Q1 luvut ulkona:

Vahvaa kasvua edelleen, EPS juuri karvan verran plussalla. Samoin Free cahs flow plussalla ![]()

- Beat Q1 guidance on both of the non-GAAP metrics we primarily focus on, ex-TAC Gross Profit and Adjusted EBITDA.

- Revenues of $354.7M grew 17% over Q1 2021.

- Gross Profit of $112.0M grew 25% and Ex-TAC Gross Profit of $138.2M grew 31% over Q1 2021 and 8.4% pro forma with Connexity**.

- Generated net income of $3.9M, Non-GAAP Net Income of $21.9M and Adjusted EBITDA of $34.9M.

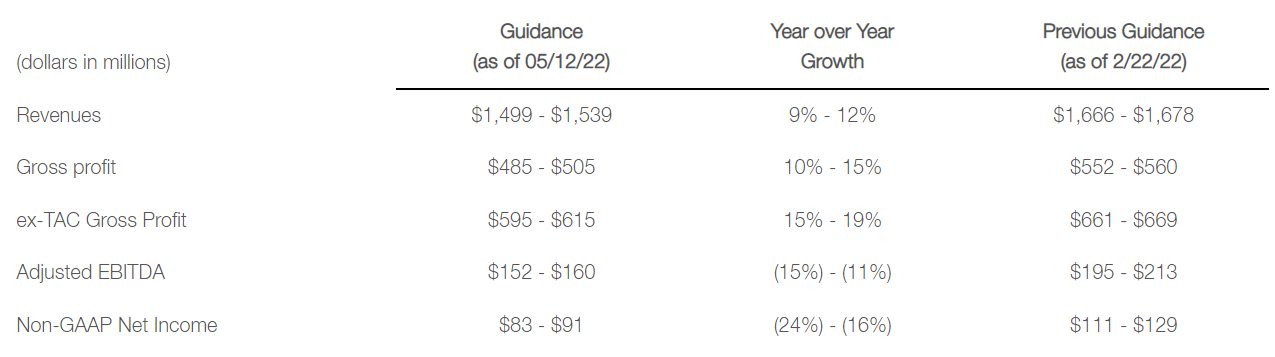

- Revising 2022 full year guidance ranges to Ex-Tac Gross Profit of $595M to $615M, and Adjusted EBITDA of $152M to $160M.

Jatkossa kuitenkin vedetty ennusteita reilusti alas, kasvu jatkuu YoY, mutta hidastuu ![]()