Seeing Machines (LSE: SEE), https://www.seeingmachines.com/, a global company headquartered in Australia, is an industry leader in computer vision technologies which enable machines to see, understand and assist people. The company originates from the Australian National University, founded in 1999 by Alex Zelinsky, Sébastien Rougeaux, Tim Edwards and Jochen Heinzmann. Seeing Machines Limited has been listed on the AIM market of the London Stock Exchange since December 2005.

The Company’s machine learning vision platform has the know-how to deliver real-time identification and understanding of drivers through Artificial Intelligence (AI) analysis of heads, faces and eyes. This insight enables Driver Monitoring Systems (DMS), which monitor driver/operator identification and attention and can detect drowsiness and distraction across multiple transport sectors.

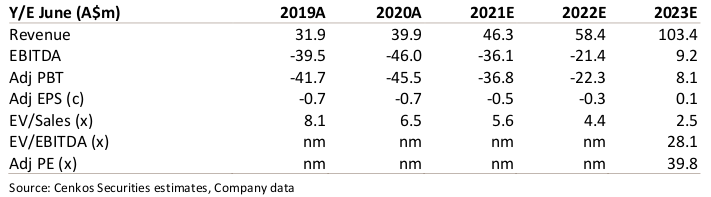

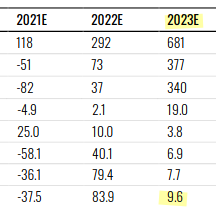

SEYE ketjussa oli spekulaatiota osakkeiden ensi vuoden kurssikehityksestä. Raa’asti jos vertaa Cenkoksen laatimaa ennustetta SEYEen, niin SEE ei nyt varsinaisesti näytä halvemmalta ainakaan peilaten hieman pidemmälle, vuoteen 2023. Päinvastoin. Tietysti ennusteet ovat vain ennusteita, joten niihin pohjautuvat vertailut pitää ottaa varauksella.

Alla RE:n näkemystä SEYEstä, alin rivi PE, ylin rivi Revenue

Earlier strategy didn’t succeed. Not enought HW agnosticism compared to competitors. Xilinx chips aren’t preferred enough widely by OEMS.

Top management was changed due to this.

They negotiated a deal with Qualcomm to have “fast access” to ~20OEMS. Most likely the terms of this deal are in favor to Qualcomm.

Here I have to point out that QC is most likely working with all HW agnostic Tier2 DMS providers. Smart was their new partner at CES2019:

One thing is that I don’t have that positive view of Seeing’s management… Like here they are giving a very questionable statement about industry analysts knowledge. Not good.

P. McGlone:

Redeye analyst covering Smart Eye. I have read his reports and he has no idea what he is talking about. He really doesn’t understand how everything works in the OEM industry.

Source:

Also some bad feedback from former employees. This is in contradiction to what I have learned from SmartEye.

September 2020:

“Outdated technology, desperately trying to pretend it is the world leader. Terrible management who seem like they are just attempting to cash in before the company runs out of money. The entire business plan is built around hope, even though that hasn’t worked for the last 10 years.”

Source:

Opportunity:

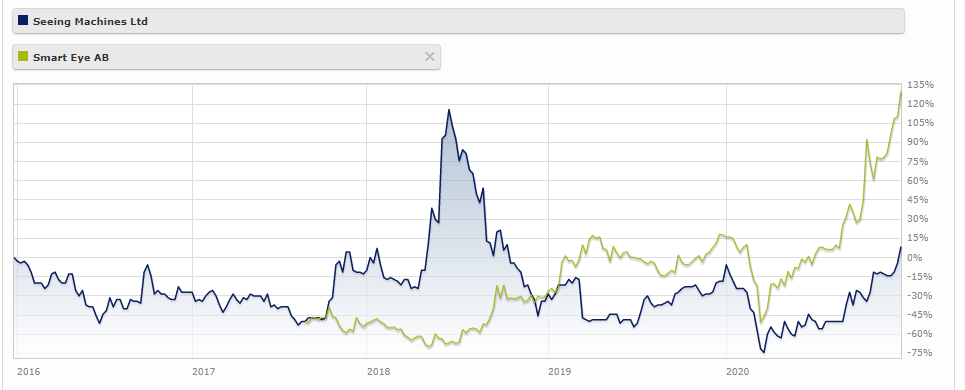

Now the situation is very interesting. It’s an interesting tought that by having both SEYE and SEE in your portfolio you could have maybe 80-90% of the DMS market.

I’m not expecting SEE to success very well in upcoming “DMS procurements” but it’s possible that SEE has fast access to Qualcomm integrated vehicles.

If the DMS market advances quickly in 2021-2024 most likely you wouldn’t have to wait 4 years and still be at 0% return as those that bought in 2016… very interesting.

However current pricing does not seem that cheap in terms of 2023 estimates (P/E clearly over 40, EV/EBITDA over 30). But there is quite a leap in 2024 estimates.

Tätä olen miettinyt myös. Monissa keskusteluissa en ole löytänyt yhtäkään mielipidettä, jossa olisi kyseenalaistettu Qualcomm-diilin haittapuolia.

Oon myös miettinyt, että miten Qualcommin kautta mennään myymään asiakkaalle ilman että osallistutaan kilpailutukseen? Luulisi että autofirmat haluaa kilpailuttaa pienimmänkin asian/softan joka nykyään ja varsinkin tulevaisuudessa autoihin tulee, koska niitähän tulee kasvavasti

Jos Qualcomm myy jotain kokonaisratkaisua, niin en tosiaan veikkaa että on niiden omis tuotteita joista katetta lasketaan, vaan juurikin (epätoivoisen?) Seeingin katetta, kun on pienempi toimija ja riippuvainen Qstä.

Here is one of the advantages of optimising your code for specific hardware, it can run really well on the hardware that is some carmakers have already selected.

It may take a few years for Agnostic software to run well on what is really quite different hardware that also supports Over The Air updates

Save the date! Our Automotive Redefined: Technology Showcase event is taking place January 26-27. @cristianoamon and @nakulduggal will host the 2-day event, covering our latest cutting-edge automotive tech and sharing insights into the industry’s future. https://twitter.com/Qualcomm/status/1336748693056352257/photo/1

@T3r00 Seeing Machines is listed on the AIM market of the London Stock Exchange. It is a proper market, but just like the shares on the Nordic markets, not all shares on all markets are available on all platforms

Hmmm… Stock price have been nearly the same from 2006.

Why ?

What is wrong with this picture. I think that SEE and Seye should have biggest market position.

Huge dip 2018-2020 what was the reason ? Investors tired to wait for profit ?

Can you open this for me ?

Regards Parre

Edit:

I am new in stock markets so I apologize for dumb questions. But since you know so much of SEE . I try to learn and see if you can sell this for me

@Parre, the spike in the price was on news of a contract with Ford (The F-150 truck the highest selling vehicle in the States and 2nd in the world) and on rumour of a takeover.

But during this time there was a worldwide shortage of capacitors which delayed delivery of our fleet product Guardian just as we had scaled up the US sales operation.

That is all resolved now. Heads did roll.

The Guardian devices have now clocked up

5,741,407,225 kilometers travelled

8,099,462 distraction events detected

153,621 fatigue interventions

(in last 12 months) https://www.seeingmachines.com/ for daily updates

For each of those distraction events we have captured the video. These are sent to our centres in Canberra, Australia or Tulsa, USA for analysis of the event if relevant the haulier is contacted and they contact the driver. That is the 150k number.

The haulier pays a monthly fee for this service as well as the upfront hardware cost.

Due to the delay in Guardian our cash flow suffered so profitability moved back several years and there was an extra fundraise. That is what caused the long term flat share price.

I am glad to say with our last fundraise our share price rose due to the confidence of bringing in US funding

EDIT: the guardian events are used for training AI, so we have a rich variety of edge cases which means we have fewer false positives and can catch more real positive events