Kysyin tästä firman toimitusjohtajalta. Vapaasti muotoillen vastaus oli tyyliin, että “Ei me haluta kokonaan luopua öljypuolesta, koska meillä on timanttinen hallitus, joka osaa kasvattaa öljybisneksien osalta näistä lähtökohdista jotain hienoa. Tykätään pääomakevyistä bisneksistä.”

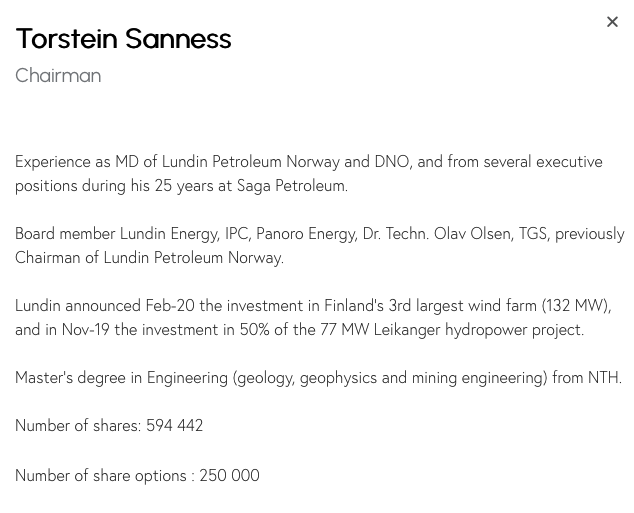

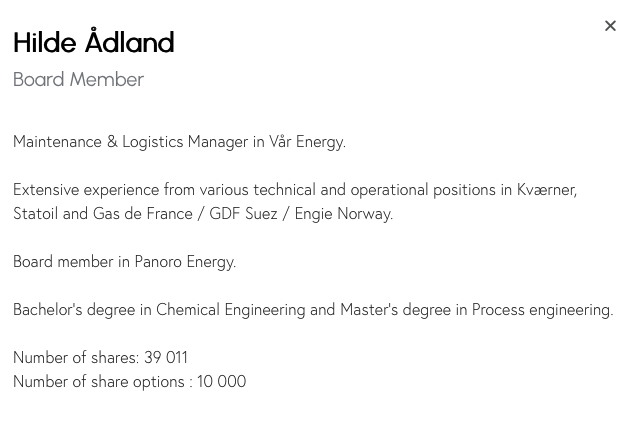

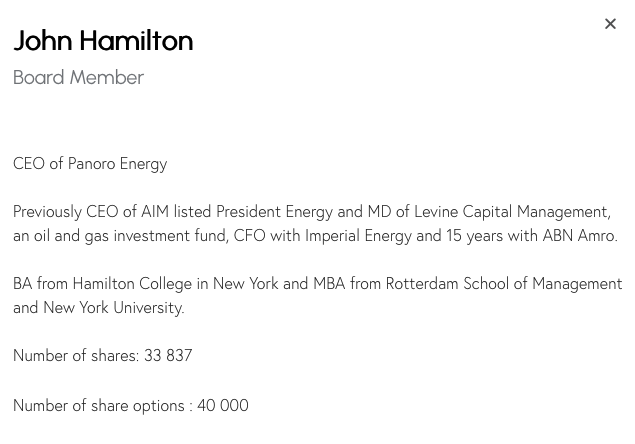

Onhan nää kyllä kovia tyyppejä ja kaikilla linkki Panoro Energyyn, joka omaa erittäin kevyen organisaation öljy-yhtiöksi, kun ostelevat pitkälti vähemmistöosuuksia öljyprojekteista: