Suurin osa 888 liikevaihdosta tulee B2C liiketoiminnasta. Urheiluun liittyvä vedonlyönti se osa-alue, joka lukuja nyt kasvatti, koska 2020 vertailujakso oli niin heikko (COVID käynnissä, ei mitään tämänhetkiseen EURO 2020 jalkapalloon verrattavaa tapahtumaa). Pitäisi näkyä aika komeasti myös Kindred luvuissa kun liikevaihdosta n. 50 % pre-game ja live sport betting ja juuri ns. säännellyiltä markkinoilta, joita 888 kommentoi.

“Growth driven by regulated and taxed markets, which contributed 74% of revenue (Q2 2020: 73%), with strong performances in the UK, Italy, Spain, Romania and Portugal offset by the impact of the new regulation in Germany.”

“B2C revenue increased 11%, led by Casino (13%) and Sport (94%), with Sport growth boosted by a reduced number of sporting events in the prior year period”

Betsson posari, eiköhän tässä vedetä hyvin myös koko ala ylöspäin. Tuossa puhutaan, että turnauksien alkuvaiheen pelien lopputulokset olivat suotuisia Betssonille. Näin on varmaankin myös nyt viimeiset välieräpelit, kun molemmat päättyneet tasan.

“High sportsbook margin, high customer activity in general in combination with major sports events, such as the Copa América and the UEFA Euro 2020 and an increased share of sportsbook revenues in relation to total revenues, has created a strong EBIT momentum”

“The quarter saw an increase in active customer numbers of around 25 per cent compared to the same quarter last year, driven by an increased sportsbook activity. The sportsbook turnover increased by circa 73 per cent compared with Q2 2020. The sportsbook margin was approximately 8.5 per cent for the quarter, compared to the eight-quarter rolling average margin of around 7.4 per cent. The higher sport book margin is to a large extent explained by favorable outcomes in the initial phases of the two football tournaments.”

Kiinnostavaa on tosiaan tuo EM-kisojen pelatuimpien pelien päättyminen tasatuloksiin. Vedonlyöntifirmoille voisi kuvitella sen olevan jonkin sortin unelmatilanne. Brittien innostuneisuuden vedonlyöntiin tietäen, ei Englannin päätyminen finaaliin ollut myöskään pöllömpi juttu.

Kindred Group plc (the “Company”) hereby announces that it, on 9July 2021,has receiveda notification of major holdings from SMALLCAP World Fund,Inc., a company with its registered office in Los Angeles, USA.

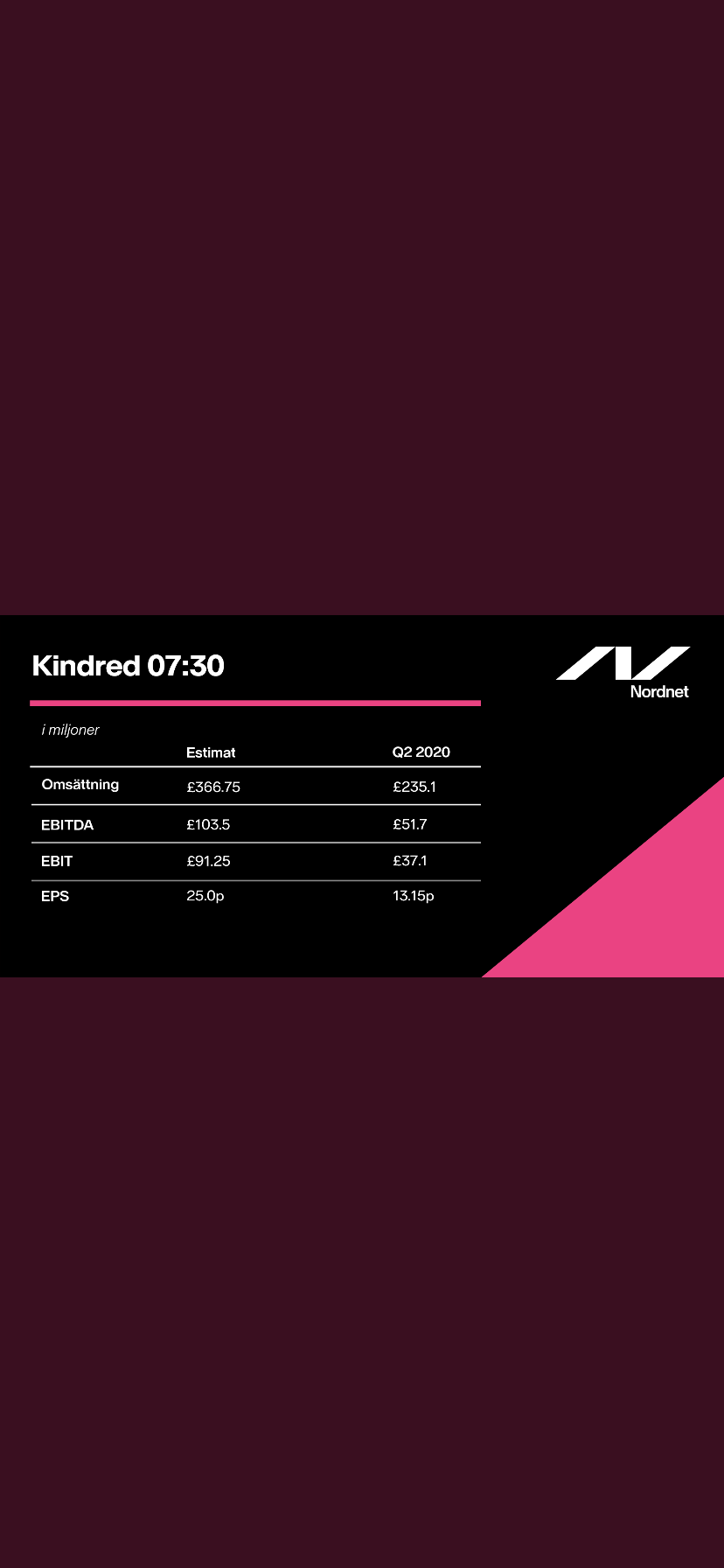

Kindred Group plc – Interim report: January – June 2021 (unaudited)

Second quarter 2021

Gross winnings revenue increased by 55 per cent to GBP 363.7 (235.1) million

Underlying EBITDA was GBP 114.3 (51.7) million

The result for the quarter has been impacted by M&A costs of GBP 3.7 million connected to the acquisition of Relax Gaming and a credit of GBP 4.2 million following a reduction of the disputed regulatory sanction from the SGA

Profit before tax amounted to GBP 102.5 (31.3) million

Profit after tax amounted to GBP 87.1 (26.8) million

Earnings per share were GBP 0.38 (0.12)

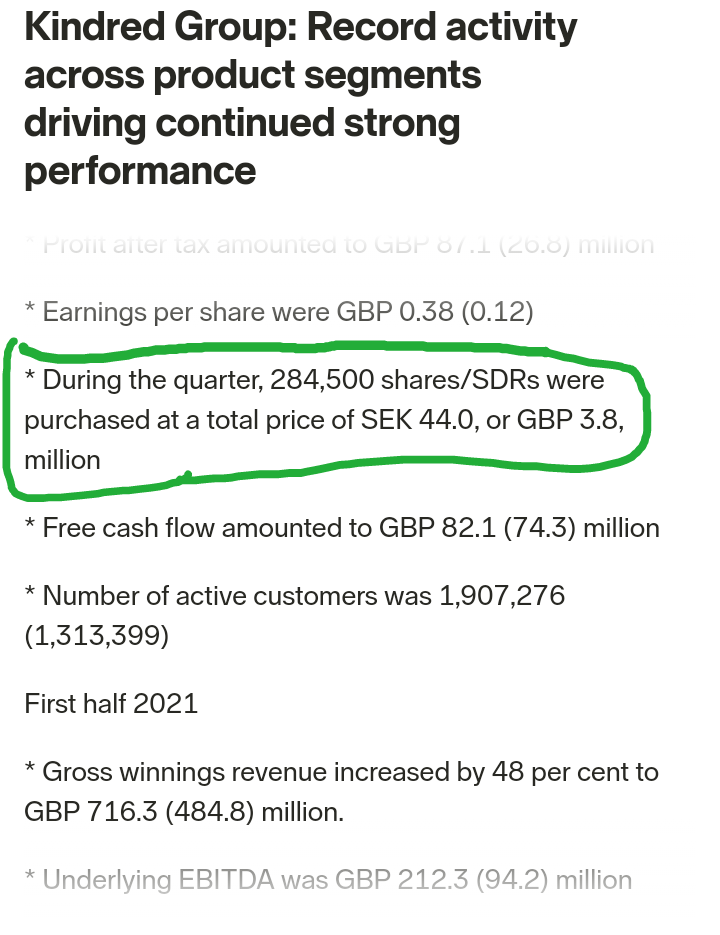

During the quarter, 284,500 shares/SDRs were purchased at a total price of SEK 44.0, or GBP 3.8, million

Free cash flow amounted to GBP 82.1 (74.3) million

Number of active customers was 1,907,276 (1,313,399)

Muutamat muut firmat ovat valitelleet että kasino on hiljentynyt EM-kisojen takia. Kindredin raportista tämä pisti hymyilyttämään:

“Meanwhile, the casino segment has delivered a record quarter with 18 per cent growth compared to the same period last year, despite this being a sports-heavy quarter.”

Selittäkääs joku viisaampi, miten tämä firma voi olla näin halpa? Onko kyseessä vain krooninen regulaatioriskin hinnoittelu uhkapelifirmoissa vai onko tässä jotain mitä en ole ymmärtänyt?

Ainoastaan auringonlaskun alat kuten öljy tulee mieleen, joista löytyy firmoja joiden P/E=9. Nämä tosin eivät kasvata tulosta 20%+ vuodessa kuten kindred.

Nordea på Kindred: We expect negative consensus est revisions of around -2% to 0% on adj. EBITDA and a slight negative share price reaction. The lower activity in the sportsbook and the slightly weaker sportsbook turnover is neg for H2 and speaks of a lower momentum entering Q3”.

En tuota Nordeankaan kommenttia kyllä ymmärrä, ellei jossain Raporttitiedostossa ollut enemmän asiasta kuin tuossa Q2 tiedotteessa.

Lisäksi omia ostettu ainakin hieman näköjään😃

Hei, Enemmän Kindrediä seuranneet osaatteko avata minkä vuoksi esimerkiksi Nordea odottaa EBITDA kasvavan tasaisesti vielä 2021E, mutta ottavan kyykkäyksen 2022E 336 → 291?

Vastaavasti 2018 - 2019 tapahtui iso kyykkäys kannattavuudessa 203 → 128. Sen verran lueskelin uutisia, että tapahtuiko tuolloin pari vuotta sitten jotain isoa regulaation suhteen? Ennustellaanko tässä jotain vastaavaa heikkoa kehitystä seuraavalle vuodelle? -21 P/E näyttää halvalta, mutta pohdin mitä tässä hinnoitellaan sisään tulevia vuosia ajatellen.

Moi,

Ihmettelin sitä aikaisemmin myös miksi se heillä näin menee, mutta muistaakseni liittyi kasvaviin markkinointikuluihin, joita syntyy kasvun seurauksena(USA todennäköisesti.) Tällainen muistijälki siis jäänyt.

Aivan samaa mietin. Vaikka arvostuskertoimet pysyisivät edelleen seuraavat vuodet alhaisina, niin kovat kasvuluvut EPS:ssä vetävät osakkeen hinnan pitkässä juoksussa samaan kasvuun. Jotain pelkoja täytyy olla ennusteissa.

Toisaalla arvioitiin, että voi olla jonkun suuren omistajan ESG-myyntejäkin. Ei ole erityisen vihreä tai moraalinen toimiala, joten jotkut rahastot haluavat ehkä siivota rivin pois vaikkapa sen takia. Itselläni ei ole siis mitään tietoa tästä, mutta tuollainen voisi selittää.