Magnora ASA: Minutes from Extraordinary General Meeting 19 February 2024

19.2.2024 13:52:07 CET | Magnora ASA | Additional regulated information required

to be disclosed under the laws of a member state

MAGNORA ASA has today held an Extraordinary General Meeting.

Attached to this announcement are the minutes of the Extraordinary General

Meeting in Norwegian and translation into English.

All proposals on the agenda were approved.

DISCLOSURE REGULATION

This information is subject to the disclosure requirements pursuant to section

5-12 of the Norwegian Securities Trading Act.

Torstein Sanness, Executive chairman, email: sanness at sf-nett.no

ABOUT MAGNORA ASA

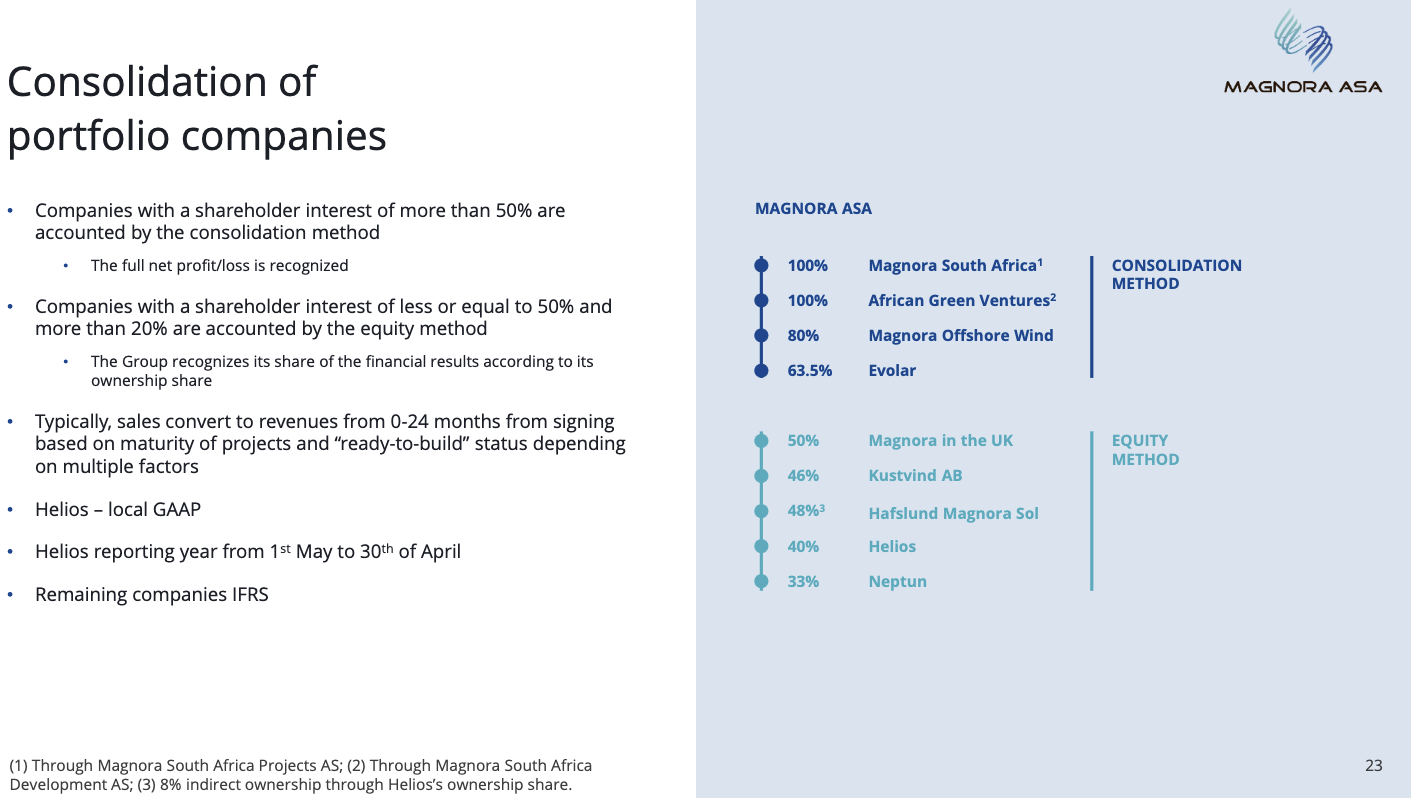

Magnora ASA (OSE: MGN) has a legacy royalty business that is re-invested in

renewable energy development projects and companies. Magnora’s portfolio of

renewable companies consists of Helios Nordic Energy AB, Kustvind AB, Magnora

Offshore Wind AS, Magnora Solar PV UK, Hafslund Magnora Sol AS, Magnora South

Africa, and AGV. The company is listed on the main list on Oslo Stock Exchange

under the ticker MGN.

Heliokselta vuoden ensimmäinen toimitus.

Sanoisin, että aika ajoissa keväällä viime vuosiin verrattuna, joten toivotaan tämän povaavan hyvää vuotta.

Kyseessä keskikokoinen 40 MW toimitus Nordic Solar AS:lle Gotlannin saarella Ruotsissa.

Teen uuden viestin aiemman editoimisen sijaan, jos joku jo peukuttaneista ei vaikka olisikaan halunnut peukuttaa tätä lisäystä.

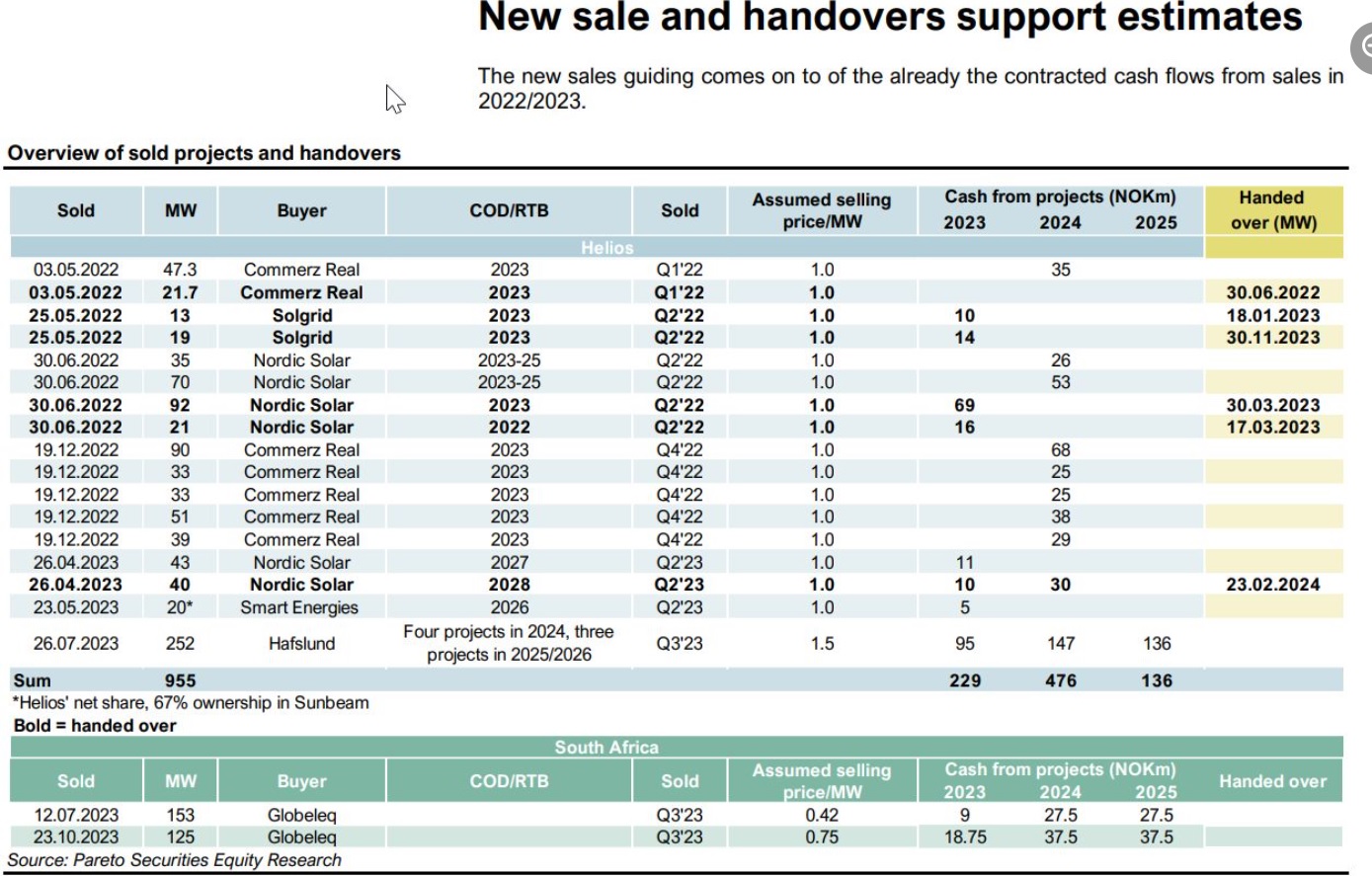

Tiedotteessa mainitaan, että Helios on myynyt tähän mennessä 955 MW verran projekteja.

On myös tiedossa, että Helios on maksanut tähän mennessä 60 MSEK osinkoa osakkeenomistajilleen.

Jos tehdään täysin vastuuton laskelma aiemmin viesteissä pyörineillä luvuilla:

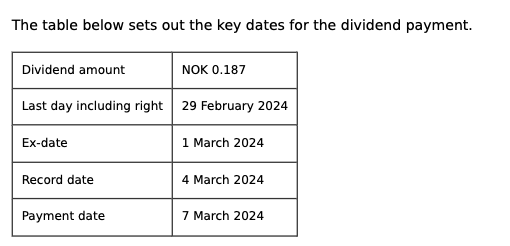

On 28 February 2024, the Board of Directors held a board meeting to authorize

cash distribution. The Board authorized a payment of 0.187 per share. The cash

distribution is based on the Company’s annual accounts for 2023 and

authorization from the AGM held on 25 April 2023.

Magnoran vuosirapsa ulkona, ja hyvältähän tuo ensinäkemältä näyttää, sekä kuluneen vuoden että 2024 osalta:

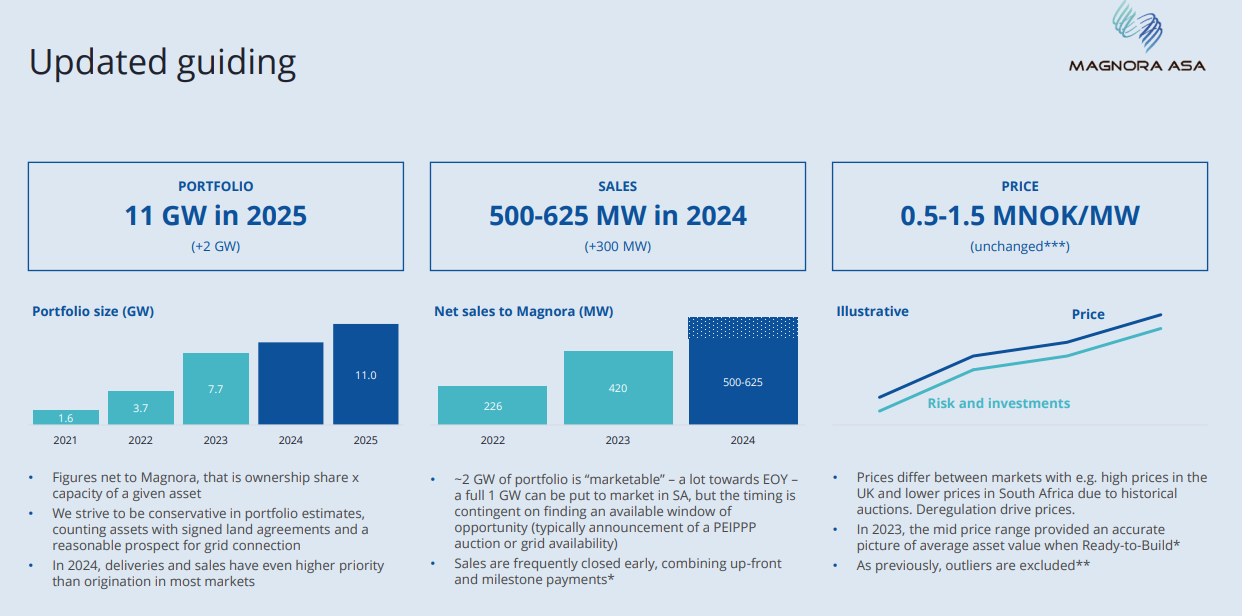

On 29 February, Magnora published its annual report for 2023. The company also published sales guiding of 500-625MW for 2024 (up from 200-325 MW in 2023) and raised its portfolio guiding for the second time in 9 months, now indicating an 11 GW landbank in 2025.

Magnora’s board emphasized how the company’s 2023 results would shape the outlook for 2024.

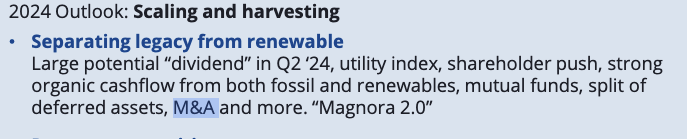

Strong results and strong cashflow from old and new business allow Magnora to split the legacy business from the renewable business and streamline the businesses.

More of Magnora’s portfolio companies are shifting from origination to sales, or from sales to delivery. Milestone payments are expected from multiple sources, alongside dividends and share buyback with more sales being recognized as revenues.

Organic growth looks set to continue across geographies and products, while farm-downs, and alliances remain a very real prospect in 2024 (cf. our stock exchange notice of August 2023, “Evaluation of Corporate Structure”).

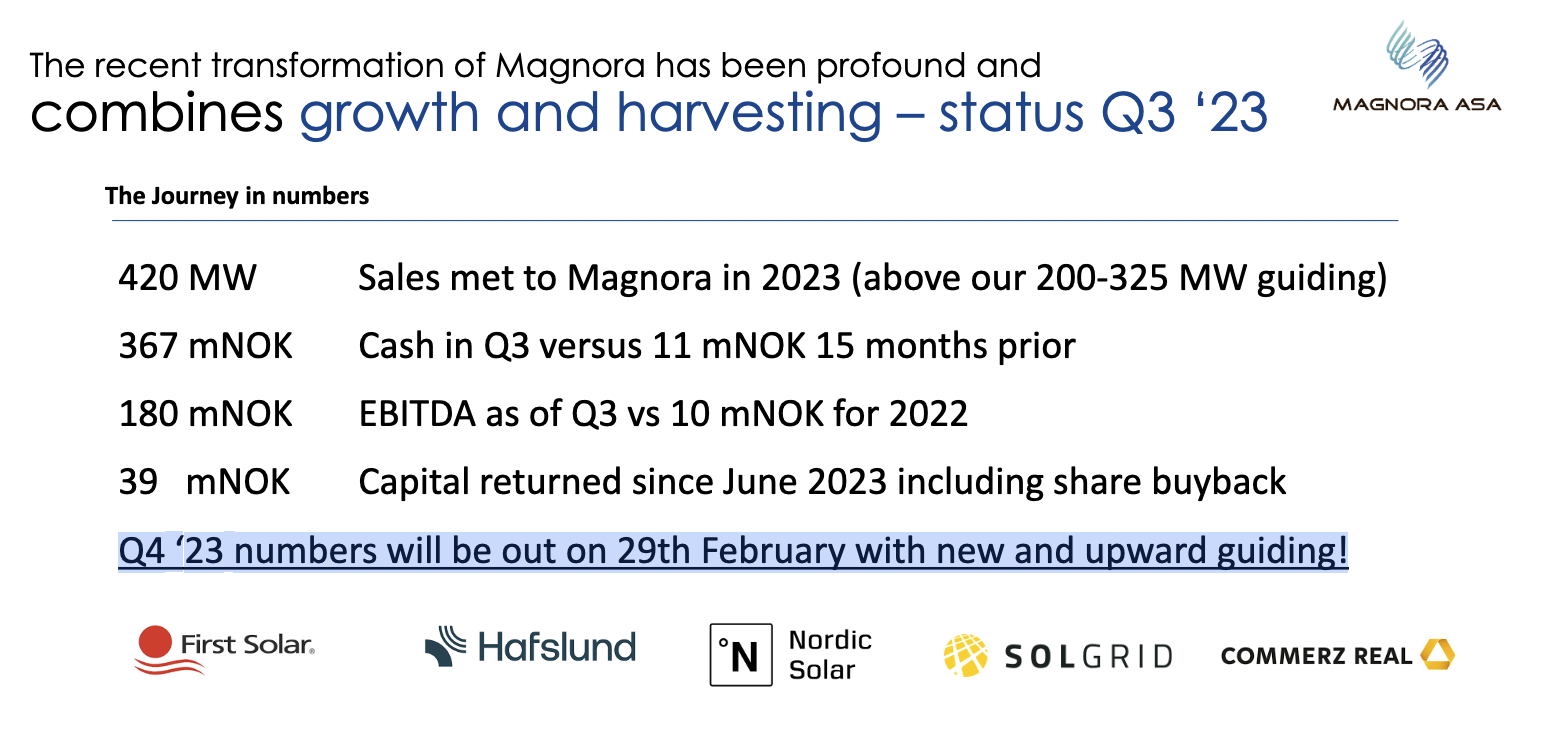

Net cash generated from disposals and other investment activities was NOK 304.9 million (negative NOK 125.3 million in 2022).

Net cash at year end: NOK 347.6 million

Sold 420MW (net to Magnora), beating our 200-325MW guiding in 2023

Grew the portfolio (land bank) to 7.7 GW by the end of 2023

Net profit was NOK 178.9 million (versus NOK 3.9 million in 2022). The increase was mainly driven by the disposal of Evolar and two SPVs in South Africa, coupled with positive results from associated companies in the Group.

Below are the highlights for the year:

On 12 May 2023, Magnora sold all its holdings in Evolar to First Solar, Inc. for approximately USD 29 million (NOK 314 million) and additional milestone payments of up to USD 24 million (NOK 256 million with 10.65 USD/NOK rate).

On 21 June 2023, the annual general meeting of Helios approved SEK 60 million (NOK 59.9 million) in dividends to the shareholders. Magnora holds 40 percent of the shares in Helios and received approximately NOK 24 million.

On 12 July 2023, Magnora sold its first project in South Africa to Globeleq, one of the leading IPPs in Africa owned by Norfund and British International Investment. The agreement provided for an upfront payment and additional payments subject to the project reaching certain commercial and technical milestones. The project is a 153 MW battery storage project with the potential to add solar PV to make it a hybrid project.

On 26 July 2023, Helios divested seven projects with combined capacity of 252 MW to Hafslund. This transaction is Helios’s seventh and largest in terms of size and value to date, and the price per MW for the projects sold is in the high end of Magnora’s price guiding. Hafslund is a leading European utility producing 21 TWh annually. Hafslund is also an owner in Magnora ASA.

Magnora continued buying back its own shares and held 1,070,854 treasury shares at the balance sheet date. The maximum consideration set for shares acquired under the buyback program is NOK 45 per share and NOK 50 million in aggregate.

On 23 August and 2 November, Magnora made a capital distribution of NOK 0.187 per share. Technically, Magnora repays paid-in capital in excess of the share’s par value, which can offer a tax advantage for some shareholders in certain jurisdictions.

On 28 August, Magnora issued a press release regarding evaluation of corporate structure and the hiring of Pareto Securities to assist in the process of enhancing shareholder value. The restructuring process has progressed and is expected to be implemented during the first half of 2024.

On 20 October, Magnora sold its second project in South Africa to Globeleq. The project is a solar PV project in an area with several potential industrial customers that have expressed an interest in private power purchase agreements (PPAs). The project was on 4 December expanded from 90 to 125 MW, releasing additional payment to Magnora.

On 31 October, Magnora sold all its shares in the Neptun Tromsø project to a project partner. The agreement provided for a cash payment, yielding a profit on invested capital for Magnora.

On 16 November, Magnora reached an agreement with NEO Energy and Dana Petroleum for redeployment of the Western Isles FPSO to the Greater Buchan Area (“GBA”) where start-up is expected in 2026.

Vuositasolla tulos on todella hieno, joskin suuri osa siitä on kertynyt ilmeisesti Evolarin ja Neptunin myynnistä…? Q4/23 tulos verrattuna vastaavaan kvartaaliin Q4/22 on huonompi: EBITDA Q4/23 on -13.9 verr. Q4/22 65.5, jossa operating revenue oli peräti 79.9 MNOK verr nyt 1,9 MNOK. Mistähän nuo isot Q4/22 tulot olivat syntyneet? Öljytuloja vai mitähän lienevät? Q4/23 tulos toki on parempi verrattuna edeltävään Q3/23:een: -15.9 MNOK verr. -19 MNOK. En osaa tarkemmin näitä tulkita, olisi mukava saada mielipiteitä näistä

Suunta on kaiken kaikkiaan hyvä, minkä osakurssikin nyt viimein on noteerannut

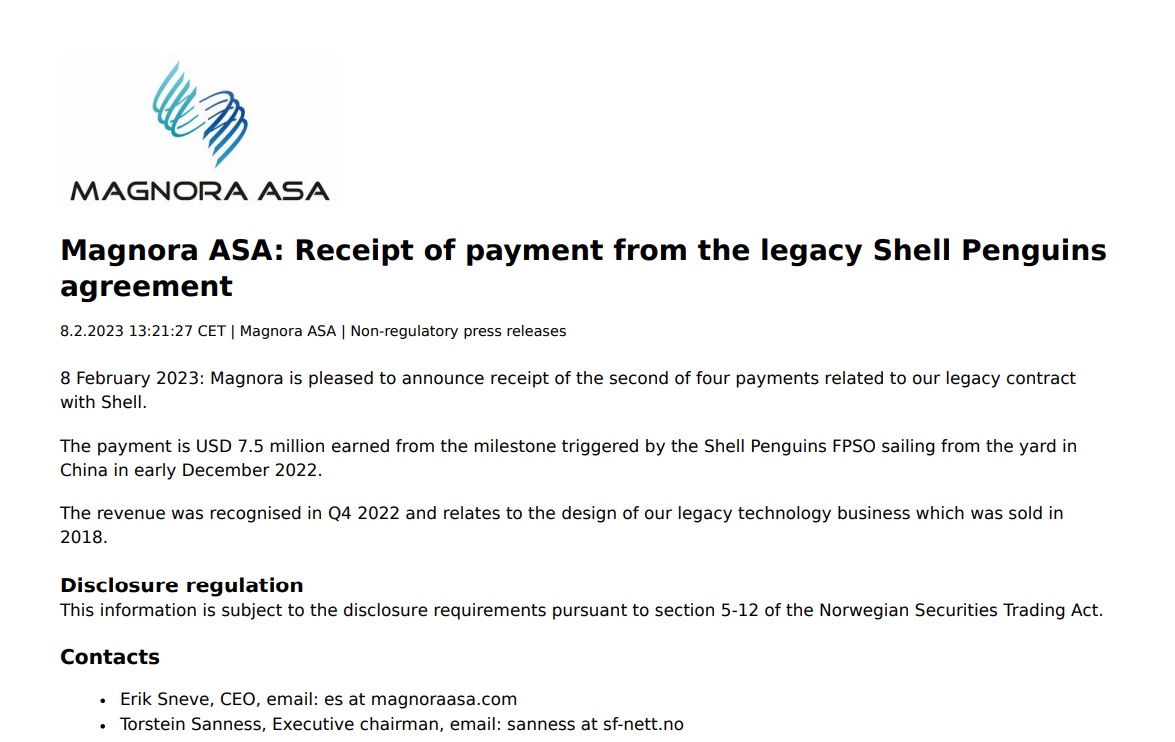

The big Q4/22 revenue came from the Penguins “sail-away” milestone. They recognized the revenue when the FPSO left from China. I believe it was 7,5 mill USD

Tämä taitaa olla ensimmäinen kalvo, missä myönnetään suoraan että öljylegacyn erottaminen uusiutuvasta bisneksestä mahdollistaa yritysjärjestelyt. Magnoran omia sijoituksia ja M&A-hankkeitahan öljybisneksen mukanaolo ei ole haitannut, joten kyseessä on Magnora joka tässä on M&A:n kohteena. Audiocastissa myös mainittiin “M&A related activities to Magnora and Magnora companies.”

Vaikka legacy-bisnes ollaan erottamassa uusiutuvista, niin Magnora mainitsee vuosiraportissa yrittävänsä myydä Western Islesin lisenssimaksut eteenpäin. Olen vieläkin hieman ihmeissäni tästä kiireestä listata legacyöljytfirmat pörssiin Q2 aikana. Sen jälkeen kun Western Isles on myyty ja saadaan noi loput Penguins rahat, niin legacyä ei enää ole. Ellei siellä nyt sitten kirjaimellisesti ole Hafslundin ostotarjousta odottamassa splittiä, niin luulisi että nuo saataisiin lähikuukausina myytä ja legacy ajettua alas orgaanisesti

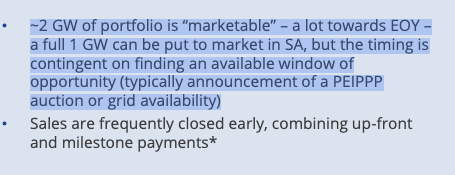

Yhtiö kertoi nyt myös ensimmäistä kertaa ohjeistuksen sille, että kuinka suuri osa maapankista on “myyntikunnossa”:

On kommunikoitu ulos ja tuota ei ole muutettu, mikä on hyvä asia sillä yleisessä keskustelussa on puhuttu, että uusiutuvat eivät enää olisi kannattava sijoituskohde nousseiden korkojen ja kustannusten vuoksi.

Magnoraa on hieman haastavaa tulkita perinteisillä luvuilla koska vain osa firmojen finanssitiedoista konsolidoidaan, mutta sitä arvokkainta osaa yrityksestä kohdellaan sijoituksena, jolloin kohdeyhtiön tulos ja maksetut osingot ratkaisevat. Tämä tehokkaasti piilottaa mm. Helioksen todellisen arvon niin kauan kun yhtiö on hurjassa kasvumoodissa:

Kysyin tästä firman toimitusjohtajalta. Vapaasti muotoillen vastaus oli tyyliin, että “Ei me haluta kokonaan luopua öljypuolesta, koska meillä on timanttinen hallitus, joka osaa kasvattaa öljybisneksien osalta näistä lähtökohdista jotain hienoa. Tykätään pääomakevyistä bisneksistä.”

Onhan nää kyllä kovia tyyppejä ja kaikilla linkki Panoro Energyyn, joka omaa erittäin kevyen organisaation öljy-yhtiöksi, kun ostelevat pitkälti vähemmistöosuuksia öljyprojekteista:

Voisikohan joku norjaa paremmin ymmärtävä käydä kuuntelemassa tämän ja tehdä pienen referaatin foorumille? Löytyy myös Spotifysta. Tuntuvat toisella foorumilla olevan aika innoissaan sisällöstä.

Also, @Hammerix, we welcome an agent from FA forum! We appreciate having someone with home ground advantage. And… related to that, I assume you have already listened to the above podcast? Would I be asking too much if I were to request a short summary of the main points? Just a request so no pressure. You wouldn’t even have to write in Finnish, English would suffice just fine

Edit: Podcastissa kyse siis Erik Sneven haastattelusta.

FA:n foorumilta poimittuja pointteja haastiksesta, joille haluaisin vahvistuksen:

Working with entry into 3-4 new markets!

South Africa will be the new Helios.

The sales in SA this autumn had a price of well over 100 million.

Well, the interview is 43 minutes, so I can not give you all the details. But I can highlight the main points:

South Africa:

They believe that South Africa will be the new Helios, and that all key circumstances are in place for this to happen.

They have an enourmous amount of land in SA. Size is compareable to building 40gw of solar pv, but grid connection is a restraint. So they include just a fraction of this when speaking about their portefolio.

They believe they will have 1 GW of the portefolio in SA marketable for sale in 2024, but timing is important.

They have sold projects for above 100 mill NOK in SA. Significant payment upfront, and then milestones through 2024 and 2025. 157 mill according to Pareto.

Other markets:

They have a team of 4 employees working on new markets on a daily basis.

They have identified 3-4 new markets - New geographies.

Offshore wind:

Not looking actively for new projects, but focusing on the ones they already have. Growth will happen within, Solar pv, battery and onshore wind (SA)

Legacy:

Spin off for several reasons.1. Utility index, 2. Mutual funds, 3. Largest investors wants to get rid of oil. 4. Enough money from renewables.

The new company will be similar to what Magnora was 4 years ago, but much better positioned. Better outlook on revenue streams from WI + Very good team.

Magnoras ownership has to be below 50%, but the board has not made a final decision. They need to get below 5% top-line revenue.

Value will most likely be highest when WI resumes production in 2026

If approved by AGM i April, Magnora shareholders will recieve this “monster-dividend” in June

Allekirjoittaneelta oli mennyt pieni präntti ohitse vuosikertomuksesta. Ilmeisesti Evolarin ensimmäinen milestone-maksu pitäisi saada ennen 12 toukokuuta, joten tässä on syytä odottaa lähiviikkoina tiedotetta että ensimmäinen milestone on saavutettu. Vaihtoehtoisesti jos tuohon mennessä ei mitään kuulu, niin saattaisi käydä harmillisesti niin että tuo Evolarin myynnin reilu parikymmentä miljoonaa dollaria jää saamatta.

Jotain ennätystuloksia tuo Evolar (Nykyään First Solar European Technology Center AB) on saavuttanut viime viikolla, joten toivottavasti tuosta se maksu pian irtoaa

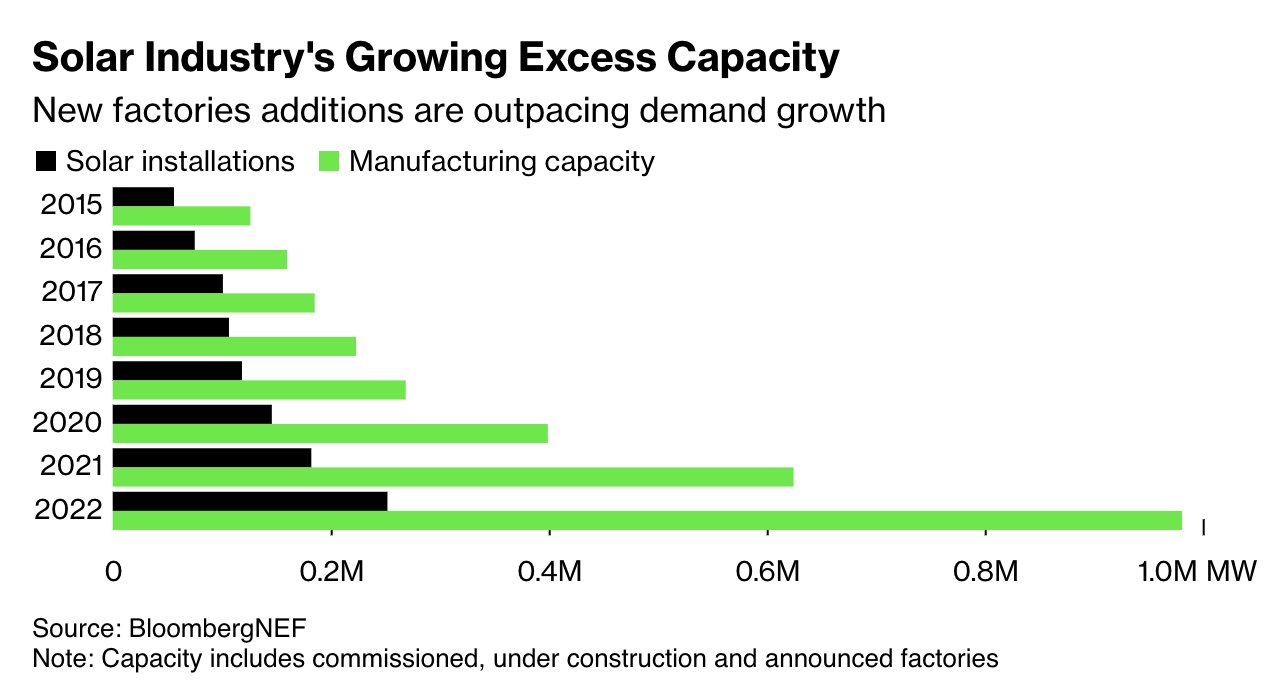

Aurinkopaneeleissa on valtava ylikapasiteetti tällä hetkellä ja lähivuosina. Tämä on erinomainen tilanne kehittäjille, koska matalat paneelien hinnat lisäävät kysyntää projekteista ja helpottavat investointipäätöstä aurinkoenergiaa operoivien yritysten osalta:

Näillä paneelien hinnoilla ja korkotasoilla ei oikeasti ole sähköntuottajille juurikaan järkeä rakentaa mitään muuta kuin lisää aurinkoenergiaa

Nyt tuli yhtiökokous kutsuki. 70% Magnoran PT2 osakkeista siirtyis Hermanni Holderille ja osakkeenomistajat saa yhen Hermannin per nykyne osake. Jakautumisen vaikutus Magnoran kurssiin 0,1 NOK osaketta kohden.