Tässä ilmaispuolen uusin kommentti, olkaatte hyvät.

Strong first quarter, despite supply chain challenges and cost inflation

We regard Genovis’ Q1’22 report as solid. Sales came in at SEK 32.6 (15.7) corresponding to a growth of 107 % y/y (Fx-adjusted sales growth was 91% y/y). During the last quarter of 2021, Genovis entered into a partnership agreement with Selecta Biosciences to evaluate the combination of its IgG protease, Xork, and Selecta’s ImmTOR platform to enable both gene therapy for patients with neutralizing antibodies and as a treatment method for antibody-mediated autoimmune diseases (please see our research update from November 2, 2021 for a more detailed discussion around the partnership agreement). In Q4’21, Genovis received around SEK 20m of the USD 6m (SEK 59m) upfront payment, and another SEK 10m were received in Q1’22. Adjusted for this, sales for the first quarter amounted to SEK 22.6m (+44% y/y), highly in line with our adjusted sales and growth estimates of SEK 22.9m and 46%, respectively. We expect Genovis to receive remaining parts (c. SEK 16m) of the upfront payment during the course of 2022.

We are encouraged to see that Genovis is reporting yet another solid quarter and that the growth remains high, particularly in the Enzyme business (+37% y/y). This is impressive in our view since the omicron variant was still spreading rapidly across Genovis’ key markets during the beginning of the quarter. Moreover, it is comforting to learn that Russia’s war in Ukraine has had a limited impact on the business so far and that the company is actively working to make sure that its products are not sold or distributed in Russia.

In previous quarters, the antibody business (QED) has been a bit of a disappointment, partly due to the fact that it has been shown to be less resilient to the pandemic. Difficulties in meeting customers has hurt service operations and shifts in revenue between individual quarters has posed challenges. It is therefore satisfying to learn that the antibody business is growing again and that the sales trend for the antibody products that were developed for synergies with the enzyme business continues to be strong. The rationale behind the acquisition of QED was, as mentioned in previous notes/updates, to realise synergies rather than boost sales. Thus, we feel more comfortable with the acquisition now and expect gradually improving results from the antibody business over the coming quarters.

In summary, we estimate the sales split for the first quarter to be:

- ~ SEK 19.1m for Analytics/Other services

- ~SEK 3.5m for QED

- ~SEK 10.0m for Selecta Partnership/Gene Therapy

Looking at the gross profit, it grew by 96% y/y and reached SEK 29.4m (90% margin). By adjusting for income relating to the license agreement with Selecta Biosciences, the gross profit amounted to around SEK 19.4m, corresponding to a gross margin of 86% (we expected a gross margin of 85%). The gross margin is one of the key strengths with the case and the company should be able to swiftly pass on higher input costs to its customers, which is extra important in the current state of the economy with higher inflation and supply chain constraints. Although Genovis has experienced higher input costs, delivery delays as well as increased transportation costs (highest impact on its earnings) over the past months, the effects have been relatively limited so far. This is of course satisfying, even though future effects are difficult to assess at this time.

EBIT for the quarter amounted to SEK 10.1m (0.6), representing a margin of 31% (4). Adjusted for the license agreement (we estimate 90% EBIT margin), EBIT amounted to ~SEK 1.1m, corresponding to an adjusted EBIT margin of roughly 5%. This was below our forecasted SEK 4.9m, but we learn in the CEO letter that Genovis acted on several of its strategic goals during the first quarter, which rendered higher costs compared with Q1’21. Genovis has during the first quarter expanded its sales organization with local representation in Shanghai and the UK. This should enable it the strengthen its position in these markets going forward and similar initiatives have been initiated in Germany and Switzerland in the beginning of the second quarter. We foresee an increasing customer activity over the coming months on the back of eased restrictions in most of Genovis’ key markets (China is more uncertain) and argue that the company has good growth prospects over the coming quarters.

Looking at the financial position, Genovis had cash and cash equivalents amounting to SEK 78.1m by the end of the quarter. Given its strong financial position, we think that Genovis has the opportunity to increase its M&A activity and invest in new growth opportunities going forward.

Bioprocess – Still a big question

A big question is still whether Genovis will receive a follow-up order within Bioprocess. We have no reason to believe that the project has been terminated and thus continue to expect a follow-up order over the coming months. This could potentially happen already in Q2, but given the current market conditions, we have moved it into Q3. However, we continue to see this as a key near-term catalyst for the stock.

The share

The share reacted positively to the Q1’22 report and was initially up by around 8% (we expected +3-5%) and closed the day at +2.1% (SEK 49.8 per share). The YTD performance has been poor though, and the share is down by some 32%. This is of course highly attributable to the poor sentiment for, particularly, growth stocks seen lately on the back of a rising inflation, higher interest rates as well as high geopolitical uncertainty. However, owing to its optionality on the upside and its resilience to cost inflation and supply chain constraints (so far), we see this drop as a good buying opportunity for the long-term investor.

Financial forecasts and valuation

Below, we present our financial forecasts for the coming years as well as provide our quarterly estimates for 2022. As mentioned previously, we have moved a potential follow-up order within Bioprocess to Q3 on the back of the current market conditions. Besides that, we have only made some minor adjustments to our near-term cost estimates (slightly higher personnel and other external costs).

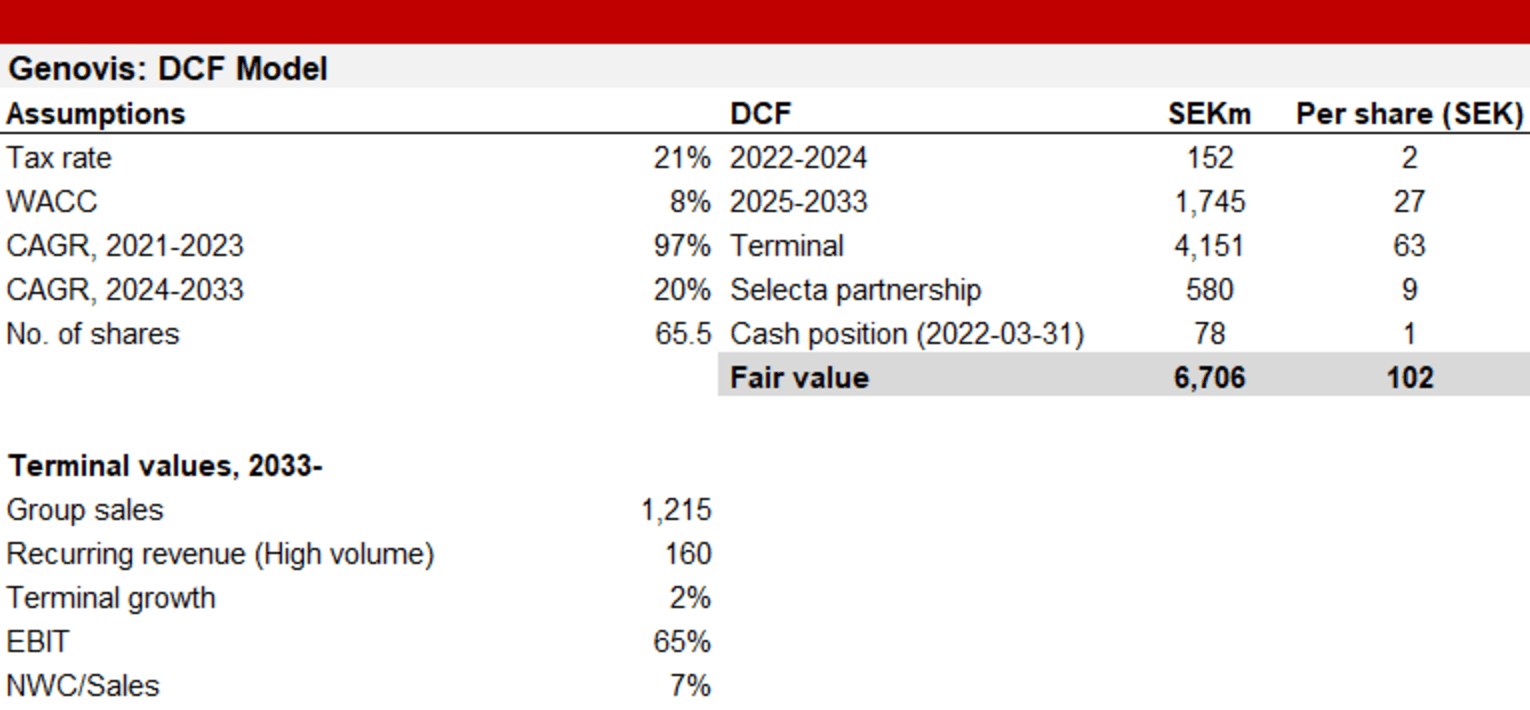

Following the Q1 report, we reiterate our Base Case of SEK 102 per share, while our Bull and Bear cases remain at SEK 150 and SEK 30, respectively. We also want to highlight that the share is one of Redeye’s Life Science Top Picks for 2022.