Täältä myös Q4-presentaatio ja rapsa haltuun: https://bettercollective.com/investors/

En itse ehtinyt kuin plärätä läpi, mutta tuokaahan löydöksiänne tänne jos ehditte tutustua tarkemmin

Tästähän on kovaa vauhtia muodostumassa oikea kassavirtakone Lisäksi kun voittoja käytetään omien osakkeiden takaisinostoon (viime vuoden lopulla 5m€ arvosta, eilen ilmoitus uudesta 10m€ ohjelmasta), niin voittojen kotiutus on myös pienomistajille edukasta. Myös tälle vuodelle saatiin ihan mukavat kasvutavoitteet (liikevaihto 290-300m€, EBITDA 90-100m€, kuva näistä alla), vaikkei nyt toista rakettivuotta peräjälkeen tulekaan.

Arvelinkin jo, että Betcon viime vuosi saattoi sujua mainiosti, sillä vedonlyöntiyhtiöillä liikevaihdot olivat mallikkaita, mutta marginaalit pettivät - ja Betcohan saa tuloksensa joko revshare-mallilla tai kiinteillä soppareilla. Mutta enpä silti uskaltanut lisäillä syksyn aikana - onnea niin tehneille

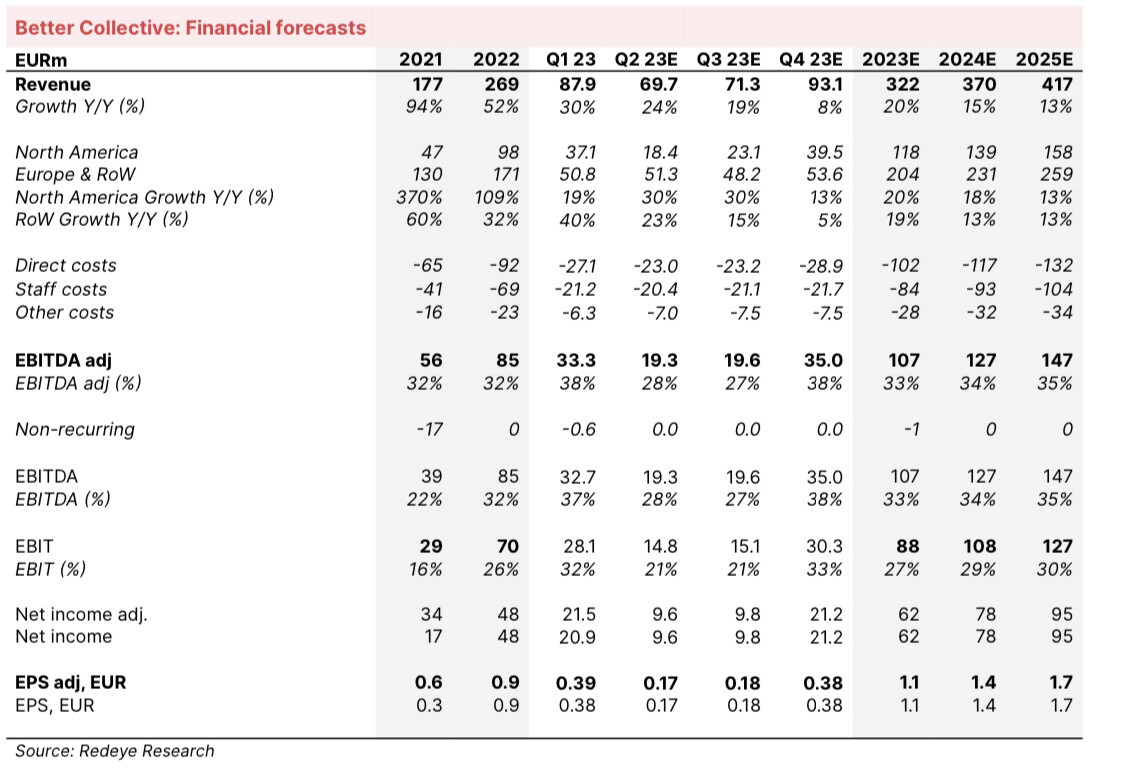

Redeye updates on Better Collective following its Q4-results which were stronger than expected driven by the US market and a strong performance during the FIFA WC. We were also encouraged to see strong growth of recurring revenue for which the company also introduced a new key metric which includes subscription revenue and CPM in addition to revenue-share income. The company’s updated financial targets for 2023 were largely in line with our expectations, although we slightly trim our EBITDA estimates owing to growth investments in a new markets and an adtech platform. Our valuation range is increased however due to a lowered discount rate following an updated rating and our new base case stands at SEK325 (SEK270).

In conclusion, Better Collective’s CMD confirms a positive growth outlook in the coming years. The company has a strong track record of achieving its targets and we expect the company to continue to deliver on its new targets in the coming years. The expansion into new revenue streams could also have potential to drive a higher valuation of the company is this will reduce the mix of revenue coming from online gambling. Overall, our positive view of Better Collective remains and has strengthened on the back of the CMD.

Tuossa pohdiskelin tullaanko ohjeistukselle mitä tekemään. Q2 ja Q3 kausiluontoisesti hieman heikompia kesätaukojen myötä. Jalkapallon MM mukavasti sotkemassa pakkaa, kun oli poikkeuksellisesti viimeisellä kvartaalilla. Ei harmainta hajua mitä markkinat odottivat tältä kvartaalilta, mutta vaikutti ihan ok tietäen tuon suurtapahtuman olleen viime kvartaalilla

Tase alkaa olla jo paremmassa kunnossa. Ehkäpä siellä on lisää yritysostoja odotettavissa?

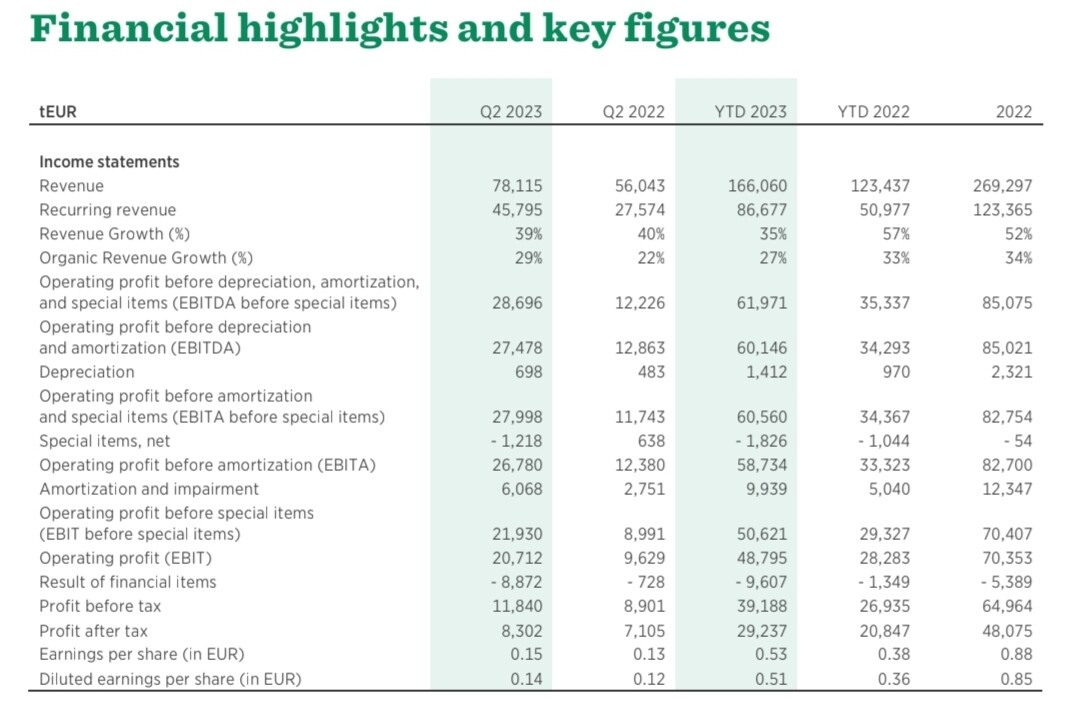

Better Collectiven osari tuli eilen pörssin sulkeutumisen jälkeen. Tulos ylitti Redeyen odotukset. Etelä-Amerikka vahvana Q1:llä. Myös Q2 alkanut Better Collectivella hyvin, huhtikuussa 40 prosenttia kasvua verrattuna edelliseen vuoteen.

Better Collectiven base-tavoitehinta on Redeyella 325 kruunua ja osake kuuluu Top Pickseihin.

Better Collective announces an upgrade of its 2023 financial targets. Following its record-breaking Q1, the group has carried on its strong momentum into Q2, highlighting above expected performance from the Americas, media partnerships, and the sports win margin.

New 2023 financial targets

Revenue of 315-325 mEUR (previously 305-315 mEUR)

Implying 17-21% YOY growth

EBITDA before special items of 105-115 mEUR (previously 95-105 mEUR)

Implying 24-35% YOY growth

Net debt to EBITDA before special items <2.0 (unchanged)

“All in all, we increase our 2023E EBITDA with c5% driven by the updated financial targets, while 2024-25E EBITDA is increased with 6% driven mainly by the acquisition of Playmaker HQ. On the back of the increased estimates, we also raise our valuation range where the new base case stands at SEK360 (SEK340) while the new bull case is SEK500 (SEK470) and the bear case SEK200 (SEK195)”

Digital sports media group Better Collective strengthens its position in Sweden through the strategic acquisition of four flagship sports media brands from Everysport Group. The acquired brands include SvenskaFans.com, HockeySverige.se, Fotbolldirekt.se and Innebandymagazinet.se with a combined reach of 9 million monthly visits from dedicated Swedish sports enthusiasts.

Transaction details

The total purchase price will be 3.7 mEUR paid in three installments and will be financed with cash. Better Collective estimates that the post synergy 2024 EBITDA multiple will be below 3x. The 2023 financial targets remain unchanged following the acquisition.

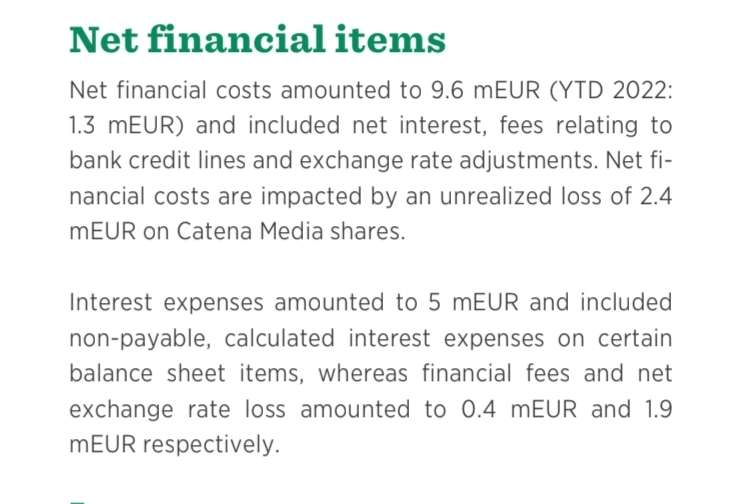

Ylärivillä hyvää tekemistä vs ennusteet mutta kyllähän tuo nettotulos ja EPS jätti hieman toivomisen varaa. Isoimpana syynä tuo tuloslaskelman kohta “result of financial items”, mikä pitää sisällään lainakorkoja yms (tarkemmin alla). Ja näiden kokoluokan oli Redeye arvioinut kyllä aivan päin mäntyä

Tutustun huomenna tarkemmin itse rapsaan, mutta odottaisin lievästi positiivista kurssireaktiota.

Edit: @Gadus käytännössä Redeyen arvio oli, että tuo erä, joka siis sisältää korkokulut, olisi ollut yhteensä alle 1m€ (toteuma lähes 9m€, josta 5m€ korkoja). Heidän laskelmassaan Ebitistä ei siis tarvitse vähentää kuin verot, niin ollaan jo aika lähellä tuota nettotulosta.

Tämä siis todistaa sen, että RE:n laskelmiin pitää jatkossakin suhtautua erittäin kriittisesti, jos näinkin olennaisia ja yksinkertaisia asioita unohdetaan huomioida. Nyt EPS osui lankulle vain sen takia, että Betco ylisuoritti operatiivisesti - muuten tulos olisi ollut n. puolet arvioidusta, ja kurssireaktio sen mukainen…