojen jälkeen on 2022 ennusteilla hieman yli 100 MEUR. Tämä jäisi jatkossa Sammolle, eli nykyisellä osakemäärällä noin 0,18e/osake. Oletuksena tässä, että kauppa rahoitetaan käteisellä, eikä velalla. Jos tähän käytettäisi velkaa, niin EPS vaikutus luonnollisesti laimenisi jonkin verran. Tähän päälle sitten synergiat (karkea työluku ennen veroja 50-100 MEUR) eli 0,08-0,16e nykyisellä osakemäärällä. Kokonaisuutena siis voitaisi puhua 0,26-0,34e potentiaalista ilman velan kustannuksia eli reilu 10% korotus tulosennusteisiin.

40 tykkäystä