Niitä lienee erilaisia, mutta suurin osa liittynee aiempien tilikausien tappioihin, jotka sitten on vähennettävissä verotettavasta tuloksesta. Eri mailla on erilaisia verotuskäytäntöjä, joten jokaisessa toimitaan omien lakien mukaisesti.

5 tykkäystä

Ja lisäyksenä että tämä lienee liittyy myös q4/2020 tehtyyn alaskirjaukseen, josta voidaan mahdollisesti ammentaa lisää plussaa tulokseen, toki hyvää kirjanpitokäytäntöä noudattaen.

7 tykkäystä

Kannattaa pitää kyllä tätä silmällä jatkossakin Mobilen ohella

nyt Mobile Q1llä 45% liikevaihdosta, kun Infra 35%

7 tykkäystä

Viikko 17 – Viikon tärkeimmät Nokia -uutiset ja asiat

Omat subjektiiviset näkemykseni.

• Tärkeimmästä liikkeelle: Nokian tulos oli erittäin vahva vastoin yleisiä ennakko-odotuksia. Hämmästyttävästi liikevaihto kasvoi orgaanisesti 9 % (valuuttakurssihuomioituna 3 %) ylittäen konsensusodotuksen 8 %:lla. Verkkoinfrastruktuuri -segmentti oli tämän kvartaalituloksen tähtiosa-alue. Myös Mobile networks oli tulokseltaan positiivinen vastoin odotuksia. Lisäksi kassavirta oli odotuksia parempi – nettokassa on nyt peräti 3,7 miljardia euroa markkinoiden odottaessa keskimäärin vain 2,1 miljardin kassaa. Tämä avannee luultavasti paluun osingonmaksujen tielle seuraavan yhtiökokouksen jälkeen. Loppuvuoden ajan roikkuu positiivisen tulosvaroituksen mahdollisuus, ja varmaan enimmäkseen mahdollinen komponenttipula esti sitä tapahtumasta jo nyt. Jokainen analyytikko voi nyt luopua ajatuksesta että korpivaellus kestäisi vielä vajaat 3 vuotta. Kuuleeko Alex Duval, huhuu.

o Suositusmuutokset tähän mennessä:

Inderes 4,50 € (3,60), Lisää

Danske 4,60 € (4,40), Osta

Bank of America 4,70 € (4,00), Pidä

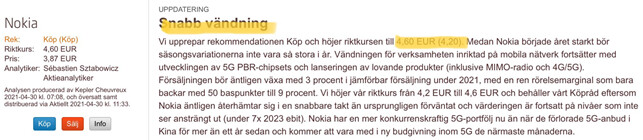

Handelsbanken 4,70 € (4,20), Osta

SEB 4,60 € (3,80), Osta

OP 4,10 € (3,6 €), Lisää

Nordea 5,0 € (4,5 €), Osta

Näiden keskiarvo 4,60 € (ennen muutoksia 4,01 €).

• Telefonica Spain valitsi Nokian toteuttamaan IP verkon modernisointia. Osana kauppaa Telefonica ottaa käyttöön Nokian 7250 IXR reitittimiä. Muutostöiden avulla Telefonica pystyy laajentamaan kiinteitä kuituyhteyksiä sekä näin 5G mobiilitarjontaa asiakkailleen. Nokian tiedote

• PA Consulting vahvisti tutkimuksessaan, että Nokia johtaa 5G patenteissa. Ei se määrä, vaan laatu. Nokian tiedote

• Italian suurin teleoperaattori TIM on tiettävästi työntämässä Huawein kokonaisuudessaan syrjään. Nokia olisi ilmeisesti saamassa (epävirallisen tiedon mukaan) 40 %:n osuuden rakennettavasta 5G verkosta, Ericssonin viedessä 60 %. Vielä joulukuussa Reuters uutisoi näin: “Ericsson will provide the bulk of the equipment, while Huawei and Nokia will get a 20-25% each”, one of the sources said on Wednesday.” Nokia olisi siis saamassa merkittävältä osin Huaweille ennalta suunniteltua osuutta. Muistamme TIMin myös siitä että se kritisoi Nokiaa vuonna 2019 ettei se ole teknisesti valmis, ja suunnitteli Nokian jättämistä kokonaan 5G rakentamisen ulkopuolelle. Signaalia!?

• Kenties ORAN riskiä ylimitoitetaan (ainakin joissakin keskusteluissa) Nokian ja Ericssonin näkökulmasta. Yksi Euroopan suurimmista operaattoreista Orange kertoi että vaikka heillä on tavoitteena vuodesta 2025 eteenpäin käyttää vain ORAN yhteensopivia verkkolaitteita, ja toisaalta heillä ei ole aikomusta pienentää Nokian ja Ericssonin osuutta omassa verkossa.

• Nokia vaikuttaa saavan privapuolella järjestäen lähes jokaisen sopimuksen mitä tulee kaivosteollisuuteen. AO GMK Nornickel (venäläinen kaivosyhtiö) ja Nokia ilmoittivat tiistaina, että Skalystyn kaivoksen pilottihanke onnistui.

• Signaaleja kun tarkastelee: BT:n teknologiajohtaja Neil McRae kehui twitterissä ”fantastisen partnerin Nokian platformia” samassa yhteydessä kun yhtiö otti käyttöön Nokian radioita uudella taajuudella.

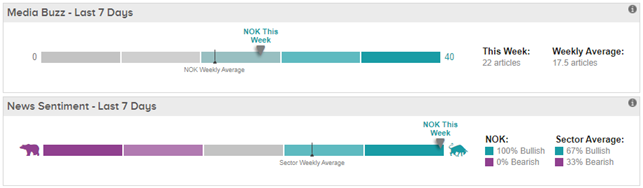

Tipranks News sentiment:

Viikon uutisvirta on ollut poikkeuksellisen myönteistä hyvän tuloksen ajamana.

Viikkoperformaatio: Nokia +12,8 % ja Ericsson -2,3 %. Nokia on noussut hyvän tuloksen ansiosta, toisaalta sektorilla on ollut painetta joka näkyy Ericssonin kehityksessä. Btw YTD tuotot: Nokia +27,3 % ja Ericsson +20,0 %.

Pitkä viikkotason tekninen kuva. Purkaantuminen ylös ja ulos symmetrisestä kolmiosta muutti Nokian kannalta asetelmaa selkeän myönteiseksi. Osake on tällä hetkellä 3,91-4,00 €:n vastusalueen (tukialueen) tuntumassa, ja seuraava tarkkailtava taso on noin 4,26-4,34 €. Samoin ”WSB huippu” 4,9505 € kannattaa jo muistaa, joka on kuukuusitason edellinen huippu. Odotan tästä eteenpäin nousevia viikkotason pohjia.

50 päivän MA 3,46 € - yläpuolella

200 päivän MA 3,52 € - yläpuolella

50 viikon MA 3,55 € - yläpuolella

200 viikon MA 4,27 € - alapuolella

Mikaelin kommentti tuloslivessä kuvastaa hyvin sitä että nousulle on perusteita.

24 tykkäystä

Ja mediaani 4,70 € , kun arvioidessa on hajontaa, niin usein mediaani on kuvaavampi.

5 tykkäystä

“Ei meidän tarvitse kertoa sellaista tarinaa että Nokia nousee uuteen loistoon ja siitä tulee kannattava kasvuyhtiö. Tällä hetkellä riittää kolmen vuoden remonttivaiheen katsominen, ja jos se onnistuu kohtalaisesti, niin selkeää että osake on eri tasolla kuin se on tällä hetkellä.”

Vastaa omia ajatuksia. Kohtalaisellakin onnistumisella tuotto-odotus on selkeän positiivinen.

9 tykkäystä

Muutama päivitys tuli vastaan:

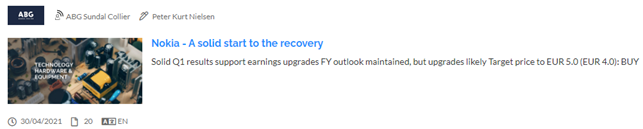

ABG Sundal Collier: Osta, Target 5,0 € (aiemmin 4,0 €)

Oddo BHF: Pidä, Target 4,2 € (aiemmin 3,8 €)

8 tykkäystä

… ja vielä Deutsche Bank. 4,60€ → 4,80€ (BUY)

04/30/2021 10:51:21 AM

Deutsche Bank raises target for Nokia to 4.80 euros - ‘Buy’

FRANKFURT (dpa-AFX Analyzer) - Deutsche Bank has raised the price target for Nokia after quarterly figures from 4.60 to 4.80 euros and left the rating at “Buy”. Like Ericsson, Nokia experienced a strong March after a weaker February, wrote analyst Robert Sanders in a study published on Friday. The Finnish network equipment supplier had literally blown away the expectations of the results./bek/knd/Publication of the original study: 30.04.2021 / Time not specified in the study / GMT

First publication of the original study: 30.04.2021 / 06:37 / GMT

9 tykkäystä

Laskennallisia verosaamisia syntyy kun yritys tekee kirjanpidollista tappiota. Verotuksessa vahvistetut tappiot saa vähentää voitoista Suomessa seuraavan kymmenen vuoden aikana. Kun tappiollinen yritys kääntyy voitolliseksi nämä verosaamiset ovat ihan todellisia ja pienentävät koko määrällään voitoista maksettuja veroja. Nämä eivät normaalisti liity kirjanpitoon muuten kuin, että näkyvät pienempinä veroina.

7 tykkäystä

Oleellista on, että aiempien vuosien tappioiden vähennys tehdään aina loppupäästä, myös ennen viimeisimmän tilikauden verojen maksua. Näin aiempien vuosien tappiot saadaan parhaimmalla mahdollisella tavalla hyödynnettyä.

2 tykkäystä

klo 13:54 päivitys

Update on Robot #1750 so far today in Helsinki Stock Exchange @ 13:54

1231 out of 14769 transactions was 1750pcs events ~ 8,34 % of all transactions

(1231x1750) out of 17,36m changed total shares ~ Minimum of 12,41% of total shares exchanged

(1231x1750) out of 16,69m changed total shares, without morning auction ~ Minimum of 12,9% of total shares exchanged

This between 10:00 and 13:54 today, with avg price of 3,98

Update on Robot #2000 so far today in Helsinki Stock Exchange @ 13:54

380 out of 14769 transactions was 2000pcs events ~ 2,57 % of all transactions

(380x2000) out of 17,36m changed total shares ~ Minimum of 4,38% of total shares exchanged

(374x2000) out of 16,69m changed total shares, without morning auction ~ Minimum of 4,48% of total shares exchanged

This between 10:00 and 13:54 today, with avg price of 3,98

3 tykkäystä

Pekka @ BloombergTV

Hyvä haastattelu tämäkin. Suunta on hyvä. Pekan kommunikaatio on sikäli hienoa - jämäkkää ja johdonmukaista.

19 tykkäystä

Lainattu Tomi Lahden twiitistä.

Kepler Cheuvreux Nokia osta, target 4,60 € (aiemmin 4,20 €).

Jospa nuo jotkut jenkkitahot myös ymmärtävät pikku hiljaa lopettaa myynnit. Eihän se GS vaan Alex Duvalin johdattamana tuota ongelmia?

8 tykkäystä

Otetaan alekorista lisää jos kerran jenkit tuuppaa sinne niitä. Kyllä tämä tästä…

13 tykkäystä

Mobile Networks is still the largest sales driver for the vendor, contributing revenues of €2.26 billion (slightly down from a year ago), but the unit is still in turnaround mode as the vendor migrates its portfolio to its own ReefShark chipset.

Lundmark noted during the webcast that demand had been strong across all parts of the Network Infrastructure portfiolio and that the “mega trends” driving demand for fixed access broadband technology “are not going away.”

3 tykkäystä

Taitaa se Goldmannin Duval vielä jättää Nokian target -hinnan 3,20 EUR? Ainakin tämä uutinen antaisi niin ymmärtää, ja ajoituksellisesti eetterissä 3h osarin ulostulon jälkeen.

Siinä missä periaatteessa osakesijoitus pitäisi kyseenalaistaa kun uutta uutista tulee, pitäisi myös oma analyysikin kyseenalaistaa. Tosin kun ei analyysiä ole tullut luettua, ei tietenkään voi tietää on herralla havainto jota itse ei tiedosta.

NOKIA : Gets a Neutral rating from Goldman Sachs

04/29/2021 | 04:12am EDT

Goldman Sachs confirms his opinion on the stock and remains Neutral. The target price remains unchanged at EUR 3.20.

© MarketScreener with dpa-AFX Analyser 2021

3 tykkäystä

Reilu tunnustus myös ajalle ennen omaa toimitusjohtajakautta. Parempia tuotteita ei vain ehditty saada ulos erilaisten vastoinkäymisten takia ennen Suria ![]()

8 tykkäystä

Jotenkin uskoisin, että päivitystä tulee vielä. Mutta Duval on koko ajan ollut ihan omilla asteikoillaan ja voi toki pitää itsepäisesti kiinni jostain päähänpinttymästään – ihmisiähän nämäkin. En tosin tiedä kenen etua se palvelee. Kysymyksiinsäkin Duval sai eilen kattavan ja mielestäni hyvän vastauksen Pekalta, vai onko nyt sitten siitä jotenkin möksähtänyt. Vaikea ymmärtää, miten eilisten lukujen ja näkymien valossa mikään ei Alexin mielestä ole muuttunut. ![]() Sen verran pitää antaa krediitiä herralle, että haistoi kuitenkin hyvin tilanteen, josta Nokian taapertaminen oikeastaan alkoi pari-kolme vuotta sitten. Nyt pitäisi vaan nähdä myös se paikka, missä tilanne kääntyy toiseen suuntaan. Eilinenhän nyt oli vain korjaus kurssinousuineen eli voihan Alex vielä osuakin todellisen nousun alkuun suosituksineen.

Sen verran pitää antaa krediitiä herralle, että haistoi kuitenkin hyvin tilanteen, josta Nokian taapertaminen oikeastaan alkoi pari-kolme vuotta sitten. Nyt pitäisi vaan nähdä myös se paikka, missä tilanne kääntyy toiseen suuntaan. Eilinenhän nyt oli vain korjaus kurssinousuineen eli voihan Alex vielä osuakin todellisen nousun alkuun suosituksineen.

En kyllä usko, että tämän miehen ja GS:n suositukset sanelevat Nokian kurssia. That said – yllättävän synkälle kannalle ovat jääneet pari jenkkipankkia ilman sen kummoisempia perusteluja.

12 tykkäystä

Tämä artikkeli oli itseltä mennyt kokonaan ohi (vai oliko jo täällä?), julkaistu päivää ennen Q1/2021

- FTTx is as hot as 5G, says Nokia’s President of Network Infrastructure

- Federico Guillén has submarine, optical, IP and fixed access in his portfolio

- Fixed access market demand for 10 Gbit/s PON is ramping fast

- Growth potential is there, but so is the competition

When Nokia CEO Pekka Lundmark announced his restructuring plan and new executive management team in October last year, all eyes were on the Mobile Networks unit and whether Tommi Uitto would retain leadership of the vendor’s largest and arguably most important division, with sales of €10 billion in 2020, nearly 46% of total revenues – he did.

There was less industry fanfare around the consolidation of the vendor’s fixed network units under the Network Infrastructure business group, but with €7 billion in revenues last year and a strong position in its key sectors (fixed broadband access, IP routing and optical infrastructure), long-time senior executive Federico Guillén picked up a prime role, and one that has become increasingly important during the past year as the value and importance of the long-haul, metro, packet transport and fixed access infrastructure (particularly FTTx) elements of telco networks has been reassessed and given appropriate credit.

Guillén even claims that network operators are now attributing as much importance to their fibre network plans and investments as they are to their next generation mobile broadband infrastructure.

“Customers say the fixed network is more important than ever – some have seen traffic volumes go up by 50%, as much as 75%, and it will not go down,” noted Guillén during a recent conversation with TelecomTV. “Also, the profile of the traffic in the networks is changing because now we have more upstream than in the past because now everybody’s doing video conferences… I believe we are going to make more use of the technologies that we have learned during Covid times.”

That’s one of the reasons that customer priorities are being reassessed, he says. “Customers used to tell us that 5G was their number one priority, but while 5G continues being a priority, fibre is as important as 5G these days for two reasons: One, to support the growing traffic volumes; and two, when you go deep with 5G and you’re going to millimetre wave, you’re going to need to backhaul all the small cells that are deployed, and you cannot do that with point-to-point fibre – you will need point-to-multipoint, and that’s the reason why our technologies are [evolving to] 25 Gbit/s PON for the right level of latency. The demand is clear, and we are serving multiple customers across the world with fixed access, with [optical] transport and with IP, because the pipes are getting filled…. the priority one year ago was 5G, and it was the only priority – now there are two priorities and equally important.”

Well, yes, of course his customers would say that and, of course, so would Guillén. But it’s logical that telcos would have to invest in fibre and IP transport to support cloud, streaming video and [ultimately] 5G traffic, otherwise the bottlenecks would destroy their business: As a result, major operators have been investing more in their fibre-based fixed access infrastructure for a few years now and there are also much greater competition in many markets, driven quite often these days by the involvement of private equity investors, which now have a growing appetite for digital infrastructure investments. That fuels new demand for the likes of Nokia’s Network Infrastructure unit and also acts as the catalyst for additional investments from incumbent operators, most of which are Nokia customers.

And according to Stefaan Vanhastel, CTO of Fixed Networks at Nokia, the demand for 10 Gbit/s fixed broadband ports is now booming.

“For us, XGS is our 10 Gbit/s [technology of choice] and we built two types of line card – a pure XGS line card, and a multi-PON line card, which supports multiple flavours, including GPON, XGS 10 Gbit/s and 25 Gbit/s,” he explains.

“What we saw happening in around Q2 and Q3 last year was that [demand for] the multi-PON line cards overtook the pure XGS line cards by far,” driven in part by increased levels of home working during the pandemic in Europe, the US and elsewhere. “And this is important because it shows a shift in the thinking of operators, because as long as you deploy a pure XGS line card, it’s a tactical 10 Gbit/s deployment, because what you do is you insert the XGS line card in an OLT here and there, and then whenever you need 10 Gbit/s you multiplex the 10-Gig wavelength into the PON, but that’s really a tactical deployment – it’s a port here and there. If you switch to multi-PON line cards, you get 10 Gbit/s on every port, and it’s really striking that we’re starting to get massive volume on the multi-PON line cards, which simply means that operators see that now is the time where you need 10 Gbit/s on every port. So this year we’re ushering in the mass adoption of 10 Gbit/s,” added Vanhastel.

“And it’s not just residential, it’s business services, and mobile transport, and that of course links to the evolution of 25 Gbit/s. For us this is all on the same line card – GPON, XGS and 25 Gbit/s, so that makes for a very easy introduction, but the interest is there… the scaling of the residential network to 10 Gbit/s, and then the reuse of that network for business services and for mobile transport,” he adds.

So where’s this demand particularly noticeable? Exact detail isn’t forthcoming from the Nokia execs, but Guillén notes that operator customers are “pushing the pedal to the metal on fibre” in European countries that don’t have big penetration of fibre…Germany, Belgium, Netherlands, UK, Italy, France,” he says.

It’s possible some of that activity will show up in Nokia’s first quarter 2021 financial statement, which hits the wires on Thursday (29 April).

There’s certainly optimism at Nokia that the Network Infrastructure business will grow, as the overall market is expected to grow (see chart above) and Huawei, a key rival across all sectors, is struggling to hang on to existing customer relationships in many markets: Guillén declined to discuss specifically whether Nokia is snapping up new business as Huawei falters.

But of course Nokia doesn’t have the fixed, IP routing or optical markets to itself and Huawei isn’t the only rival: In fixed access ADTRAN has been doing well, while Calix has just reported first quarter financials that were much healthier than anticipated, and DZS under the stewardship of Charlie Vogt is increasingly aggressive; Cisco and Juniper are still major rivals in IP routing; and in optical Ciena, Infinera, ADVA and others are also benefiting from positive market trends.

Under Nokia’s new structure, Guillén now has full P&L responsibility for the Network Infrastructure unit, so its success (or otherwise) will rest fully on his shoulders: The potential is there for the unit to deliver an increasing slice of Nokia’s pie and help prop up the Mobile Networks division while it takes a margin hit this year. If that can be achieved, then maybe the spotliohgt will fall more often on the fixed side of Nokia’s house.

20 tykkäystä

Hieno nosto, eteenkin kun olemme saaneet nähdä, että noin juuri kävi todellisuudessa. Informaatiolla on arvoa, jos sitä osaa käyttää. Ongelma vain on, että sitä on niin paljon, ja kuten olemme nähneet, ennustaminen on vaikeaa. OP:kin ennusti poikkeuksellisen heikkoa Q1:stä, vaikka yleensä on ollut tarkimpia Nokia-ennusteissaan, ja Mikael joutui kääntämään takkinsa kokonaan. No, Mikael teki sen ihan arvostettavalla tavalla, siitä pisteet hänelle. Mikaelin puolesta pitää toivoa, että Nokia suorittaa jatkossakin ![]()

18 tykkäystä