Nyt löytyi helmi Title insurance markkinasta!

Hyvin silmiä avaavaa, vaikka periaatteessa tämä kaikki oli jo tiedossa. Tämän kun lukee, niin nämä “title insurance is a scam” jutut alkaa näyttäytyä aika totuudenmukaisina. Lähdekin on luotettava Business Insider.

Vahvistaa myös Voxturin AOLn tarinaa. Rahoituslaitokset haluaa/tarvitsee edelleen vakuuden, että laina on myytävissä secondary markkinalla. Eipä tässä paljon muusta olekaan kysymys koko asiassa.

Vahva lukusuositus!

For decades, America’s economic rules have been rigged to the benefit of homeowners. There’s the 30-year fixed-rate mortgage, which drives down monthly payments. There are four government-backed agencies, including Fannie Mae and Freddie Mac, working to reduce banks’ risk so they’ll lend more money to a wider pool of homebuyers. There’s the tax deduction for interest paid on mortgages up to $750,000. Taken together, these efforts have played a pivotal role in creating America’s middle class.

But sitting in front of this golden, taxpayer-backed bridge to financial security is a private tollbooth. It’s run by an obscure industry that’s pretty much permitted to charge you whatever it wants for a product you’ll probably never need. It’s dominated by four big companies whose profits have surged during the decade-long housing and refinancing boom. And it bilks homebuyers out of a staggering $20 billion a year.

The product is title insurance. In the simplest terms, a title-insurance policy guarantees the seller of a home actually owns the property free and clear. If it turns out they don’t — if someone shows up claiming to be a long-lost heir, say, or wielding an undiscovered lien — the title-insurance company will step in and either resolve the problem or pay the bill.

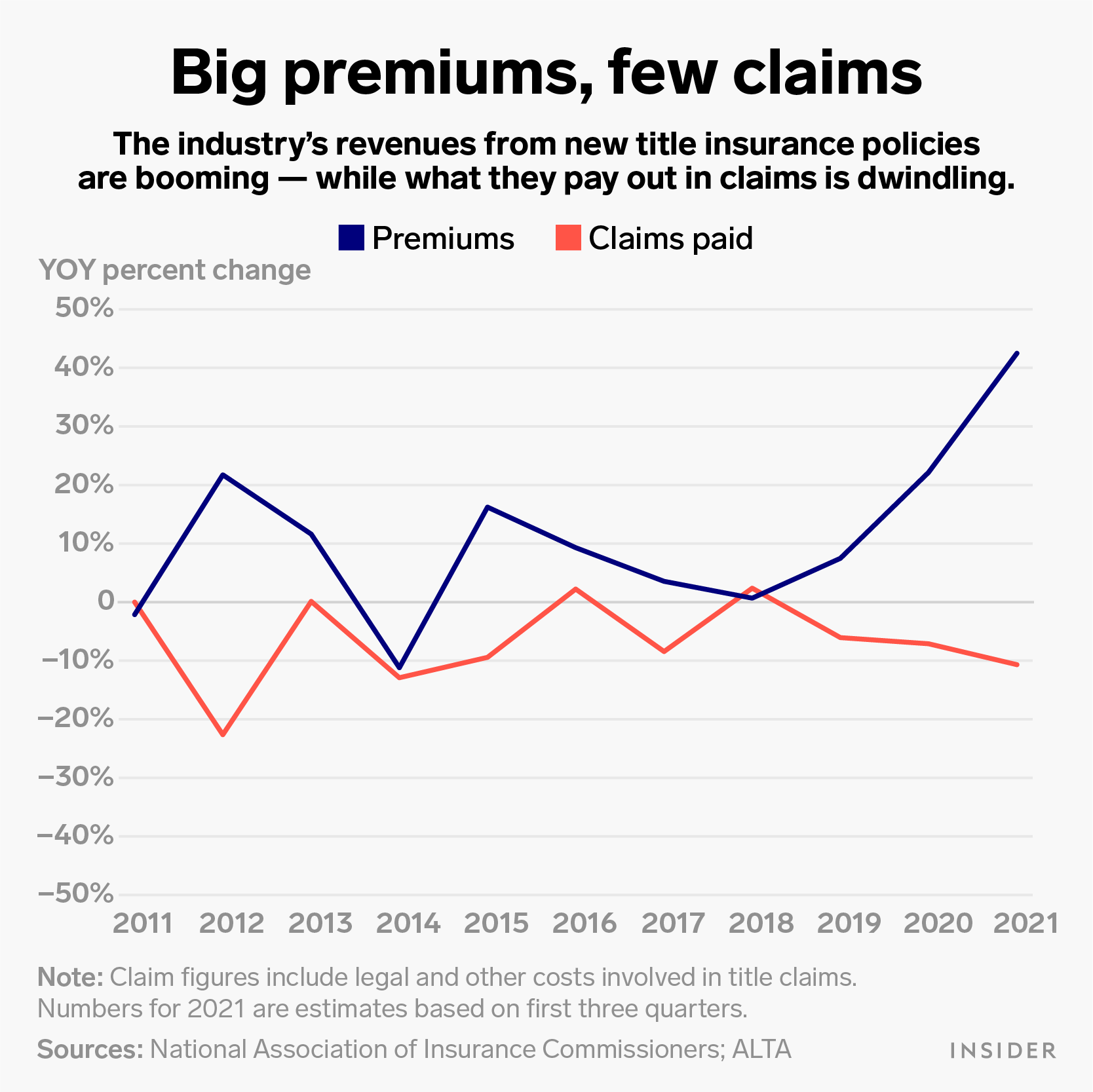

In practice, these hiccups almost never happen. More than half of car-insurance premiums are paid out in claims. Last year, title insurance paid out less than 2%. But to make a mortgage into a marketable commodity — one that other companies will purchase — banks need a guarantee they actually own the investments they’re making. So the banks have essentially created a protection racket, requiring homebuyers to purchase title insurance to protect the bank’s interest in their homes.

From the consumer’s perspective, title insurance is essentially a special license you need to show the bank before it’ll lend you the money you need to buy a house. It adds hundreds or even thousands of dollars to the price of your new home. And the cost typically isn’t revealed until after you make your offer, when it’s bundled into the mysterious catchall known as “closing costs.”

Economists call this information asymmetry — the gap between what sellers know and what they tell consumers. “People might not actually want these services, or understand what prices are negotiable, but they’re bundled into the transaction,” Ben Keys, a former Federal Reserve economist who teaches at the Wharton School, told me. “You’re bombarded with technical terms and reams of paperwork, and you wind up feeling that you simply have to write the check so you can get the keys to your dream house. It’s a real power imbalance in terms of getting from one end of the transaction to the other.”

No comparison shopping

Like millions of homebuyers, I wasn’t aware that such a thing as title insurance even existed until I bought my first home. Last summer, shortly after placing a bid on a house I’d found, I received a document called “Buyer’s Estimated Closing Costs” from my real-estate agent, Linda, a salty older woman who drove a leather-trimmed luxury car and graciously put up with my first-time-buyer jitters. The projected price of my title-insurance policy — $4,901 — stood out among the long list of two- and three-figure fees for things like document preparation and processing. That number rose to $5,105 after a second, slightly higher offer I made on the house was officially accepted.

At the time, I experienced title insurance as something like a tetanus shot — a small but necessary pain to prevent an unlikely but potentially devastating misfortune. It hurt, but it was for my own good.

The sting, however, was compounded by the fact that the house I wanted to buy was in Philadelphia, the city where title insurance was born in 1876. Almost every title agent in the state charges homebuyers according to rates set by a private board called the Title Insurance Rating Bureau of Pennsylvania. The board of TIRBOP has five officers. One is a full-time employee; the other four all work for large title-insurance conglomerates. State insurance officials have to approve the industry-set rates, but in practice they’ve done little more than push for small reductions. When TIRBOP asked for a 4.95 percent increase in late 2019, the state trimmed it back to 4.88 percent.

Prices for title insurance in Pennsylvania are among the highest in the nation. I asked Dave Buono, the state’s acting deputy insurance commissioner for market regulation, why that is. “That’s a really hard question for me to answer,” he said — an answer that surprised me, given his department’s official mission to promote a competitive marketplace that benefits consumers. “I don’t know what other states charge.”

I had the sense that I was getting a raw deal, but there wasn’t much I could do about it. There was plenty of flexibility in the case of the mortgage. Natasha, the mortgage broker Linda recommended, kept offering me better and better deals to match offers made by her competitors. But when it came to title insurance, the state-approved pricing schedule meant that shopping around wouldn’t be of much use.

“There’s no comparison shopping,” says Stewart Sterk, who teaches real-estate law at Cardozo Law School. “The people who pay aren’t in a position to do anything but pay. The banks are the only ones who have some leverage in this situation to keep rates down. But they don’t have much incentive to do so if they can pass on all the costs to homebuyers.”

There was one small loophole: I could choose to work with someone called “an approved attorney” instead of a title agent, who usually pockets 75% or more of the insurance premium. I learned this from the website of one Jeff Rosner. With him, I could get insurance for a mere $4,080 — saving me $1,025 compared with the title agent Linda recommended I use.

It felt as if these quotes were being pulled out of thin air. And that feeling only intensified when I started looking at what title insurance would have cost me if I were buying the same house in another state. The ideal place would have been Iowa, where I would’ve paid no more than $750 in premiums and related fees. That’s because Iowa handles all title insurance through a state-run company, Iowa Title Guaranty, which charges 90% less than its private-sector counterparts in Texas, New York, and Pennsylvania.

Why is title insurance so much cheaper in Iowa? For starters, the state keeps its overhead low: The director of Iowa Title Guaranty earns $130,000 a year. By contrast, annual compensation for the CEOs of the “Big Four” companies that dominate 80% of the industry runs as high as $10 million a year. And because Iowa Trust Guaranty isn’t pocketing any profits, it’s able to return some $2 million a year to the state — money that’s used to support first-time homebuyers.

Title insurance is “basically an oligopoly,” says Gerald Glombicki, who tracks the industry for Fitch Ratings, a leading credit rating agency. The Big Four devote a lot of money to lobbying the banks and real-estate brokers who can steer business their way. That gives them an incentive to charge higher prices, so they can shower banks and brokers with all kinds of perks, from steakhouse dinners to luxury boxes at NFL games. In a subtler but more lucrative system of kickbacks known as “captive reinsurance arrangements,” a broker or builder steers a homebuyer to a title-insur (loppua en saa kiinni millään…)