Aika hidasta näyttää olevan neuvotttelu ja päätöksenteko tällä hetkellä. Paljonkohan noita osakkeita on mahdollista antaa ulos vielä tuon edellisen yhtiökokouksen päätöksen perusteella? Saattaa olla, että tulee ensin suunnattu anti sittenkin, että nuo tilit saadaan auki. Luulisi, että ilmoitus yhtiökokouksesta ei veisi kovin pitkään.

2 tykkäystä

Kuten tunnettua, odottavan aika on suhteellisen pitkä, joten taidanpa uutta tiedonantoa odotellessa pienenä kevennyksenä itselleni laittaa soimaan YÖ-yhtyeen kappaleen: “Niin paljon me teihin luotettiin”.

6 tykkäystä

“Preliminary data from the study were presented during the 2023 ASH Annual Meeting. At a data cutoff date of May 2, 2023, a total of 26 patients had been enrolled to part 1 of the study. The median patient age was 68 years (range, 22-85), and 77% were male. Sixty-nine percent of patients had AML, 15% had MDS, and 15% had CMML.”

" In terms of efficacy, 50% of 6 response-evaluable patients with AML who received the agent at 96 mg experienced a response to the agent after 1 cycle of treatment. Moreover, 1 patient with adverse genetics in the form of complex karyotype and a TP53 mutation, achieved a complete remission with incomplete count recovery and continued to be in remission after 3 treatment cycles. Another patient with AML and adverse genetics, complex cytogenetics, and TP53 mutations who had previously received 2 regimens achieved a morphologic leukemia-free state (MLFS) and is pending count recovery. A third patient who had AML and normal cytogenetics, adverse genetics, and relapsed or refractory disease following 5 regimens and achieved an MLFS. However, complications that were not determined to be associated with ocifisertib led to dose reduction and treatment hold, and the patient relapsed."

“Grade 3 or higher TEAEs were experienced by 31% of patients.”

Ei nyt niin kovin moni ole saanut vastetta ja vakavamman luokan haittavaikutuksia 31%:lla. Orphan drug ja fast track kuitenkin saatu ym. tuloksilla.

10 tykkäystä

itekki ollu toista vuotta hiljaa ja ollut kyydissä, kyllä täytyy nyt ihmetellä faronin johdon toimintaa. jossain vaiheessa olin hyvin luottavainen mutta nyt on kyllä usko koetuksella. btw saatiin näköjään tällekkin päivälle -10%

2 tykkäystä

Noo kyseessä kuitenkin monoterapia. Et voi verrata bexmabiin millään tavalla.

1 tykkäys

Tuota on tutkittu monoterapiana (13 potilasta, ClinicalTrials.gov) joka on juuri päättymässä. Sekä menossa isompia 72 potilaan tutkimus ClinicalTrials.gov

(Non-Randomized) jossa kaksi linjaa

Experimental: 1A: Monotherapy escalation and expansion

Dose escalation and expansion arm with CFI-400945

Experimental: 2A: Combination escalation and expansion

Dose escalation and expansion arm with CFI-400945 and azacitidine

2 tykkäystä

No verrataan sitten bexmabiin kun noista kombinaatiotutkimuksista tulee dataa, sehän onkin mielenkiintoista. Mutta linkkaamasi uutinen koski monoterapiaa.

1 tykkäys

Noh parempi lääke voittakoot. Pitää muistaa että sitä käyttää ihmiset. Kurssi varmasti ponkaisee ylöspäin, kun rahoitusotku saadaan selviteltyä. Oma mutu on että mennään yli kakkosen silloin. Enempi odottelen kuiteskin vielä isompia uutisia, koska nämä ovat sivujuonteita matkalla kohti myyntiä tai konkurssia.

7 tykkäystä

12 tykkäystä

Nyt Faroniin syntyneen, kriisitilanteen selvittäminen tulisi tapahtua laillisessa järjestyksessä.

Tärkeää on, ettei osakeyhtiölakia - eikä mitään muitakaan lakeja rikota ja tehdyistä sopimuksista ei poiketa omavaltaisilla menettelyillä.

Yhtiön toimitusjohtajalla, -hallituksella ja tilintarkastajilla on vastuulla hoitaa syntynyt tilanne lakeja noudattaen.

9 tykkäystä

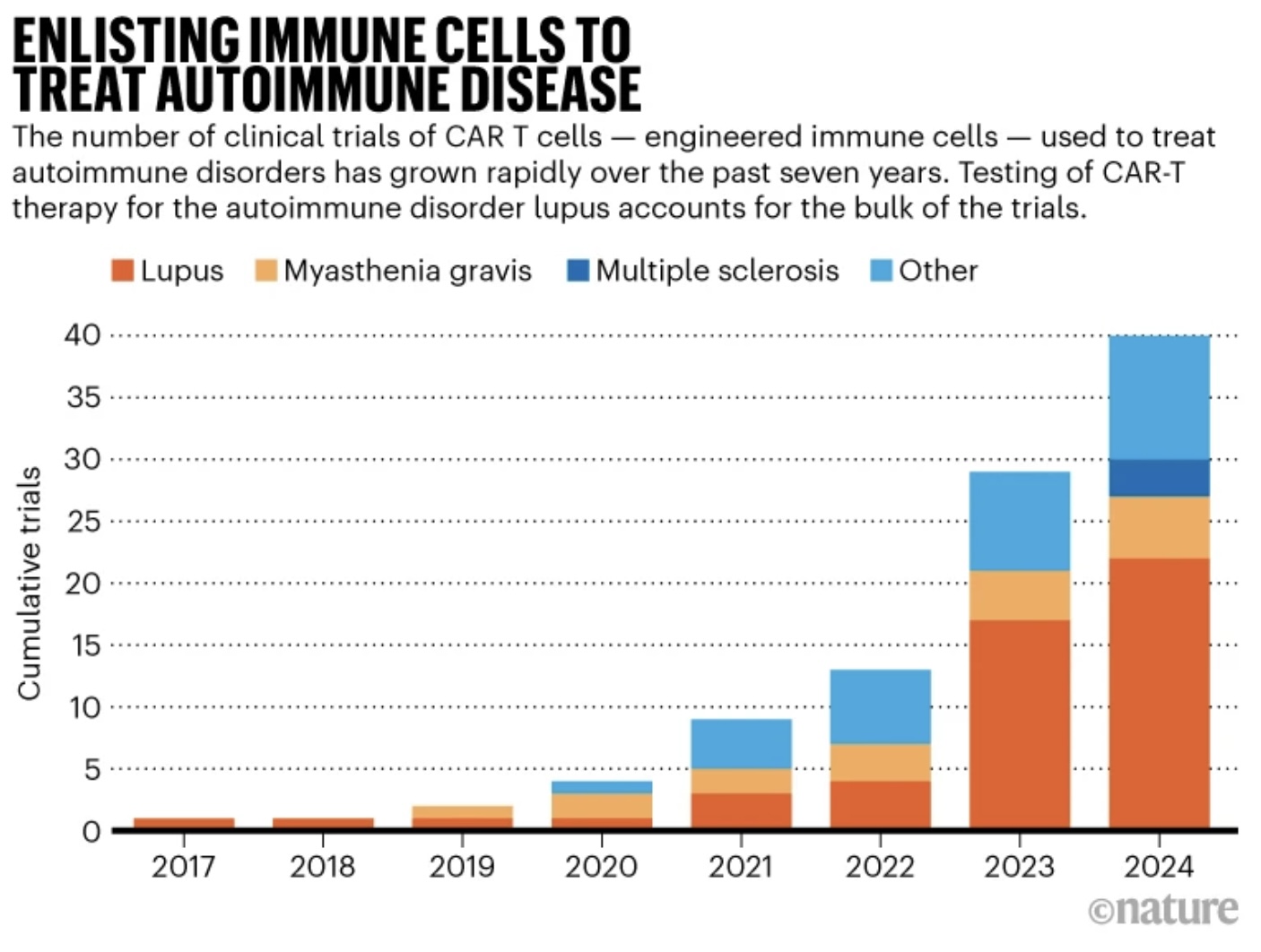

Tuota @Koodinikkari videon IFN-beta-1a eli Traumakine-trialia eli maaliskuuta odotellessa Nature-katsausta kiihtyvään CAR-T-hoidon tutkimukseen. Syöpien lisäksi sitä tutkitaan autoimmuunitauteihin, kuten reumataudit ja MS-tauti. Niissä trialeiden vuosittaisen määrän kasvu on 25-100 % viime vuosina eli aika kova.

”His biggest concern is brain toxicity, which can cause confusion, seizures and death and has been seen when CAR T cells have been used to treat cancer. The brains of people with MS are already inflamed, potentially exacerbating the danger, says Freedman, who consults for BMS but is not involved in the new trial.

Jeffrey Dunn, who is running the first trial of Kyverna’s CAR T cells in the United States, will be watching closely for brain toxicity, which he says seems to be linked to the number of B cells in circulation. B cells are everywhere in B cell cancers, but less abundant in MS. “We’re hoping that we see little toxicity,” says Dunn, a neurologist at Stanford University in California.”

https://www.nature.com/articles/d41586-024-00470-5

Syövissä kohteena olevien solujen määrä on suuri ja siten CRS riski on suurempi kuin autoimmuunitaudeissa. Neurologisten haittojen mahdollisuus on kuitenkin olemassa ja jos Traumakinella saadaan veriaivoeste paremmin pitämään, tullee se myös autoimmuuni-CAR-T edeltäväksi lääkkeeksi.

11 tykkäystä

Noh parempi lääke voittakoot.

Tartun tuohon hieman. Jos siis viittasit tällä yllä mainittuun osifisertibiin. Tämä ei varsinaisesti ole mikään kilpajuoksu missä “paras” lääkeaihio voittaa ja muut ovat sen jälkeen merkityksettömiä. Samaan indikaatioon on yleensä liuta vaihtoehtoisia lääkehoitoja ja niitä voidaan sen mukaan vaihdella miten potilas sietää tai on sietämättä jotakin niistä. Syitä on lääkevaihdoille monia, ei mennä nyt niihin.

Jos siis syntyi mielikuva, että bexmarilimabi olisi tässä nyt jotenkin jäämässä alakynteen tai osifisertibi olisi sille laakista vainaa -uhka, niin itse en näe asiaa mitenkään dramaattisena.

8 tykkäystä

Tälläinen osu silmään, saa asiantuntijat kommentoida tarkemmin liittyykö aiheeseen. Kiinnitin huomioita vaan nopeaan etenemiseen ja haittavaikutuksiin, jotka taitavat olla toissijaisia kun etsitään uusia lääkkeitä mitkä edesauttavat eliniän kasvattamisessa.

FDA Approves First Cellular Therapy to Treat Patients with Unresectable or Metastatic Melanoma | FDA

The FDA granted the approval of Amtagvi to Iovance Biotherapeutics Inc.

Amtagvi also received Orphan Drug, Regenerative Medicine Advanced Therapy, Fast Track, and Priority Review designations.

Among the 73 patients treated with Amtagvi at the recommended dose, the objective response rate was 31.5%, including three (4.1%) patients with a complete response and 20 (27.4%) patients with a partial response. Among patients who were responsive to the treatment, 56.5%, 47.8% and 43.5% continued to maintain responses without tumor progression or death at six, nine and 12 months, respectively.

Patients treated with Amtagvi may exhibit prolonged severe low blood count, severe infection, cardiac disorder, or develop worsened respiratory or renal function or have fatal treatment-related complications. A Boxed Warning is included in the label containing information about these risks. Patients receiving this product should be closely monitored before and after infusion for signs and symptoms of adverse reactions. Treatment should be withheld or discontinued in the presence of these symptoms, as indicated.

1 tykkäys

Lontoon sheriffin mietteitä:

"Hi Santhi . Yes I’m here ( just been on a 3 day walking holiday) . Plenty of time to chew things over in my mind , but to be honest with what we’ve been given , it’s hard to come to any firm conclusion .

Faron a have up until now been perfectly capable of raising small to medium amounts to get them to the next milestones .

Placings often over subscribed . Loyal shareholders , and they have been a shining example of how to conduct yourself . Multiple grants , and recently high profile tie up with LLS opening doors to the premier cancer treatment centres in the US .

The IPF relationship , although welcome at the time - has caused problems . The cash buffer requirement has been a constant factor in raising funds , and the previous re- negotiation , came after a period where the SP dipped into the 180’s - and IPF came out of that with a much better hand . I don’t think we have ever been given the full details of the IPF agreement - so we don’t know about any small print . But compared to say a normal loan - IPF seem to have a lock over Faron with some severe penalties , and some other share price related conditions .

So - how did we get here ?

The accounting error reason initially seemed the most obvious - but I just can’t see that as the case . Maybe it is and we are stuck in a pickle while Markku tries to get the company back on its feet ( a month to sort it won’t be a complete disaster - but it will be massive egg on face moment) but I really don’t see it . It’s like running out of petrol on the way to church on your wedding day . They can’t be that careless.

So that leaves us with IPF pulling some kind of stunt ( either alone or in step with someone else ) . For reasons to benefit either them ( some kind of extra cheap warrants/ options) that was in the contract ? Who knows . But also - surely it wouldn’t do their reputation much good if future partners with them see how they are prepared to wreck a company for their own gain .

So the third option is that a deal was being finalised - funding was expected - but for some reason didn’t arrive - and this situation occurred . IPF were handed this situation - and had full right to renegotiate their hand again - thank you very much . The SP tank will probably help them - so no rush in sorting it out while share not suspended .

Markku will not panic . There ‘WILL’ be options he can take . What they are doing now I suspect is working through waht will be best for the company ( and shareholders to a lower degree , and remember they are large holders themselves) in the longer term . They have by whatever reason - now got a chance to make themselves a bit less vulnerable .

So - for now - I am over the worrying stage . Out of our hands - all we can do is buy/sell /hold . I have read enough about the company to be confident in their abilities - and have belief in Bex .

I apologise if people have over invested here and are distraught - due to my ramping/ ultra positive nature .

As a side note - look at Avacta - massive potential . Last science day SP was at £1.50 ish . Yesterday 77p . Nothing has changed - they are still making progress -no financial issues - but they are under short attacks , and full on campaign to lower SP . They do have a very large number of PI holders , and for some reason there is the ability in the shady corners of the market to create these situations . But loyal holders will maybe try and trade a bit themselves , buy the dips and wait for the return to form , as they know the company will be worth at lot more than 77p . Likewise here . Good luck . We’ve had it easy compared to some shares . I wish them well . Poor old shareholders certainly getting a kicking all over the market at the moment ."

10 tykkäystä

Todella ruma jälki jää ainakin lyhytaikaisesti, sen näkee sitten tuleeko pitempiaikaista vahinkoa. Tiedehän sen lopulta Faronin kohdalla näyttää.

Se on varmaa että tilanne stressaa ja aika kuluu hitaasti näin talon ulkopuolella, varmasti stressaa sisälläkin, mutten usko ajan kuluvan tällä hetkellä kovinkaan hitaasti ![]()

6 tykkäystä

Omia pohdintoja:

1.Rahoitus kuntoon

2. Tutkimus ei saa keskeytyä

3.Selvitys sijoittajille

4. Syyllisten ruoskiminen ja muutosten tekeminen

5. Paluu arkeen ja tekemään historiaa

21 tykkäystä

Villejä veikkauksia minkä takia tulevan vuosikatsauksen (29.2.2024) päivämäärä hävis Faronin sivuilta?

Eikö oo sillon vielä mitään kerrottavaa? ![]()

5 tykkäystä

Tuntuu että tässä firmassa tapahtuu ennen kuin siitä mitenkään ilmoitellaan ![]() Vähän kuin appiukko osti uuden auton mutta ei uskaltanut kertoa siitä anopille

Vähän kuin appiukko osti uuden auton mutta ei uskaltanut kertoa siitä anopille ![]()

7 tykkäystä

- Ei ole asiat vielä selviä kerrottavaksi

- Jonkun toisen yrityksen tehtävä

2 tykkäystä

Ei näytä jos rahoitusta ei irtoa. Kyllä historiassa on lupaavia molekyylejä jotka vain eivät koskaan edenneet rahoituksen puuttuessa.

Tällä foorumilla on mielestäni ollut liian naiivi ilmapiiri, Faronin korkeaa arvostusta ei ole kyseenalaistettu ja ne ketkä kyseenalaistavat (CK, Pyyleva) on lytätty. Tj:n optimistiset puheet otettu faktoina. Tutkimusten kriittinen ja vertaileva arviointi unohdettu.

-Tutkimusdatan osalta kriittisin virhe mielestäni se, että bexmabin MDS tulokset tulkittu johtuvan merkittävältä osin Bexistä, ei AZA:sta koska tutkittu potilailla jotka ovat HMA-hoitoja hoitoja jo saaneet (HMA-failure). Tämä tulkittu niin että HMA lääkkeet eivät heillä antaisi vastetta ollenkaan tulevaisuudessakaan. Tälle väitteelle ei ole kyllä tutkimusnäyttöä osoitettavissa. Ei syöpätautien biologia ja lääkkeiden vaikutukset potilaassa ole pelkistettävissä miksikään flow chartiksi tai 0/1 vaihtoehdoiksi. Potilas voi respondoida myöhemmin hoitoon joka aiemmin ei toiminut. Potilas voi lakata respondoimasta samaan hoitoon. Potilas voi respondoida placeboon, tai ei mihinkään.

-Vertailu verrokkeihin katsottu Faron-lasien läpi. Keskustelua viety millon mihinkin epäolennaisuuksiin kuten yllä CAR-T hoitoihin autoimmuunitaudeissa mitkä ei ole kaupallisesti valmiita ainakaan viiteen vuoteen->Ei relevanttia. Fokus ei ole ollut Faronin valuaatiossa, Faronissa sijoituksena.

Liika sinisilmäisyys on nyt kostautumassa.

20 tykkäystä